Budgeting is the handiest financial tool that serves myriad benefits without any risk involved whatsoever. No one is ever too young to start budgeting, even if you are not earning you can budget your pocket money and plan strategically to save for that new dress you want to buy.

Building a budget

A budget should ideally be a simple plan that you can follow without any hassle. It should be easy to follow and have room for adjustment in case something prompt comes up. There are many ways to budget. You can create a budget digitally through spreadsheets, mobile apps, etc or you can go for the conventional pen-paper approach- whatever is comfortable and can be referred to anytime.

However, you may choose to note your budget, let’s go through the steps to design an effective one.

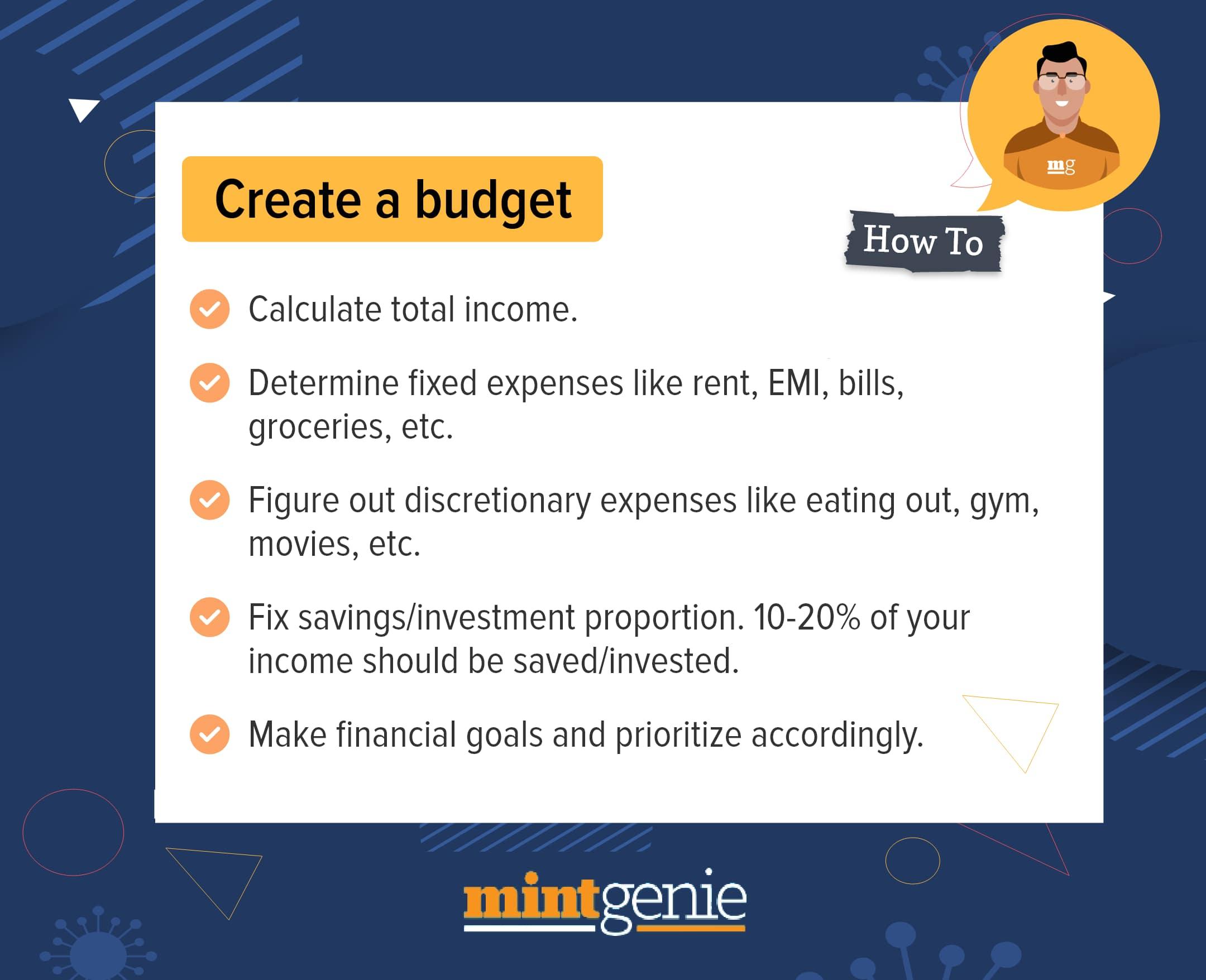

1. Calculate your income: Before anything else, calculate the net income of the time frame (preferably one month) you’re building your budget for. Enlist all your sources of income and add the after-tax income to total your net income. If you’re salaried, don’t forget to add income from any freelancing or side-hustle that you might be doing.

Calculating your income correctly is the most important step in creating a budget as it serves as a reference point around which the whole budget will be built. After all, budgeting is nothing but managing your money in the best way possible.

2. Determine your regular expenses: This includes how much you would need to fulfill basic needs like rent, groceries, insurance payments, and other monthly costs in terms of subscriptions, cell phone plans, etc. These are the basic necessities that have a fixed sum. Once you have listed out the fixed expenses, average the cost for variable basic expenses such as electricity bill, petrol/diesel expenses, water bill, and similar costs.

Since the variable costs tend to fluctuate, it is important to leave a little room for these fluctuations in your budget lest make it too restrained and not being able to follow it.

3. Demarcate saving/ investment proportion: It is imperative to take out a certain portion from your income for saving and investing. This serves in multiple ways like ensuring a retirement income, extra returns through investment, fulfilling a goal like buying a house, etc.

To inculcate financial discipline for allocating a sum for saving and investment, you can try the widely accepted 50/30/20 thumb rule of budgeting. According to it, 50% of your income should go towards fulfilling your basic needs, 30% towards entertainment expenses and luxuries, and 20% towards savings and investment.

4. Outline goals and prioritize: Outlining and prioritizing goals will assist you in making decisions throughout the process of budgeting and executing the budget. After you note down your financial goals, you'd better be able to earmark funds towards your reserve and investments in financial securities.

Managing a budget

Most people who wish to lead a financially disciplined life to overcome the first step of drafting a budget but stumble when it comes to managing and adhering to the budget. Here are some tips that will help you to execute your budget plan better.

1. Create an emergency fund: Many people forget about budgeting or their plan when an emergency or an unforeseen circumstance arises. This essentially makes the financial conditions worse for people. Thus it is very important to create an emergency fund that can support you in such situations.

An emergency fund should equal around 3-6 months of your income. It can be built by taking a small proportion of your income until you have enough to suffice in a crisis.

2. Avoid over-expenditure: Avoiding over expenditure and unnecessary purchases is key to carrying out a budget successfully. If you overspend and exceed your budget in one month, you’ll have to cover the deficit in the next month leaving you less money to meet your basic needs, again leading to exceeding your budget and thus pushing you into an inevitable vicious cycle.

This can be avoided by creating a shopping list in advance and buying only what is affordable. As the elasticity of demand necessities is low, you can cut back on goods that are superfluous.

3. Save first, spend later: The save first and spend later approach is gaining popularity these days. It is especially beneficial for individuals trying to develop the habit of saving. It is quite simple and can be followed by fixing a percent or an exact amount you want to save each month and separating it as soon as you receive your income.

To ensure that you don’t spend your savings you can deposit the sum in a separate account or invest in a liquid asset so that the money is accessible but does not mix with your expenditure income.

4. Review your budget: The importance of reviewing your budget regularly cannot be stressed enough. It is the most common mistake that people make. It helps to cover deficits of the previous months, adjust according to new circumstances like a wedding in the family, or revised rent, increase in income as a result of a promotion, etc. You’ll also be able to efficiently track your spending through this exercise.

These are not hard and fast rules that should be followed under any circumstances but a basic framework for you to create the right plan for yourself. You can tweak according to your own priorities so that the plan is simple and doesn’t stress you out.