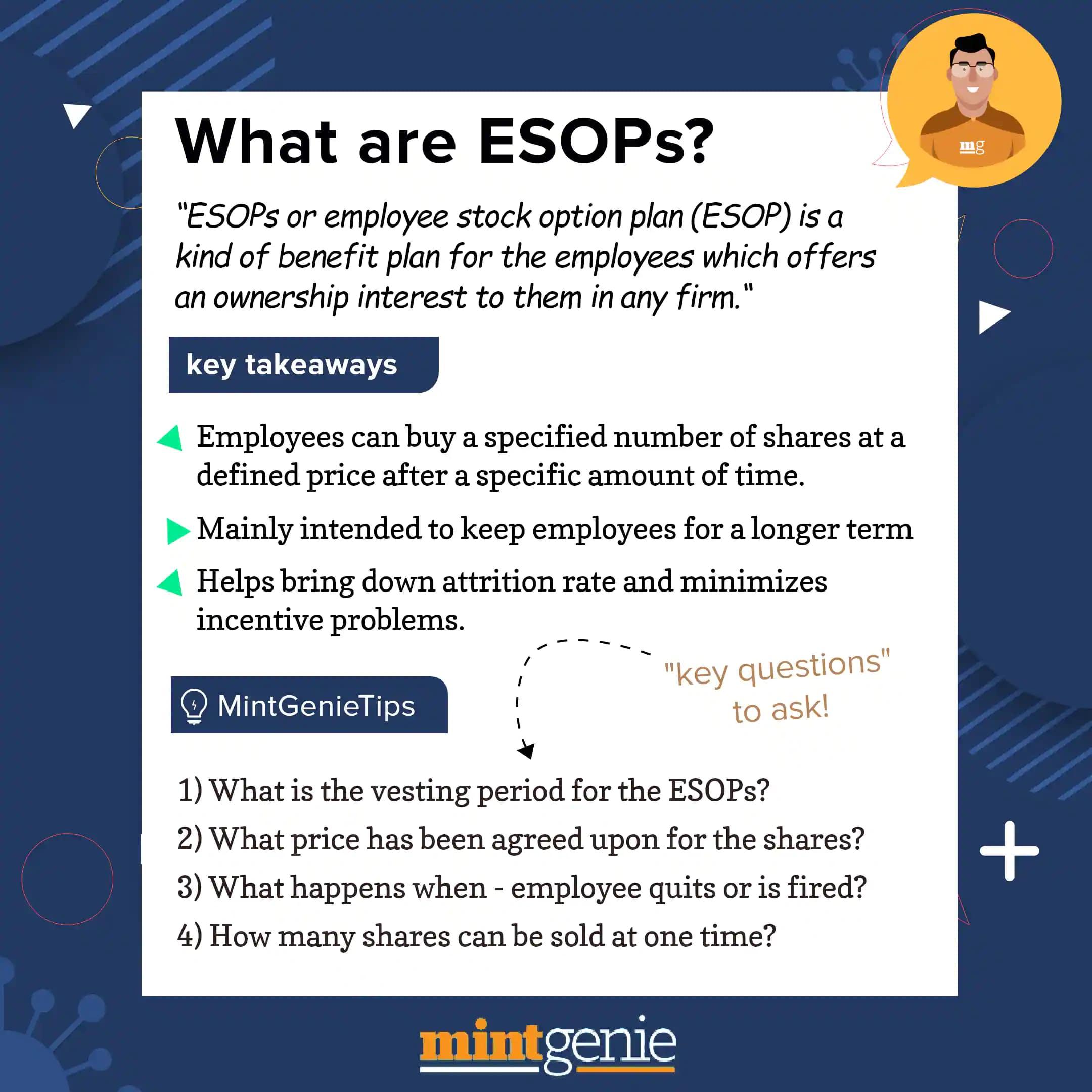

Employees Stock options (ESOPs) are one of the tried and tested ways to reward employee for their hard work, sincerity and loyalty. Some employees exercise these options but don’t sell the securities immediately, while a few do the both.

Often times, ESOPs facilitate start-up founders to make hay during a fresh round of fund raising or even during company’s listing. It is interesting to note that Paytm’s founder Vijay Shekhar Sharma was given Employee Stock Options (ESOPs) that raised his stake in the company by anywhere between 2 to 3 percent in run up to the company’s IPO, as per a media report.

According to the report, the payment wallet firm had more than doubled its ESOP pool to around 61,094,280 equity options of face value Re 1 each from 24,094,280 equity options ahead of the $2.2 billion worth IPO.

As ESOPs can bring a windfall of money for employees and co-founders, it is vital to understand the income tax treatment of these options. Let us understand this in some detail:

The stock options are taxed twice. At the outset, the taxation happens when options are exercised and the next time, the ESOP beneficiaries are meant to pay tax on capital gains when the securities are sold.

“In the year of exercising, ESOPs are treated as perquisite and taxed under income from salaries, the difference between acquisition cost and fair market value (FMV) is the taxable amount. The listed companies’ FMV is the average of opening and closing prices on the day of exercise whereas in case of unlisted companies, the fair market value is decided by a merchant banker,” says Deepak Aggarwal, a Delhi-based chartered accountant and financial advisor.

Capital gains tax is levied when the shares are sold. In this, the tax is be levied on the difference between the proceeds and the fair market value when ESOPs are exercised. The time period of holding determines whether it is long-term or short-term capital gain.

For example, Mr A of a listed company is given ESOPs of 500 shares at ₹100. On the date of exercise of option, the lowest price of shares was ₹100 and highest was ₹110 so the fair market value will be ₹105; the taxable amount will be (105-100) x 500 = ₹2,500. This will be taxed under salary income.

Now let us suppose, Mr X held those shares for longer than 12 months, it would be treated as long-term capital gains and income will be taxed at the rate of 10 per cent whereas short term capital gains attract a tax rate of 15 percent on the gains above ₹1 lakh.

Two years ago, the government gave a leeway in the budget 2020 that enables employees of certain some start-ups under section 80IAC to defer their tax liability on allotment of shares to 48 months from the applicable assessment year after exercising the right.

However, if the employee leaves the job before 48 months lapse, or happens to book the profit by selling the shares in the market, then the income tax will become due during the year he quits or sells those shares.