It seems like “Income Tax” is the most feared word in many people’s minds. The division of income into various tax slabs, the numerous heads to calculate your income sources, the complexity of deductions, exclusions, rebates and cess is enough to drive anyone crazy. However, experts also maintain that saving on your income tax can a go long way in guaranteeing your financial fitness. Some important measures that can help you include:

Invest in tax-saving instruments

True that regular investing in stocks can earn a huge corpus in the future, but you cannot also ignore the tax burden that comes with it. So, let me advise you of some simple investment options that would not only yield you some good returns but relieve you from the burden of too much taxation. For example, the amount invested in some specified instruments listed under Section 80C of the Income Tax Act, 1961 can help you with certain tax deductions. Some popular investment instruments that can help you to plan your taxes include:

- Employees’ Provident Fund (EPF) or Voluntary Provident Fund (VPF)

- Public Provident Fund (PPF)

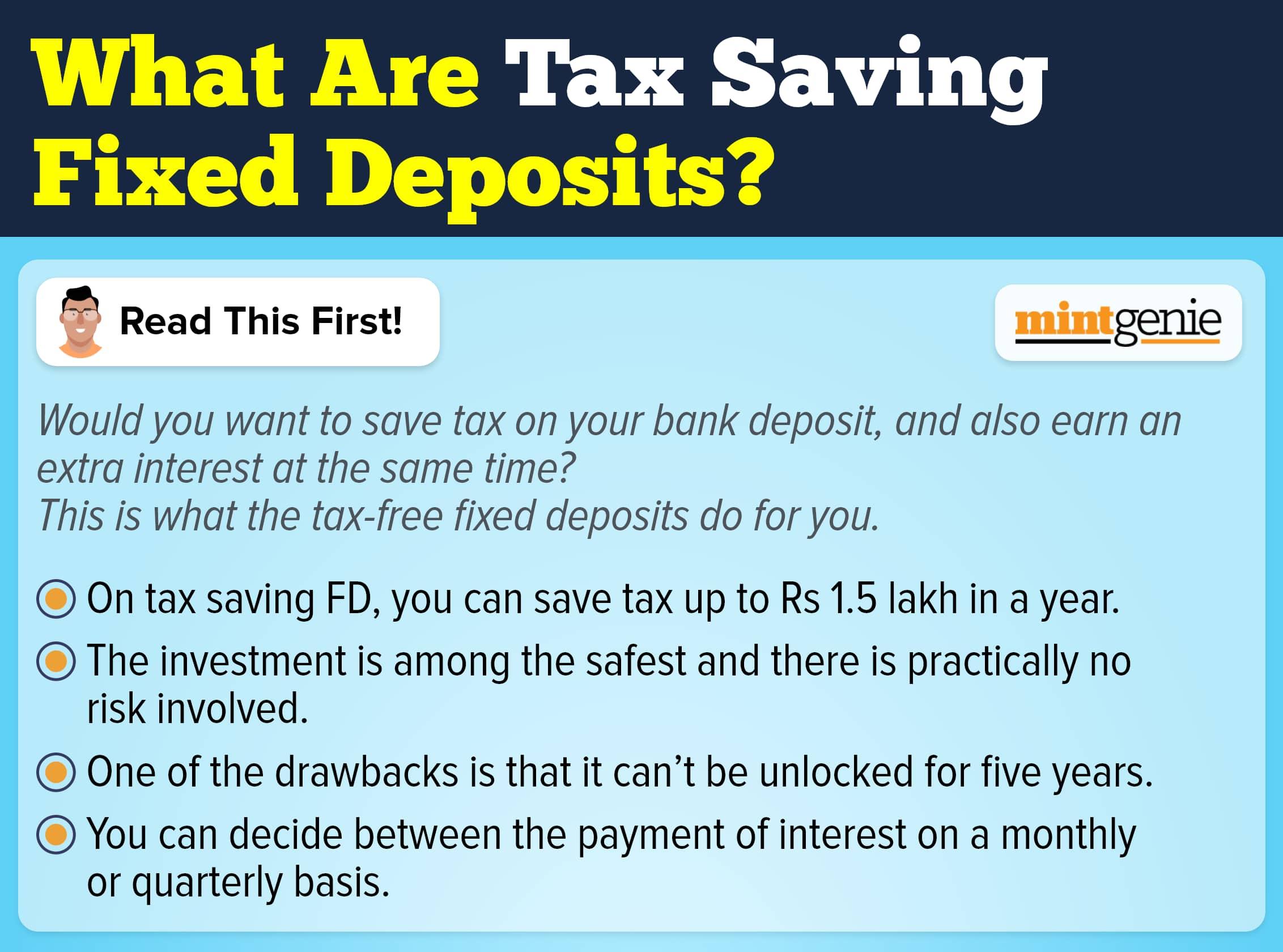

- Tax-saving fixed deposits

- Life insurance policies

- ELSS mutual funds

- National Pension Scheme (NPS)

- Pension plans

Investments in EPFs would yield annual returns of 8.1 per cent returns based on the recent announcement by the Employees' Provident Fund Organisation (EPFO). Some people tend to allocate extra money to VPF as a part of their retirement planning strategy. However, you must ensure that your contribution to both EPF and VPF must not exceed ₹2.50 lakh in any financial year, else income tax will be calculated on the interest earned on the excess provident fund contributions.

Money kept in PPF would give you 7.1 per cent returns, which is still higher than that earned on fixed deposits or most fixed-income plans.

Tax-saving fixed deposits do not help much, but a one-time deposit of ₹1.50 lakh can free you of the tax debt.

If you are looking at great returns along with tax reprieve, you can surely opt to invest in ELSS mutual funds that give market-linked returns.

Contributions to the NPS, a government-sponsored retirement benefits scheme, to facilitate regular post-retirement income to all its subscribers, are also eligible for deduction. The contributions to NPS are available as additional income tax deductions of up to ₹50,000 in NPS (Tier I account) under Section 80CCD (1B) of the Act. There are other pension plans too specified in the section from which you may choose and invest accordingly.

Choose components in your salary structure

If you are salaried, it is good to check the salary structure offered by your employer and opt for only those components that help maximize tax benefits. For example, you can opt for the House Rent Allowance (HRA) component in case you are paying rent, education allowance, food coupons, or seeking reimbursement for telephone/internet expenses. You can claim appropriate deductions/exemptions while computing taxable income as per the given tax slab in the old regime.

Take a home loan to avail tax benefits

Not all debt secured is bad debt. Take, for example, a home loan that you take to buy or construct your dream home. Did you know that you could seek tax exemptions on the cost of acquiring your home too? Both the interest and principal paid on the loan can be claimed as a deduction from the gross taxable income, subject to specified limits under the old tax provisions. You can avail of a deduction of up to ₹1.5 lakh on the principal repayment amount

This means that you buy your home at no added cost as the amount you pay towards loan repayment is deductible from your gross income, thereby, allowing you the benefit of a lower net taxable income.

Buy health insurance

This advice may seem advice at the outset, but health insurance is nothing short of an asset in disguise. Think of a possible situation wherein you or your dependant end up being hospitalized or have to seek medical treatment due to an accident or sickness. The medical expenditure would not only eat in your salary but also create a dent in your savings. Having health insurance saves you from the unwanted liability of hefty medical bills. Annual premiums paid towards health insurance policies ( ₹25,000 for self, spouse and children; ₹50,000 for parents aged above 60 years) are eligible for tax deductions under Section 80D of the Act. These deductions are over and above the amount you can save on taxes under Section 80C of the Act.

| Circumstances | Maximum Eligible Tax Deductions |

| Health insurance bought for self and family (all below 60 years of age) | ₹25,000 |

Health insurance bought for self and family + Health insurance bought for parents (All members being below 60 years of age) | ₹25,000 + ₹25,000 = ₹50,000 |

| Health insurance bought for self and family (All members aged below 60) + Health insurance bought for senior citizen parents | ₹25,000 + ₹50,000 = ₹75,000 |

| Health insurance for self and family (Eldest member being more than 60 years of age) + Health insurance for senior citizen parents | ₹50,000 + ₹50,000 = ₹1,00,000 |

Now that you are aware of investments that can benefit you both in terms of returns and taxes, you must take care to note that all the aforementioned deductions are available only if you file for taxes under the old tax regime. The government has come out with a simplified new tax regime to benefit those who wanted to escape the pain of calculating various deductions and exemptions to arrive at the net taxable income.

You can choose to pay taxes at reduced slab rates under the new regime available without deductions and exemptions. However, from the tax perspective, you must assess your tax liability under both the regimes and choose the one that helps you save your money outflow that would be spent on taxes otherwise.