Everyone wants to earn some extra money. But then the stock markets threaten many newbie investors with their constant volatility. Mutual fund investments serve them best. While it helps to have experienced fund managers using your funds, many new investors tend to be afraid of sticking to their mutual fund investments. Mutual fund investments when continued for a prolonged period yield good returns though the quantum of returns depends on the fund chosen, investments made and the tenure for which they were held.

How to get the maximum out of your mutual fund investments

TL;DR.

Mutual fund investments can help you create the much-needed corpus, provided you are ready to adhere to certain necessary rules. Most importantly, investing must be an informed and disciplined decision to ensure that you are able to make the most of the money you have invested in various funds depending on your financial goals.

However, many investors complain of not having earned enough from their mutual fund investments. A closer look suggests an anomaly in their investing patterns, especially, in the way they regard their investments.

The most common question asked is “Tell me a good fund that will give the highest possible returns in the shortest possible time with the least possible risk.”

Give your investments time to grow

Investors must realize that these things do not combine. In the short run, the possibility of creating a corpus is practically nil. Investments that look less risky and very rewarding and promise great returns will not sustain. The starting point should be “For how long should you invest the money?” This is a question that you must ask yourself and be willing to respond to it with full clarity.

Also, what kind of downside can you witness in between? You must answer this question assuming that you will stay invested for the coming decade. However, the question remains if you will be able to withstand the market volatility, say if the market goes down by 40 per cent. The one common blunder that many people make is looking at their investments every day. This causes unwarranted anxiety and the tendency to succumb to market rumours.

Muthukrishnan, a Chennai-based Certified Financial Planner says, “On a daily basis, you've one bad day for a good day. This means that 50 per cent of the time you would see your portfolio down on a daily basis. Instead, if you check on a yearly basis, you would see more good years than bad years. Roughly 70 per cent of the years are good and only the rest 30 per cent are bad. This would strengthen conviction for you to stay the course.”

Giving your investments enough time is needed. Scaling investments is possible only when you give enough time to your investments.

Knowing your financial goals

Investing in tips is one major problem. If you are a new investor, do not fall blindly for what people say. It’s okay to feel afraid when you see many people shorting their investments or read news about a decline in investments due to market tumult. It is human behaviour to feel nervous because this is how most people react. However, this reaction will be to your disadvantage.

If you are new to investing, the starting point should be to first gauge your investment tenure. For how long should you invest? This in turn depends on how many market changes can you withstand. This is important for this will help withstand how much money you should invest.

The time you are willing to give to your investments and your nonchalant attitude toward money highlights how experienced you are as an investor. Most people are able to withstand a 30-40 per cent decline for four to five years. This waives off their apprehensions regarding money investments as recurring market volatility makes you immune to it.

Dev Ashish, Founder, Stable Investor says, “When one invests in equity mutual funds, it’s always advisable to remain invested for at least five years. Most investors, who are introduced into equity via tax-saver ELSS funds believe that since the lock-in for the same is three years, they should assess equity returns too for similar periods. But that is not correct. The lock-in period is not the right time period to assess equity returns. Equity is for the long term and hence, be willing to wait for at least five years. And this is the reason that one when invests in equity, how their investments do in the initial four to five years defines how their first experience with equity is."

“If it’s good, they get convinced and start investing more in equity seriously for the long term. If the experience isn’t great, then people gradually start avoiding equities. It is, for this reason, that to increase the probability of getting reasonably good returns, one should be investing for more than five years and also not panic if there is negative volatility in the short term,” he added.

Also, decide your tenure based on your financial goals. If have a goal in mind, how negotiable is that? Are you willing to wait for a long period till you have accumulated the corpus you were looking out for or will you withdraw your money before you have hit your goal?

You must understand that some goals are not negotiable, especially, those that are tied up to a particular event in your life. Take, for example, investing in a child’s plan that requires you to accumulate a certain amount by the time your child is ready to go to school. You cannot negotiate on the day your child will go to school. This explains why you must be steadfast with your investments, especially, when the money would be needed to fund a particular or significant event because you will need that money at that particular time.

Even if you are willing to compromise, how much variation are you willing to tolerate? Would you consider the idea to withdraw a few months before you reach your goal or will wait to reach your goals while arranging the money from other sources?

Right asset allocation matters

How many of us have heard the importance of allocating our investments right? How many times have we been told not to invest all our money in only one asset or one kind of asset alone? Also, how do you go about investing your money, especially, when the going is good? Most people start with fixed or recurring deposits. This helps too as you must have enough money in the bank to pay for sudden and unforeseen expenses, especially while dealing with emergencies.

Parking your money in various investment options early is important, or else you miss out on the opportunity lost based on the time value of money to create wealth. It is good to be fully invested but that does not mean that you beg, borrow or steal to invest. At times, investors are so tempted to invest money that they end up taking loans and end up paying more in interest than what they earn during that loan period.

Sometimes, the market is fully ripe for investment. That’s when many people borrow money to invest. Suresh Sadagopan, Founder, Ladder7 Financial Advisories says, “Fundamentally, one invests when one has surplus to deploy. Borrowing money and investing is with the idea of making more money than the borrowing cost. This may not happen in many situations and one may get trapped in debt.”

Markets are cyclical, which means that bad times follow good times. This is when investors run for cover. Panicked investors take their money out and ensure that not a penny of their earnings is invested into equity. Undoubtedly, borrowing to invest is the wrong way to start. Here for most investors, the starting point is mostly in equities. This is a wrong approach to investing. Always, start with parking your money in aggressive hybrid funds. The idea ratio must be 75 per cent into equities and the remaining 25 per cent into debt. This helps because even if the market goes down temporarily, the debt component will provide the much-needed cushion, thus, acting as a necessary shock absorber.

Also, when you are about to reach your financial goals, reduce your allocation to equities so that sudden shocks do not create a dent in the earnings that you have accumulated on your investments over the period. Just five years before you retire, take out your money from equities gradually and put it into debt funds. This will ensure that your corpus is not hurt and you reach your financial goals within the decided period.

You may invest depending on your risk appetite but the whole idea is to invest in a way that smoothens your journey and helps you navigate through the various assets, irrespective of how the market behaves.

Remember that the market ups and downs will not damage your wealth permanently. Rather, they will help you better allocate and invest at lower prices to sell at higher prices. Taking the market movement into stride during asset allocation will do you a lot of good in the long run. The market is a very rewarding place for those willing to wait but can also be a dangerous place to be in if you are not careful.

Focus on fund choice

The right way to go about investing in mutual funds is to be first methodical in your approach. This you can do by choosing the correct fund. There are roughly 32 different kinds of mutual funds, which means choosing the one that befits you most is not an easy task. Also, within these 32 there could be 50 others. For example, if you opt for an index fund category, you will be surprised by so many kinds of index funds introduced by different asset management companies (AMCs) in India.

Pratibha Girish, Founder, Finwise Personal Finance Solutions says, “The category of mutual funds to invest in depends on the time horizon for the goal you are investing. For example, you could invest in debt funds (Banking and PSU or liquid funds for an emergency corpus). For goals between three and five years and for incorporating debt into a long-term portfolio, one can look at hybrid funds. For a long-term investment of more than five years, one should invest a significant part in equity funds as per risk appetite. Within this, in debt, you should look at the quality of papers held for credit risk and average maturity for interest rate risk. In equity, one should look at the consistency of performance, upside and downside capture and overlap of the portfolio while choosing funds.”

Choosing the right kind of fund is essential to asset allocation. This is because investing in funds haphazardly or based on hearsay will not grow your earnings as desired. For example, start with a hybrid fund that will ensure adequate exposure to both equity and debt.

Alternatively, you could dissolve all your equity investments five years prior to reaching your financial goals or before retirement to an aggressive hybrid fund to keep your corpus protected while also earning from the market undulations.

Simplicity pays. It helps to create wealth. Choose the right kind of fund and keep it simple. Beware of investments that you do not understand. Just drop your idea of investing in any fund if you find the contents in the fund offer document ambiguous.

Adopt a systematic approach

Most investors titillate between being greedy and being extremely fearful. However, the way we deal with the market decides how our money will grow in time. The problem is that when the market goes up, investors rush head over heels to invest their money. The same investors will rue and cry when the market goes down not realizing how they are losing out on the right opportunity to put in their money.

Investing in a market frenzy is as dangerous as taking out your money to a casino hoping to win and earn. Taking out the money when the market collapsed has caused many investors to suffer unprecedented losses. To tackle this problem, you must just focus on your investments and be regular with them. This explains the need to invest through systematic investment plans (SIPs). It justifies many personal finance experts’ saying, “Just do your SIPs”.

Adhil Shetty, CEO, BankBazaar.com says, “Investing under the SIP method prevents investors from worrying over the price of the stock or the mutual funds. Investing at regular intervals irrespective of the price of the unit cancels out the effect of price fluctuation in the market. When the prices come down, your fixed amount can buy more of the units and when the prices go up, this adds to your gains. Moreover, investing monthly develops a disciplined approach to money and investing, which is the key to building wealth.”

The drawdown of not investing through SIPs is that you will be waiting for the market to go down to investing. This also translates to missing out on possible investment opportunities because you may wait for the market to go down further. There is always a considerable wait among many investors for the market to touch the bottom, which does not happen most of the time.

By the time you realize that the markets will not drop down further and you are ready to put in your money, the markets bounce back to their original range, thus, depriving you of the opportunity to put in the money you had set aside for investments. Doing SIPs regularly reduce the risk of investing all your money when the market is at an all-time high.

Investing in a lump sum, though helps, can cause you to feel unnerved in case the market goes down immediately after you invest your money. So, invest in small amounts regularly to escape the brunt of making a large investment in one go.

The markets will keep you surprised all the time, which means that you will always be on your toes while trying to tap their movement. Better to invest in small amounts, unbiased of market oscillations.

Do not redeem midway

If you have an urge to sell your mutual fund investments, resist falling prey to all the reasons to redeem your investments halfway through your investment journey. It is common for many investors to withdraw their money after they believe they have earned enough from the growing market. Some do take their money, especially, those investing on their own sans the advice of personal finance advisors.

Simply because the market has gone up and your investments have done well is not enough reason for you to liquidate your investments. Resist the temptation to take out the money to spend or reinvest. The tendency to escape the effects of a plunging market by redeeming your investments must also be stopped.

Rahul Agarwal, Proprietor, Advent Financial explains, “As humans, we have developed this action bias where we favour action over inaction often without any evidence suggesting any value creation resulting from such action. If there is one field where the fallacy of this action bias can be seen in actual empirical evidence, it is the field of investing. There are numerous studies that amply illustrate the ‘gap’ in ‘investor’ returns vs ‘investment’ returns. This results in investors not remaining invested in the fund long enough by prematurely exiting their investment to invest in the ‘top’/‘best’ fund. Such frequent chopping and churning of funds in the portfolio in pursuit of the ‘best fund’ can be best described as an exercise in futility.”

Impulsive buying and selling is normal, and that is why you must avoid the same behaviour in your mutual fund investments too. With redemption becoming easy over the web, many people find themselves in an unjustified rush to do so.

It’s not okay if you want to redeem your money, but be methodical about it. This is as true as being methodical with your investments. Pay attention to both your purchases and redemptions. The redemption process must be gradual like your investment purchases.

Never try to time the market. Instead, rely on a systematic withdrawal plan (SWP) to take out your money. If you know about SIPs, you will surely know about SWPs too. Apart from the fact that SWPs protect you from redeeming all your investments when the market has dropped, they also allow you to liquidate your investments in a phased manner.

Adopt a methodical approach to your investments. Know where you want to invest. Opt for a decent asset allocation and pay attention to your investment timeframe. You must focus primarily on your investment timeframe, else, without this you would not know for how long to stay invested and when to start gradually withdrawing your money to escape from prolonged and sudden market dropdowns.

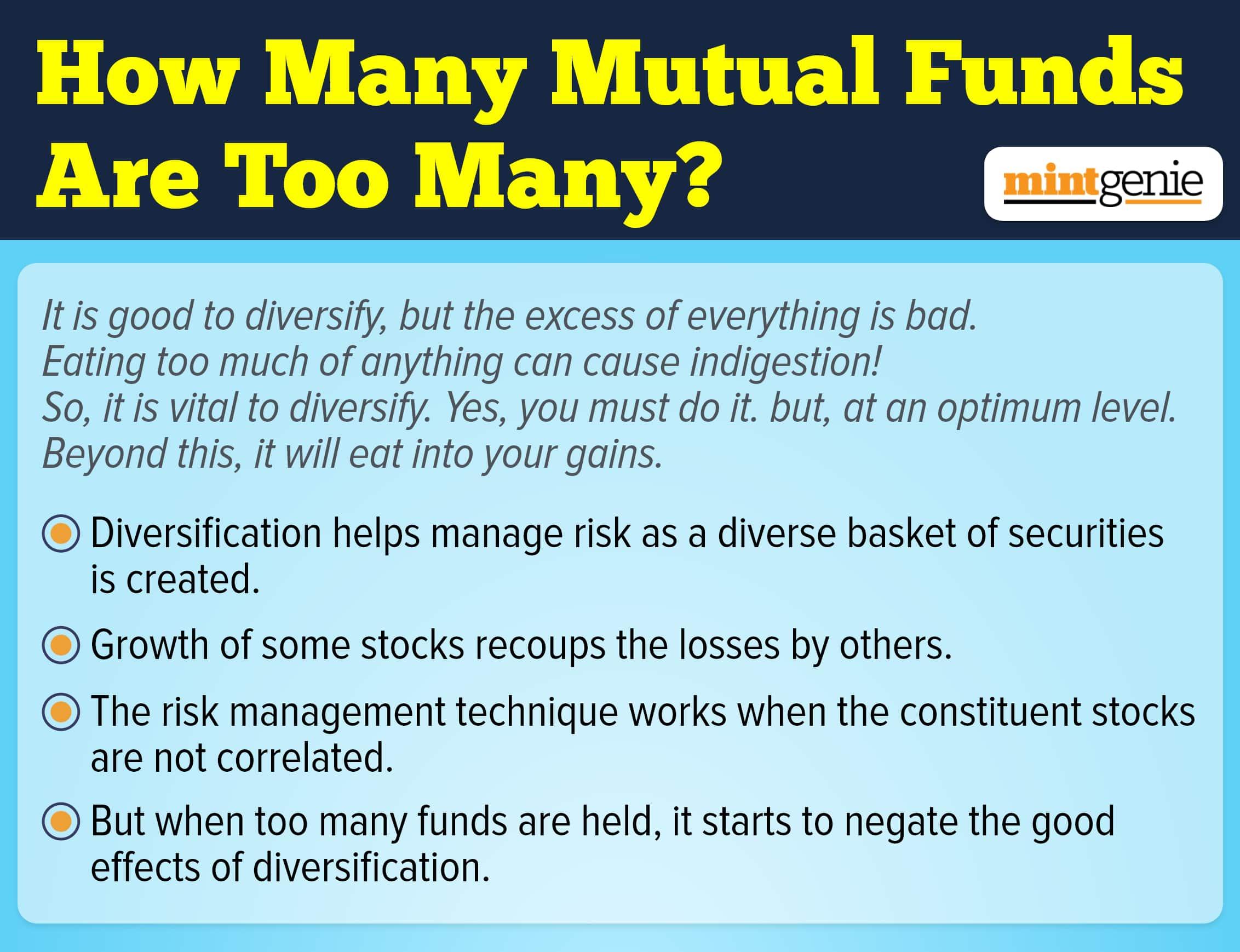

We explain how many mutual funds are too many.

First Published: 20 Sep 2022, 02:36 PM IST

Related Stories

personal finance

SIP vs STP: How to choose between the two for your mutual fund investments?

Kirti Jhapersonal finance

Mutual fund investing: Can it make you wildly rich? Yes, but some caveats apply

Abeer Ray