After a hiatus, the Reserve Bank of India (RBI) raised the repo rate for the first time in May early this fiscal. It was an unscheduled monetary policy meeting and the hike was only 40 basis points (bps). But as it was expected, it was only a start of a long and somewhat painful journey, particularly for home loan borrowers.

The subsequent hikes took place in June, August and the latest one on September 30. Each time, the hike was of 50 basis points. Overall, the repo rates were raised by 190 basis points in the past six months. These rate hikes were followed by subsequent increase in interest rates on loans, as well as on the term deposits of commercial banks.

Wealth advisors have often stated that it is the time to reallocate your portfolio and increase your allocation to debt investment, fixed deposits (FDs) and target maturity funds.

They also say that it is opportune time to invest in the fixed deposits (FDs) to maximise the returns, especially because the financial markets have given subdued returns.

Investors can make note of the following in the wake of rising interest rate scenario:

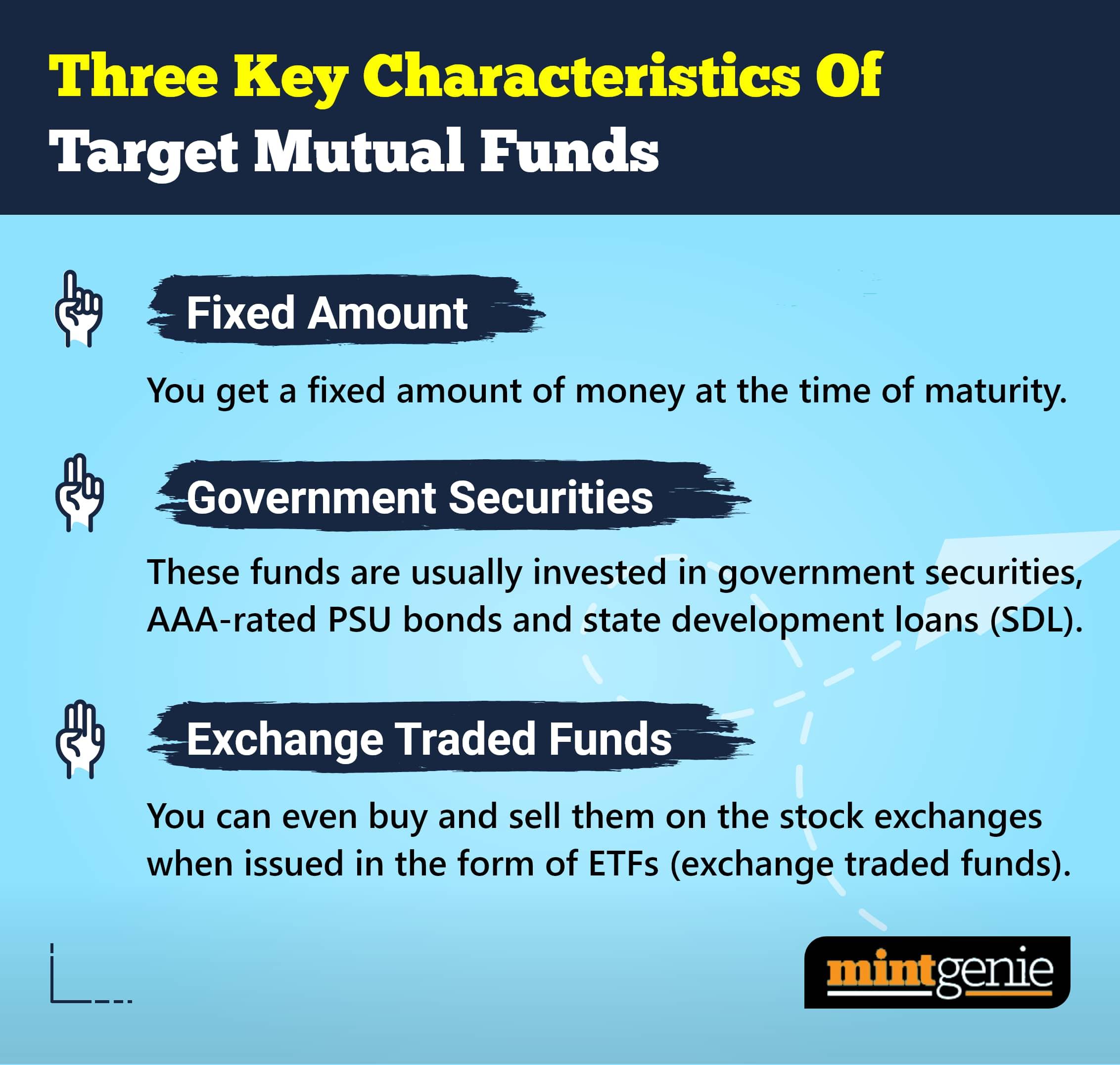

Target Maturity Funds: Target maturity funds are a type of debt mutual funds that have a specific maturity date that invest in the bonds that are included in the underlying index, and hold it till maturity to share the proceeds at a later stage with investors.

These funds predominantly invest in higher rated instruments such as government securities, AAA rated securities and PSU bonds.

Upon being asked whether this is the right time to invest in target maturity funds, Amol Joshi, founder of Plan Rupee Investment Services, says that it is not appropriate to try and time the market.

“It is not advisable to time the market -- be it equity or debt. However, one can still explore the debt funds with a roll down strategy if their tenor matches the timeframe of your financial goals. These funds usually don't face intermittent volatility unlike other target maturity funds,” said Amol Joshi, founder of Plan Rupee Investment Services.

Prepayment of loan: Wealth advisors often point out that consumers can prepay a part of their loan to cut down on your future loan liability.

“If someone has surplus cash, one can do the prepayment to avoid paying a higher interest on loan. By keeping surplus money in the bank or by investing in debt funds does not offer a reasonable return anyway. So, it is the ideal time for loan prepayment,” says Sreedharan Sundaram, a SEBI-registered investment advisor, and founder of Wealth Ladder Direct.

Preeti Zende, SEBI registered investment advisor and founder of Apanadhan Financial services, also shares the similar sentiments.

“Rise in interest rate is taking a toll on debtors particularly those who took loans when the rates were historic low. So, it is vital to prepay the loan as much as possible. And if you prepay in the first seven years, you can save your interest outgo substantially. For this, you can use your annual bonus, quarterly incentives or even monthly extra saving. But investors should ensure that they do not do this at the expense of meeting financial goals,” says Ms Zende.

Debt funds: A debt fund is a mutual fund scheme that invests in fixed income instruments, such as corporate and government bonds, corporate debt securities, and money market instruments that offer capital appreciation.

Debt funds are also referred to as fixed income funds or bond funds. The rising interest rate scenario is seen as an opportune time to invest in these funds.

Fixed deposits: As interest rates on fixed deposits have seen a number of hikes by most commercial banks, although not by the same proportion as repo rates, small investors are advised to explore term deposits as a viable investing option, particularly for allocating the portion of fixed income instruments in their portfolio. Some experts, however, do not agree to this.

“When it comes to term deposits, they still do not offer very high rates. Earlier the rates were around 4.9 percent and have gone up to 5.4 to 5.7, whereas debt yields are up to 7.5 percent. So, when seen from the perspective of indexation and taxation benefits, these funds are better than fixed deposits,” says Mr Amol Joshi.

For the unversed, the RBI increased the repo rates by 40 basis points in May followed by 50 basis points in June, and then again in the month of August. After rates increased by 140 basis points during the three policy meets, the repo rate became 5.4 percent.

Following the latest hike of half percentage point, the current repo rate has now touched 5.9 percent – which is the highest rate in past three years.