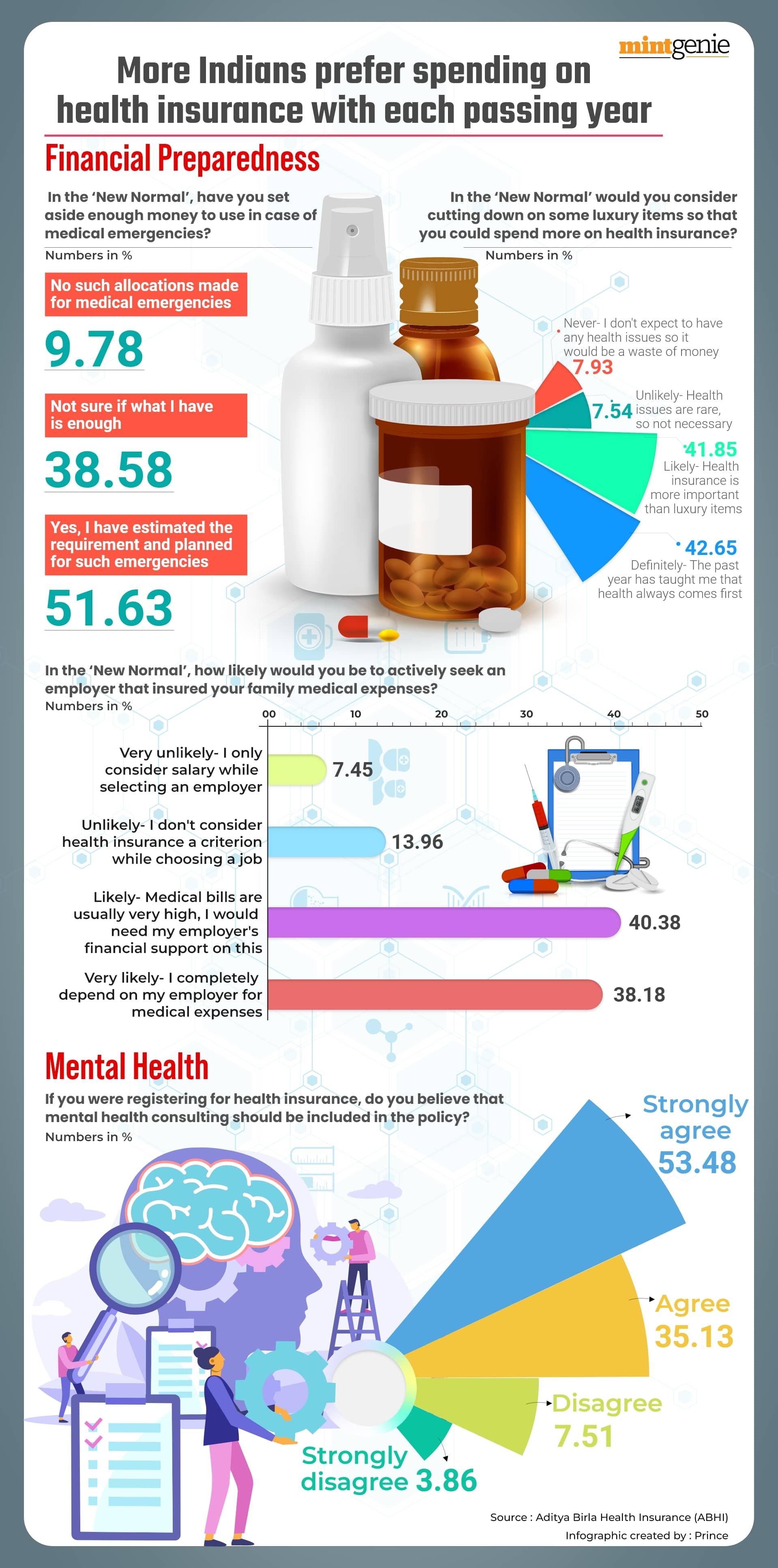

Health insurance has become a high priority financial risk mitigation measure for individuals as well as families. Hospitalizations of family members during Covid-19 showed how grossly unprepared many were financially to meet hospitalization expenses.

While the pandemic has led to the increased awareness around health insurance and the health insurance industry has seen a tremendous growth, it is important that everyone understands the fine blueprints of the policy cover they have availed in order to avoid any possible claim rejection by insurers.

According to the IRDAI Annual Report of 2022, 6.42% of health insurance claims of general and health insurers were repudiated during FY21-22. While a claim might be rejected for numerous reasons, finding yourself in a situation like that can be stressful, especially during hospitalization of near and dear ones and when you need the most financial comfort.

>>Also Read: 8 reasons to buy a health insurance plan

Avoiding rejection of claim

So, as a policyholder, what can you do to ensure you don’t find yourself in a situation like this? Here are a few things to keep in mind:

· Understanding the policy terms: Before buying health insurance cover, read the product literature and especially the policy wordings carefully. Please keep in mind that availing health insurance does not automatically constitute you being paid the entire hospitalization amount or the coverage amount specified in the policy. Every cover offered by an insurer is subject to general terms and conditions as well as specific terms and conditions applied by the insurer on the basis of the disclosures made to the policyholder. This could range from certain restrictions on types of procedures, waiting periods on some specific illnesses or any pre-existing diseases, capping on room rent or zone/city you are based out of, different types of co-payment, among others. So, before you buy a health plan, make sure you read and understand these terms clearly.

· Disclosing all health-related information: Health insurance contracts are also governed by Uberrima fides, a Latin phrase meaning utmost good faith literally or most abundant faith. When you buy a health insurance plan, the insurer may ask you to disclose all health-related information, including details of any pre-existing diseases, smoking and drinking habits, family’s health history, among others. Not disclosing or mispresenting this information when buying a policy could be a ground for claim rejection. Hence, make sure all details are disclosed to the insurer in a fair and transparent manner in the proposal form.

· Submitting claim on time: Many people assume that they can raise a health insurance claim any time after they are discharged from the hospital. However, insurers may have stipulated a timeline within which the claim should be intimated, which may range from 15-90 days. Filing a claim beyond the stipulated time period can lead to claim rejection unless the claimant can provide cogent reasons for delay in intimation. For any cashless hospitalization for planned procedures, it is advisable that you inform the insurer in advance. Timely intimation to the insurer ensures that cashless hospitalization is approved, and the treatment can be carried out without any financial hurdle. So, make sure you collect all the relevant documents and file your claim at the earliest.

Redressal mechanism for claim disputes

A claim getting rejected can be extremely frustrating. This is especially true if you feel your claim intimation has not been treated fairly. However, as the insurance industry is a regulated sector, the Insurance Regulatory and Development Authority of India (IRDAI) has put certain mechanisms in place in order to ensure any grievances of the policyholder are addressed in an efficient manner. Here are few redressal mechanisms available to you:

Reaching out to the insurer: If you think your claim has been rejected on unfair grounds, you can first write to your insurer to reconsider their decision. In this case, the insurer again reassesses the claim decision. In case you are not satisfied with the decision, you can approach the Grievance Redressal Officer (GRO) of the insurance company. The GROs of every insurance company work independently and assess the case afresh. There are also regional GROs appointed by the insurance companies in every branch office. The GROs are required to resolve your grievance within two weeks of receiving the complaint.

Approaching IRDAI’s Grievance Redressal Cell: If there is no response from the GRO within two weeks or you are still unsatisfied with the resolution provided by the insurer, you can approach the Grievance Redressal Cell of the Policyholder's Protection & Grievance Redressal Department of IRDAI. You can do this by directly going to the portal named ‘Bima Bharosa System’ (www. bimabharosa.irdai.gov.in). You can also e-mail or call them to register your complaint. However, keep in mind that only complaints raised directly by the insured or the claimants are entertained by Bima Bharosa.

Approaching the Insurance Ombudsman: After exhausting the insurer’s grievance redressal process, if you are still not satisfied with the decision of the insurer, then you can lodge a complaint with the Insurance Ombudsman based on the territorial jurisdiction of the insurer or your residential address. One can find details of the Ombudsman by going through the policy document or visiting www.cioins.co.in. You can lodge the complaint with the Ombudsman within one year from the date of rejection of representation made by insured/claimant to the insurer or if the insurer fails to address the representation made to it in a month. The Ombudsman is authorised to take complaints for loss of up to ₹30 lakh. If both the complainant and the insurer agree to mediate, the Ombudsman is required to issue the recommendation within one month and insurer has to comply within 15 days of the receipt of the same. Otherwise, the award is supposed to be passed within three months of the receipt of all requirements from the complainant. If award has been passed against the insurer, then insurer has to comply the same withing 30 days of the receipt of the award.

Other ways for redressal: You can explore other legal remedies as well like going to the Consumer Dispute Redressal Commission present at district level within 2 years of denial of the claim or approaching the relevant court based on its territorial jurisdiction as provided by the law.

It is the responsibility of the insurer to address any grievances of the policyholder in a timely and fair manner. The regulator IRDAI has also put strong mechanisms in place to ensure consumer rights are taken care of. Just like any other industry, it is natural that customer grievances might arise from time to time. It is the duty of the insurers and the industry as a whole to educate the customers on all the redressal means available to them. Customers, too, should be well aware of the policy terms to avoid any unnecessary claim rejections. Making the entire dispute resolution mechanism accessible and more transparent will aid in reducing overall insurance complaints and lead to increased trust levels among insurers and customers.

Rasika Kuber is the Chief Compliance Officer of Go Digit General Insurance. Views expressed are personal.