A PPF savings scheme has a 15-year maturity, but if your PPF account has been inactive for a while, you can restart it after following the procedure prescribed.

To reactivate a dormant PPF account, the account holder must submit a written request together with a deposit of ₹500 for each year that the account has been inactive. In addition, a penalty of ₹50 is levied for each year of inactivity.

Your account will become inactive if you do not make at least the minimum deposit amount in any year of your PPF term. If you’ve invested in a variety of options, it’s simple to lose track of a financial instrument. Due to the fact that not paying the deposit in any given year might occur for a variety of reasons, the authorities have made it simple to reactivate a dormant PPF account.

An inactive account will still pay you interest until it matures according to the terms, but it has significant drawbacks. For one thing, you can no longer take out loans against your PPF account, which could be an issue if you need cash in the near future. You will also be unable to make any premature withdrawals until you reactivate the account.

Steps to follow

These are the steps one must follow:

- The account holder must submit a written request to the bank or post office branch where the account was opened to have an inactive PPF account revived. The application can be submitted any time during the account’s 15-year tenure.

- For each financial year during which the account was inactive, the investor will be made to deposit a minimum of ₹500. Along with the application, the cheque must be delivered to the branch.

- For each financial year in which the account was dormant, the bank or post office levies a penalty of ₹50 to revive the account. Along with the payment of arrears, the penalty must be deposited.

- To finish the verification process, return to the PPF account branch.

Your account will be enabled as soon as these steps are followed. You must also reactivate an account that has matured while it has been inactive by following the steps outlined above. The account's proceeds will be frozen until the account is reactivated.

For example, you’ve reached the tenth year of your PPF investment. You deposited ₹500 and above every year for the first seven years but were unable to do so for the last three years due to a variety of factors.

To reactivate the account, you must pay the following fees:

- For each fiscal year, there are ₹500 x 3 = ₹1,500 in arrears.

- For each fiscal year, the penalty is ₹50 x 3 = ₹150.

- Furthermore, you will be required to make a minimum deposit of ₹500 for the new fiscal year, which is the PPF's 11th year.

Having paid the penalty and arrears, your PPF account would be restored.

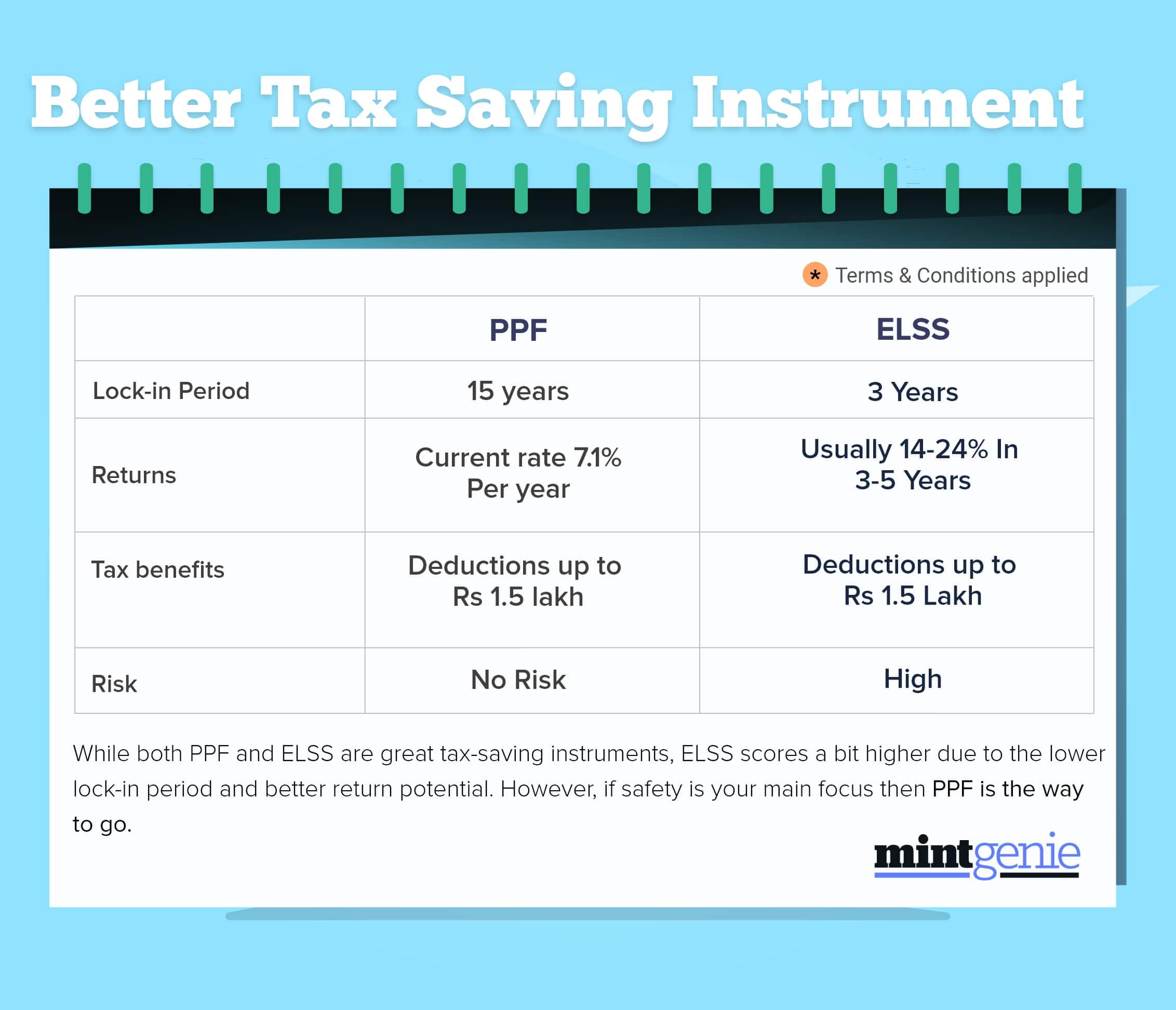

The Public Provident Fund (PPF) is a popular fixed-income investment option among investors. Individuals can invest up to ₹1.5 lakh in a PPF account each year and get a tax deduction under Section 80C of the Income Tax Act. The account has a 15-year validity period, and the account holder must deposit at least ₹500 per financial year.

The bank or post office will charge you a penalty of ₹50 to revive your PPF account if it has been inactive for more than one financial year.