Akshay Bhatt earns a handsome salary as a data science professional and aims to retire in his late 40s. To meet this goal, he has already created a wide-ranging portfolio comprising stocks, mutual funds and fixed income instruments. But lately, he has been worried because he is unable to invest at a frantic pace at which he used to do earlier. The only thing that has changed in his spending pattern lately is that he has started to use his credit card in a more liberal way.

Just as Bhatt, if you are also accustomed to using credit card(s) for the payment of most of your bills, then make sure that you clear your bills on time. Rolling over your credit from one card to another looks convenient but can hamper your financial plans in the future.

When you have an income of ‘X’ amount and the expenses nearly 70 percent, you are supposed to save the remaining 30 percent and invest the same in order to meet your financial goals. In that case, whatever you borrow over and above this will come from the pie of savings i.e., 30 percent – thus pushing the can of your financial goals further down the road.

To prevent this from happening, it is important to make note of some factors. One should consider the following points with regards to credit card usage:

1. Needs versus wants: Use credit card for an amount you need and not because the credit is available. If an urgent need could arise for an amount anywhere between ₹2 and 3 lakh, then you should keep that as a safety valve which you can use on a rainy day. Do not assume that you can spend this sum on avoidable expenses without impacting your financial soundness.

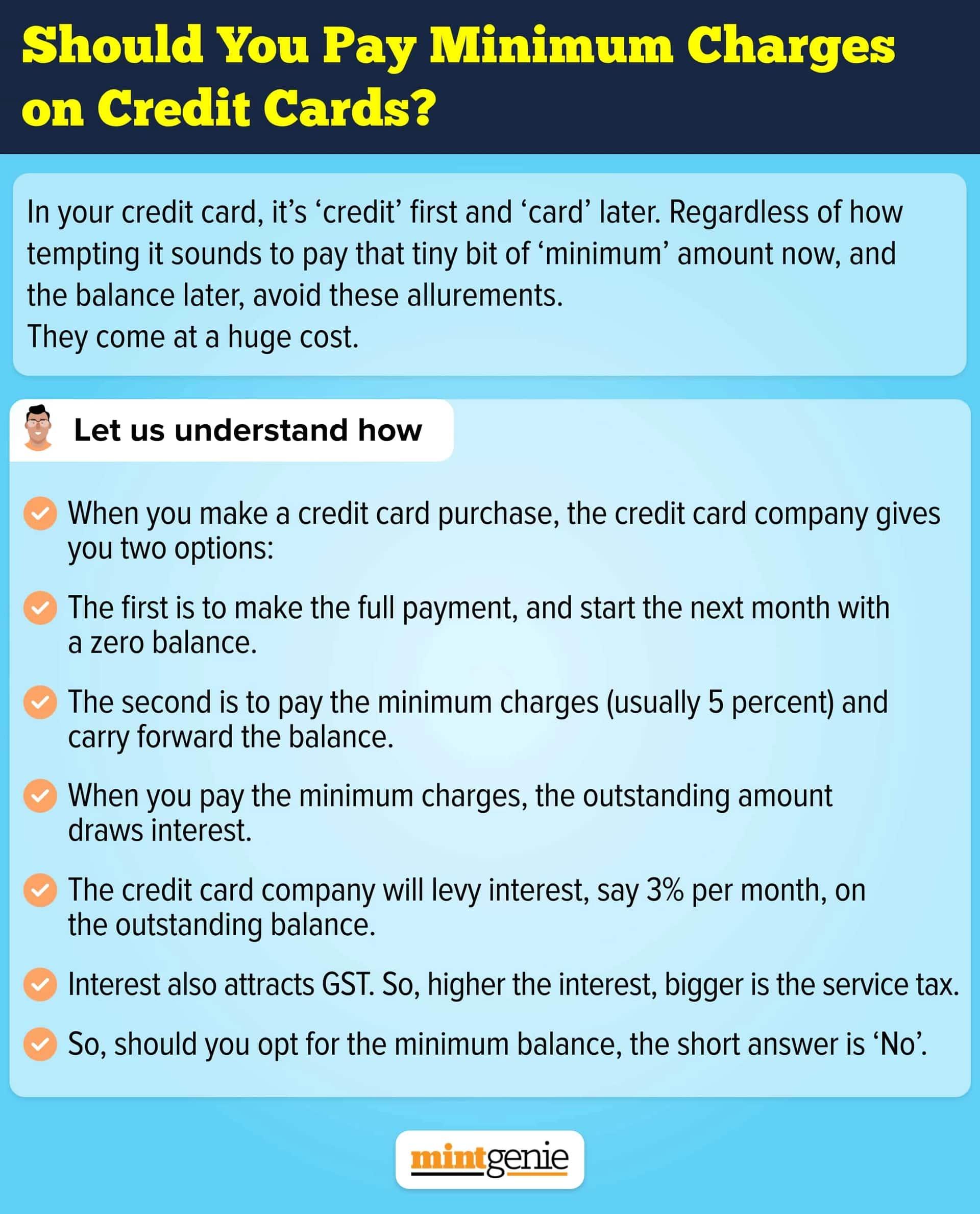

2. Rolling over credit: Rolling over credit to the next month may not be too bad but once in a while. However, one should not assume that clearing minimum balance is enough to navigate through the debt of credit card. It’s important to note that the credit card debt accrues interest on the balance not paid.

“Credit cards are only good if you can pay your full bill within the given time. If you do not clear your dues by your billing due date, the amount is carried forward and interest is charged on it. Credit card interest rates are quite high, with the average rate being 3 percent-4 percent per month, which would amount to 36 percent-48 percent per annum,” Rohit J. Gyanchandani, managing director, Nandi Nivesh Private Limited, said in an opinion piece for MintGenie here.

3. Number of credit cards: Sometimes it is okay to hold more than one credit card in order to keep a high credit score. As suggested by credit experts, it is better to take multiple cards and use a portion of each of them in order to keep a high credit score.

Although one can, but should not exhaust the credit limit of all credit cards combined. For a good credit score, one should refrain from spending more than 30-40 percent of credit limit of each card.

4. Opportunity cost: One of the ways to look at the money spent via credit card is in terms of opportunity cost i.e. the amount of investment that is foregone as a result of those avoidable expenses. In other words, if a consumer does not spend money on buying that extra piece of clothing or a new luxury watch by using the credit card, the money would have gone into one of the investment instrument, thus helping meet the financial goal faster.

“Some of the consumers do not realise that spending ought to be done after keeping aside the saving money, and not the other way round,” said Deepak Aggarwal, a chartered accountant and financial advisor based in Delhi.

5. Losing sight of the goal: Sometimes consumers start using a credit card to improve a credit score in run up to raising a loan later. However, the saving one can expect to make in terms of lower interest rate (after high credit score) should be more than what one would spend on credit card usage.

For this, it is vital to remember that credit card is accompanied with a host of expenses such as joining fees, late payment fees, processing fees and renewal fees. When one foresees less savings than these expenses, it is futile to take a credit card merely to improve the credit score.

So, it is vital to remember that credit card works like a permanent credit line which one can use as and when the need arises. It is not meant to be used for the impulsive purchases that are avoidable.