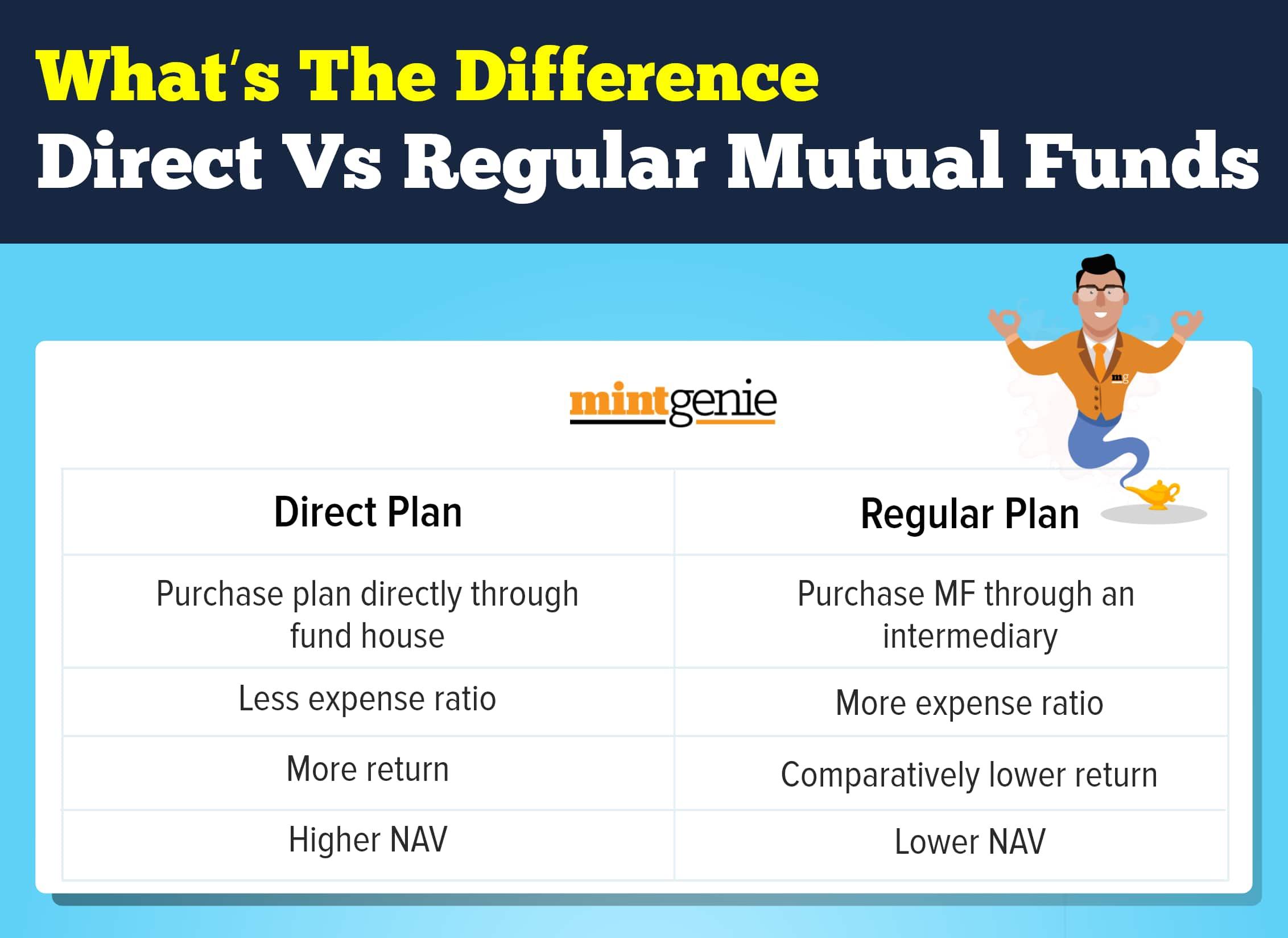

When you invest into a mutual fund scheme, you have two options: either to invest in a direct plan or a regular plan. In a regular plan, one is supposed to pay commission or brokerage to mutual fund distributor whereas direct plan doesn’t include commission.

Total expense ratio is the fee charged by fund house to manage investors’ money in each scheme. Under direct plans, the commission paid to intermediaries is not included in the expenses charged to investors, thus resulting in a lower expense ratio.

So, those investors who want to save money on their total expense ratio (TER) might want to transfer their holdings from regular to direct plan.

Migrate to direct plans

There is no doubt that migrating to direct plan will help you save money. For instance, in Kotak Bluechip Fund, NAV (net asset value) for regular plan is ₹370 per unit on February 8, 2022, while for the direct plan, it’s ₹409 per unit.

Let’s suppose, someone holds 1,000 units of this fund, the difference in the NAV between the two forms of investment stands at ₹40,900 - 37,000 = ₹3,900. Likewise, DSP Top 100 Equity Fund’s NAV for regular plan is ₹286 and for the direct one, it’s ₹304.

Someone holding 500 units through direct plan will stand to own ₹1,52,000 worth of units, whereas in case of regular plan, it is ₹1,43,000, a humble difference of ₹9,000.

There are several options to transfer from regular plan to direct plan. First is to directly give a request to the fund house’s website. The second option is to register on the website or apps of the Registrar and Transfer Agents (RTAs) such as CAMS and Karvy. Switching through the RTA is better for those who are invested into multiple fund houses.

There is a third option to register on mutual fund aggregators such as Kuvera and Groww which allow switching from regular to direct plan.

Investors should be aware of the fact that migrating from regular to direct plan is redemption in the old scheme and a fresh investment in the new one. So, the switch would attract capital gains tax. It will be short term or long-term depending on the category of fund — equity or debt.

If debt funds are sold within three years, the capital gains are treated as short term gains. When sold after three years, the gains are treated as long term at 20 percent with indexation.

For equity mutual funds, this cut-off period to determine long term capital gain is 12 months.

Long term capital gains on equity mutual funds are exempt up to ₹1 lakh a year and the remaining is taxed at 10 percent, whereas short term capital gains in equity mutual funds are taxed at the rate of 15 percent.

So, choosing a direct plan over a regular plan is certainly a rational thing to do. But one should weigh the cost involved in redemption before taking this step.