It’s raining appraisals this month. Many companies, especially, those in the manufacturing and technology sector have rewarded their employees following good sales turnover and higher profit margins. The announcement of appraisals came at a time when India is battling inflation and the chances of recession are imminent. While you may have the urge to splurge, it would be worthwhile if you plan your next investment opportunity.

Saving your money from tax outgo

A higher income begets more tax liability, so it makes sense to plan your taxes. This can you do by setting aside some of your added earnings in tax-saving instruments. For example, you may start by opening a Public Provident Fund (PPF) account in your name. If you already have one, you may consider putting some money into this long-term fixed income savings scheme offered by the Indian government. You could also consider investing your money in the National Pension Scheme (NPS) or equity-linked mutual fund schemes that earn good returns while shielding you from the added tax burden.

Those averse to risk-taking can invest in National Savings Certificates (NSCs) that offer higher interest rates than bank fixed deposits while being tax-efficient too. Since the government is set to raise interest on Employees’ Provident Fund (EPF) Scheme deposits, salaried employees may invest a higher portion of their money in the Voluntary Provident Fund (VPF) Scheme, thus, securing a higher retirement corpus over the period.

BM Singh, ESOP expert and managing partner, Brajmohan Singh and Associates says, “When you receive the increment, your income tax slab can change. Before receiving your new income, you need to assess its tax implications, how it impacts your slab change and how you can reduce the tax liability. Your first priority should be to plan for additional tax liability after receiving the increment. Therefore, invest additional income received into wealth creation and tax saving instruments such as 80C, 80D and NPS to the maximum extent possible.”

You can divide the appraisal amount in a 30:70 ratio, which means that 70 per cent of the money could be utilized to save on taxes while the rest can be put into non-tax savings deposits or investment instruments. However, if you have exhausted the Section 80C limit allowed under the Income Tax Act, you may as well put the money into NPS that lends an additional tax deduction while earning returns in sync with the market.

Getting rid of liabilities

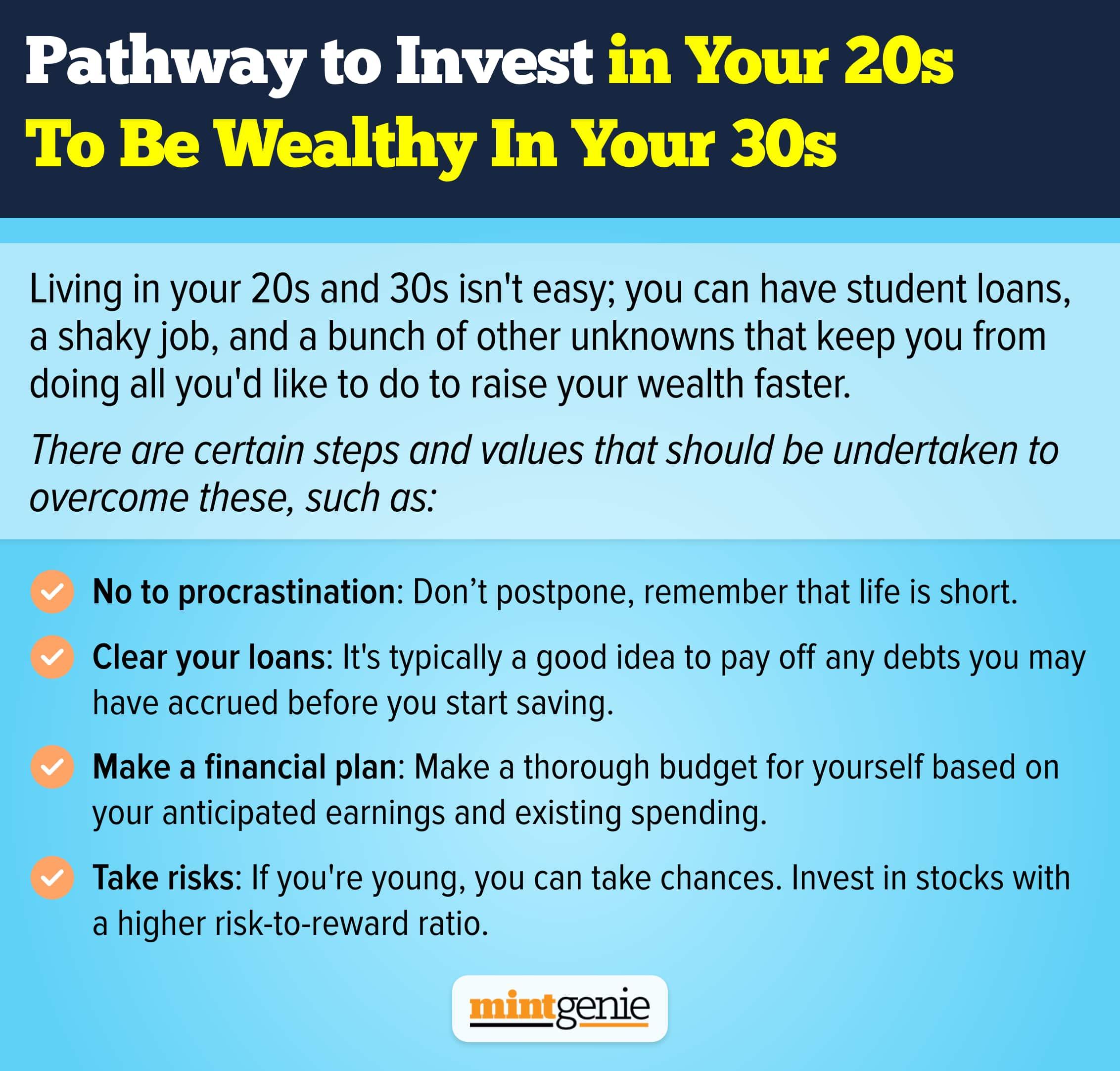

The burden of a loan dampens your investment goals. Many people complain about how they continued to be haunted by the pressure of repaying their education loans. Apart, the young generation fancies new gadgets and automobiles while relying on credit cards to make payments. This explains the recurring liabilities in the form of loans and credit card debt. Any kind of financial planning is futile unless you have got rid of your debt quickly, be it home loans, car loans, personal loans, credit card debt, or any other.

Pratibha Girish, Founder, Finwise Personal Finance Solutions says, “Depends on what kind of loan is being serviced and what rate. If the loan is at a high rate and a short-term one, it makes sense to prepay before investing. The reason being you are borrowing at a higher rate and your investments are unlikely to earn you that much over a short period. However, the same does not hold good for a home loan or a car loan or an education loan - these are long-term and repetitive and usually at reasonable rates of interest, some with tax breaks thrown in. It is not advisable to wait till these loans are paid off to start your real wealth building journey.”

Planning your next move

It is no mean feat to be rewarded and recognized for your appraisals. Celebrating your accomplishments with your family and friends makes it more special. But, do not forget about the long road ahead. Wok on rejigging your investment portfolio by either adding more money into them or by including new investment options. Investment opportunities are galore; it is our ignorance regarding them and how they work that causes us to lose out on the prospect of earning higher returns.

Let us understand the same using an example.

Assume a 30-year-old tech guy is ecstatic about his first appraisal but is equally unsure about how to invest the same. He scratches his hand while choosing between the risk versus returns quality characteristic of equity versus the stability of debt funds and hybrid instruments.

Viral Bhatt, Founder, Money Mantra says, “He should first think about what he wants to achieve with his investments. If his financial goals are not for the short term, he should then opt for maximum allocation into equities. However, if he intends to have some money in the immediate future, he should first work on a contingency fund to cater to sudden emergencies before proceeding to allocate 20 percent of his money into debt and the remaining 80 per cent into equities. If he has short to medium term goals, then he might allocate 20 to 30 percent in hybrid mutual fund instruments as well.”

Building wealth

Living in a society does entail economic obligations. The philosophy of money is to ring in personal freedom, which is not possible without financial freedom. Adequate finances bring in a sense of independence too, which is why allocation of money into all kinds of instruments including exchange-traded funds (ETFs), mutual funds, stocks, gold, fixed-income plans, pension plans, insurance schemes and real estate investments becomes important. However, allocating and reshuffling these investment opportunities from time to time depend on how quickly you are looking to attain that much desired financial independence and risk appetite.

Do not underestimate or overestimate your ability to take risks as it would determine your response to continued market fluctuations. Volatility is inherent to the market, which means that if you are gunning for high returns, you must be willing to take the risks in your stride. That off-and-on bumpy ride will lend you excitement and frustration in equal measure. Remember that it takes time to build wealth, so rushing through your investments without giving a second thought to them will do more harm than good.