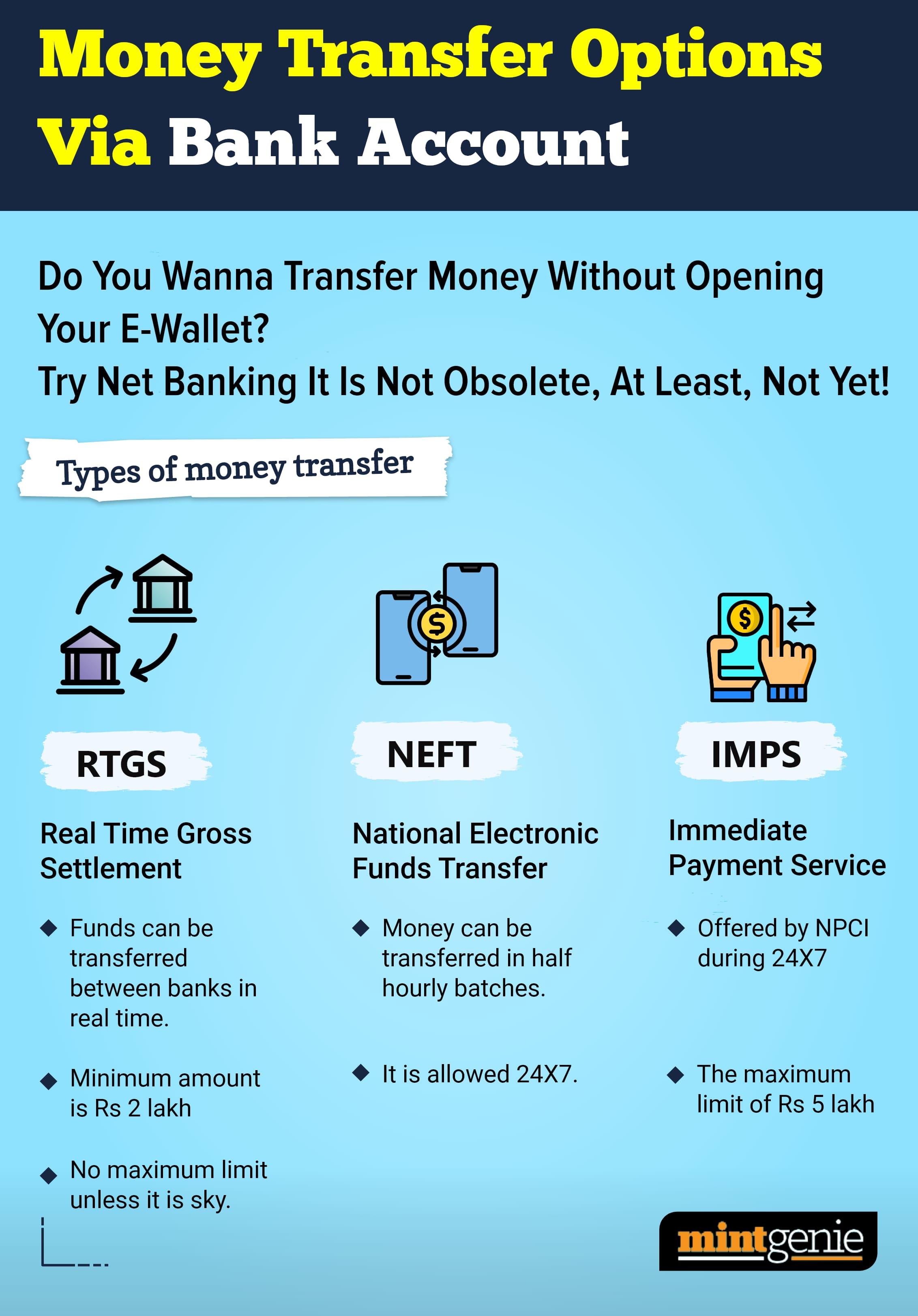

Since May, the Reserve Bank of India (RBI) has raised repo rates by a total of 225 basis points. This led to the raising of interest rates on lending as well as on fixed deposits (FD) by banks.

From time to time, a number of private and PSU banks have raised interest rates on their term deposits. So, the investors who locked their funds at the start of rate hike cycle lost big on potential earnings. And those who were patient with time and invested at a later stage stand to earn higher income.

But one does not know whether the rate hike cycle has already ended or will continue for more time to come. The better alternative, therefore, is to opt for the fixed deposit (FD) laddering.

What is FD laddering?

When you expect fixed deposit (FD) interest rates to increase, or at least change, in the near future — then instead of booking one term deposit over a long duration — it is recommended to book a series of fixed deposits (FDs) over a period of time. This process of booking a number of FDs is known as FD laddering.

Let us understand this with the help of an example. Suppose there is Mr A who wants to invest ₹5 lakh in a fixed deposit. But he wants to earn the maximum rate of interest i.e., the prevailing in the market.

There are two options: One is to invest ₹5 lakh in one term deposit assuming that the rates of interest will later on decline. And the second alternative is to open a number of deposits, say five, of ₹one lakh each across multiple tenors to make the most of surging interest rates.

For example

1. ₹one lakh FD starts in December, 2022 for six months.

2. ₹one lakh FD starts in December 2022 for one year.

3. ₹one lakh FD starts in December 2022 for two years.

4. ₹one lakh FD starts in December 2022 for three years.

Further, it is vital that the first FD that matures in June 2023 is further invested for a longer duration, say two years.

The second FD that matures in December 2023 should be further invested for another two years. The third FD that matures in December 2024 can be further invested for another three years and finally, the fourth FD is further invested for another three years.

This way, investor can earn different rates of interest on different term deposits.

Although one might wonder that a marginal increase of 5 or 10 basis points will not lead to any major difference in the overall returns, but a series of rate hikes can definitely make a considerable difference to the overall sum total of returns.