When a small investor looks for protection of their deposit, they tend to choose a big commercial bank which does not pay a high rate of interest. The average annual rate of interest on a fixed deposit ranges between 5 to 5.5 percent.

On the other hand, when an investor looks forward to earning a higher rate of interest, then one might have to choose a small bank or an NBFC where there is a relatively higher risk of capital.

The recent untoward events relating to cooperative banks and defaults by NBFC did not set a happy precedent, especially for small investors.

Dewan Housing Finance defaulted on principal of secured debentures of ₹50 crore in July 2020 and RBI imposed restrictions on depositors of Punjab and Maharashtra Cooperative (PMC) Bank in September 2019. These may be one-off incidents but they are certainly strong and conspicuous enough to send a chill down the spine of small depositors who keep their retirement savings in these banks.

The small investors must be aware that their deposits up to ₹5 lakh are safe in banks, and are insured by the DICGC (Deposit Insurance and Credit Guarantee Corporation).

The latest amendments in DICGC Act which came into force with effect from September 1, 2021 give a further impetus to small depositors.

Earlier, in case of liquidation of a bank, the insurance money to be given to depositors was the responsibility of the bank's administrator. But with the new rules in force, it shifts to DICGC, which is RBI's subsidiary.

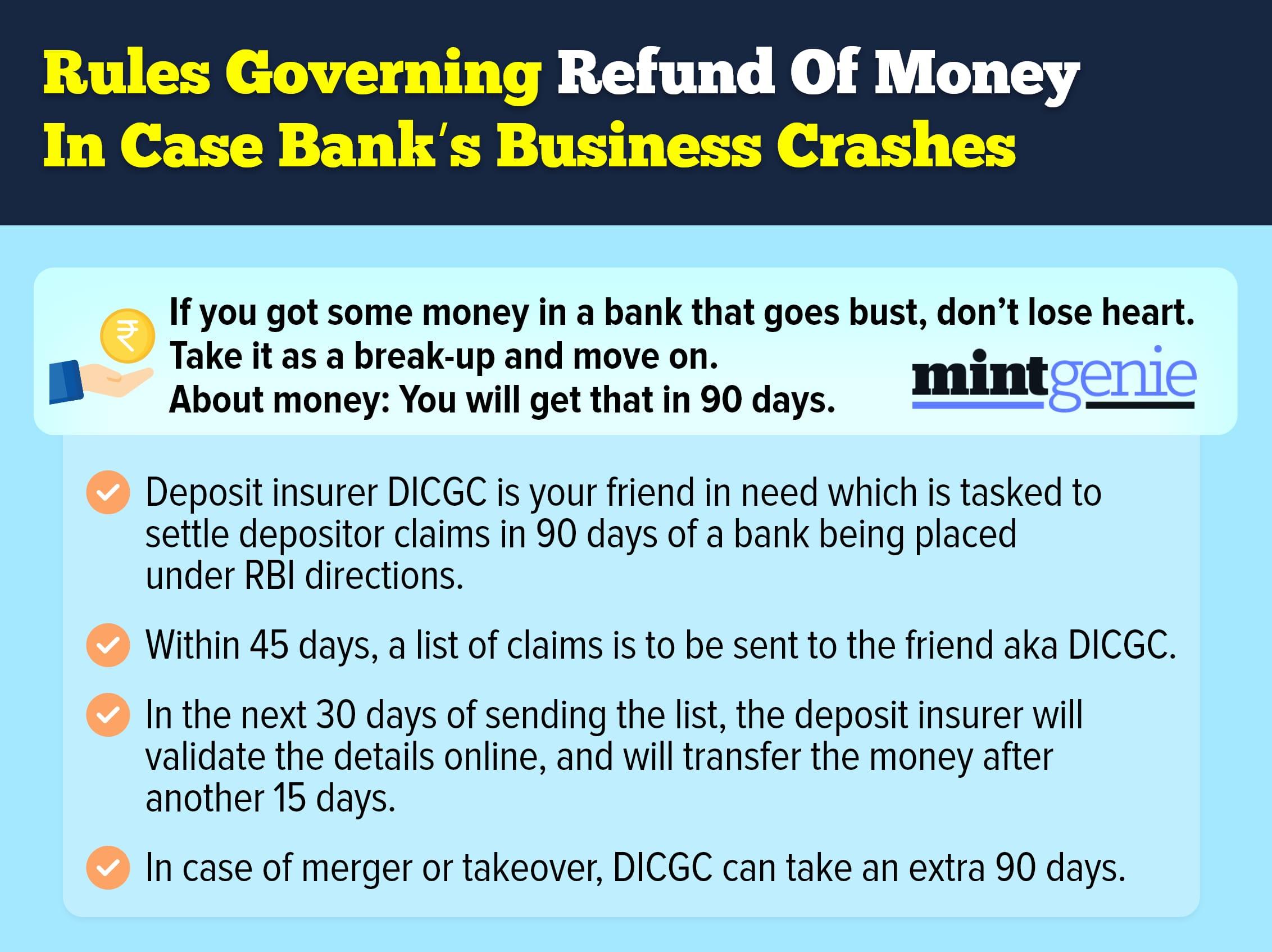

Time taken to transfer money

Although the rules enable depositors to receive their money up to a maximum of ₹5 lakh in case of bank’s liquidation. But it can take a long time before the money is finally released by the bank because of procedural and legal formalities.

Sample this: In 2019-20, it took on an average 508 days for the depositors of banks that went bankrupt to get their money. A year earlier, it took 1,425 days for the liquidated banks to disburse money to the depositors.

Now, DICGC is supposed to settle depositor insurance claims in a maximum of three months of a bank being placed under RBI directions.

As per the new rules that came into effect from September 2021, the process would begin as soon as the RBI passes directions on a bank, and within 45 days of these directions, the bank must send a list of depositors and their claims to the DICGC.

Later, in a span of 30 days after receiving the list, the deposit insurance corporation is meant to validate the details online, and to transfer the money after another 15 days.

However, if the central bank is working on a merger or takeover of the bank, DICGC can take an extra 90 days over and above the scheduled deadline.

Look beyond big banks

Since the rules apply uniformly to all commercial, cooperative and small banks, the depositors can look beyond the big banks if they are looking for a higher rate of interest.

Also, they must make sure that they do not keep more than ₹5 lakh in a small bank that might face a risk of liquidation in near or distant future.

However, the experts warn that the small depositors should not take risky bets by depositing money with not-so-credible NFBCs. “One can explore small commercial banks because they are regulated by the banking regulator – RBI, instead of a cooperative bank which are partly controlled by the state government,” says Deepak Kumar Aggarwal, a Delhi-based financial advisor and chartered accountant.

So, next time when you want to zero in on a bank for opening a fixed deposit account, make sure that your money will be safe there as well.