Equity markets in India and across the world have been volatile since the past 18 months. Investors have not made any returns in equity markets during this period and are frustrated with the sideways movement of the markets. There is some sign of relief for investors investing through a systematic route of investment like SIP/STP. However, the overall experience hasn’t been great.

Rising interest rates have made the debt category more interesting as the yields have gone up from 4% to 8% even in the short duration schemes. Going forward, unless the inflation comes under control, the markets might not deliver double digit returns in the short term. However, there are ways to invest in equities without facing a bigger drawdown on the entire capital and still generating decent returns on portfolio level.

In this article, we are going to discuss two different ways of deploying your money in equity markets that will help you reduce volatility and enhance returns over a longer run.

Systematic transfer plan (STP) is a method of investing where a lump sum investment is parked in the debt mutual funds and a certain portion of the scheme is shifted to equity funds. The frequency of transfers can be daily/weekly/monthly/quarterly/yearly. The process is automatic where you can set a pre-defined date for STP & it keeps on happening until you stop the trigger.

Let us discuss two strategies that investors can use to reduce portfolio risk & capture the upside in equities.

Strategy 1

Under this strategy, principal amount is invested in a debt mutual fund. The appreciation part of the investment is transferred automatically to an equity-oriented fund at monthly intervals. Over the medium to long term, higher expected returns in equity funds enhances the overall return of the total investment.

This strategy may be suitable for investors looking to beat FD returns along with reasonable safety of invested amount (since the money is always parked in a debt fund). This strategy involves transfer of appreciation components to equity funds, hence the principal amount is not exposed to equity markets.

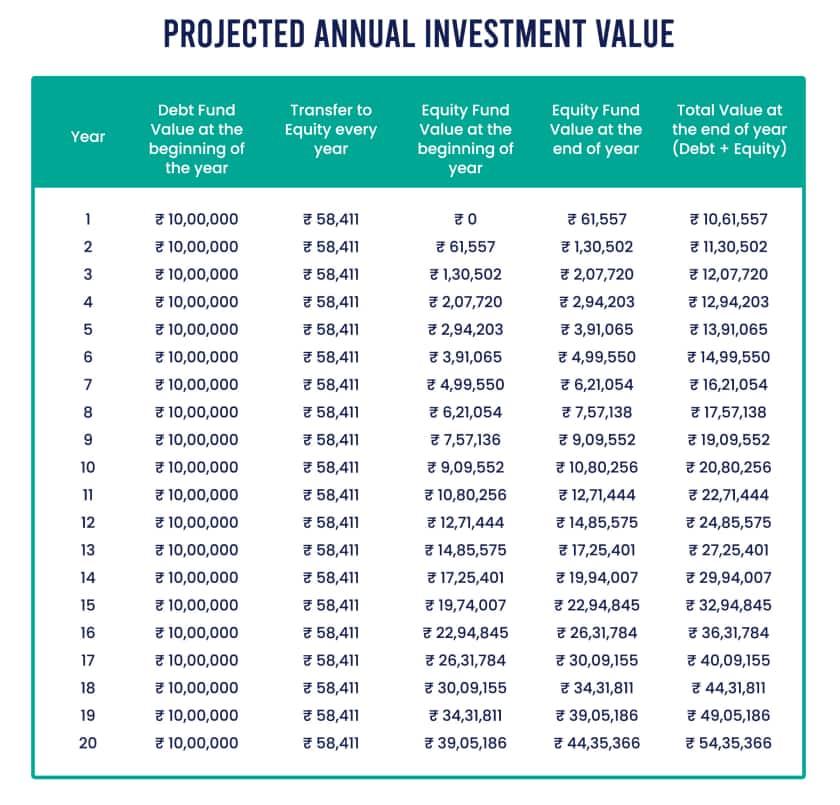

Hypothetical example:

- Initial investment in debt fund: Rs. 10,00,000

- Debt fund YTM: 6%

- Equity fund returns: 12%

- Transfer: Monthly basis

- Mode: Capital appreciation only

- Period: 20 years

The projected year-wise value is as follows:

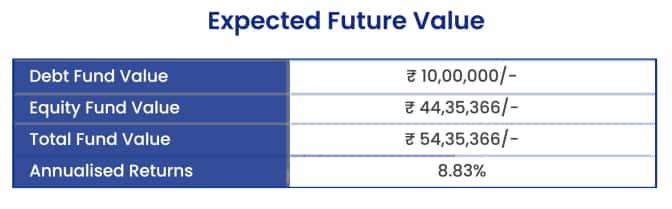

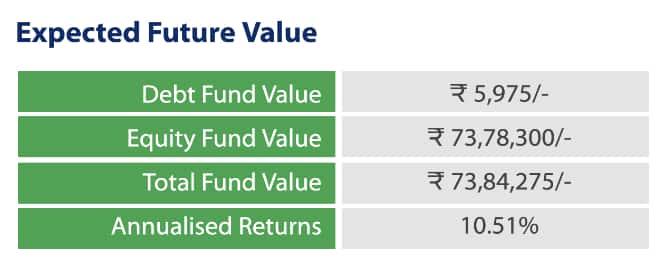

Expected future value is:

This is achieved by keeping the principal intact and moving only the appreciation portion of the investments into equity funds.

Following are the benefits of this process:

- Potential to generate better than FD returns.

- Lower taxes than FD as debt mutual funds have indexation benefits.

- Liquidity is available, the schemes can be redeemed anytime.

- Profits can be booked when markets are high and vice versa.

- Partial withdrawals are possible.

- Principal investment is never exposed to equity risks.

Strategy 2

Under this strategy, principal amount is invested in a debt fund.

Every month, 1% of the principal amount is transferred from debt fund to equity fund. This helps in averaging the cost of equity fund units. Since the transfer amount is small (just 1% of invested amount), any major fall in the markets in the short term doesn't hurt badly.

Over the medium to long term, equity markets tend to deliver better returns than debt markets, and therefore the return of the total portfolio can go up. This is suitable for investors looking to benefit from equity markets over a long period but do not want high volatility on their total investment in the short term.

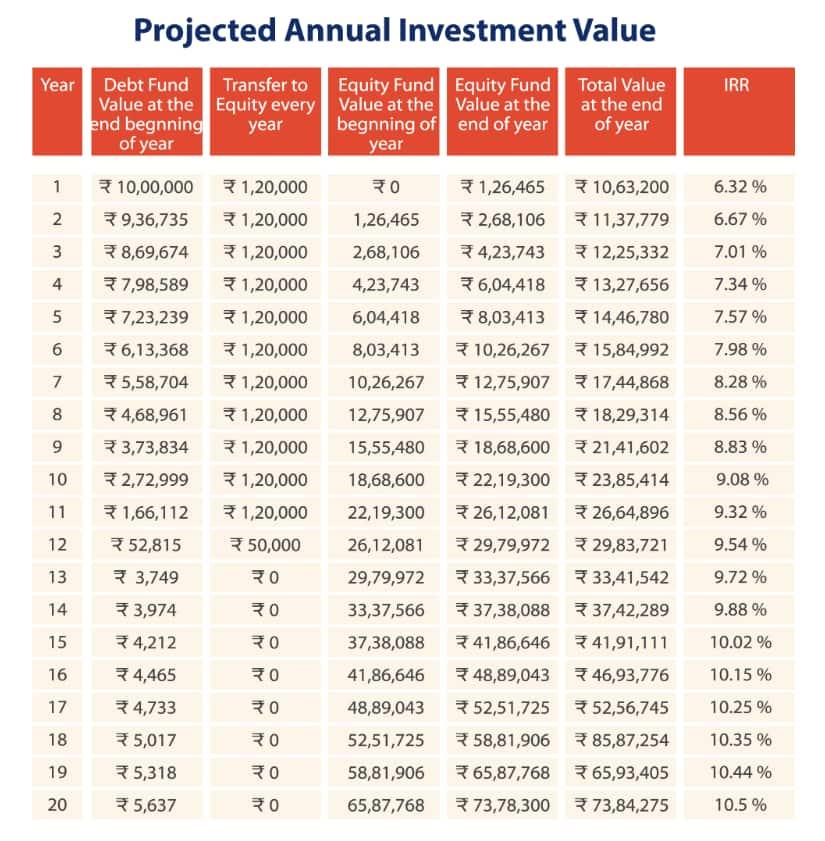

Hypothetical example:

- Initial investment in debt fund: Rs. 10,00,000

- Debt fund YTM: 6%

- Equity fund returns: 12%

- Transfer: Monthly basis

- Mode: 1% of initial investment

- Period: 20 years

The projected year-wise value is as follows:

Expected future value is:

This strategy is perfect if one wants to take long term exposure to equity but wants to iron out any short-term volatility in the market. Entire corpus is broken down into small pieces and deployed to ensure rupee cost averaging and the balance amount keeps on earning debt returns till the money is shifted to equities.

This is a very flexible strategy. One can make necessary changes in between too if the market provides opportunity. Since switching is easy, if the market corrects heavily, the debt can be deployed to equity in a much more accelerated manner. Also reverse can be done by booking profits out of equities and deploying it in debt when interest rates are higher like in the current scenario.

TIP: This is a long term strategy and suitable for investors who don't want to get into too much churning and management. Hence, schemes should be selected on the basis of consistent track record over different market cycles. Debt mutual funds have interest rate risk, it is suggested to stick to short duration/low duration funds along with consistent flexi cap funds to ensure smooth investing experience.

Rohit Gyanchandani is Managing Director at Nandi Nivesh Private Limited