Banks and other financial institutions are fighting a competitive battle against each other to inflate their loan book. To grab the largest pie of the home loan market, most banks have lately reduced their interest rates.

Union Bank of India slashed its home loan interest rate to an all-time low of 6.4 percent per annum. The Bank of India reduced its rate to 6.5 percent, while State Bank of India (SBI) cut it down to 6.7 percent.

With the race to cut interest rate heating up, it appears to be an opportune time for borrowers to transfer their loan to a lender that is offering an economical deal. As a matter of fact, most banks tend to tempt the borrowers to transfer their loan by offering attractive features such as concession to female borrowers, no prepayment penalty, and no hidden charges, etc.

Transferring your existing home loan to a new bank is easy and convenient. You need to simply approach a bank where you want to take the loan to. When you transfer the home loan, there are two kinds of institutions: transferor (previous bank) and transferee (new bank).

You need to approach the transferee bank, which will clear your outstanding loan to the transferor institution. After paying the processing fee (unless it is waived off) to the transferee, your new loan will commence with the new bank, which needs to be paid in equated monthly instalments (EMIs).

New loan transfer rules

It is noteworthy to mention that the rules governing transfer of loan were recently altered by the Reserve Bank of India (RBI). On September 24, 2021, RBI introduced its master direction on transfer of loans. This mandates all banks and financial institutions to put in place a board-approved policy for transfer of loans.

These rules say the transferor cannot re-acquire a loan exposure, either fully or partially that had been earlier transferred by the bank earlier. This means once a loan has been transferred from one bank to another, then the first bank is not permitted to have any control over the loan.

Also, the rules say that a loan transfer should result in immediate separation of the transferor from the risks and rewards associated with loans to the extent that the economic interest has been transferred.

Borrowers must be aware of certain key rules when they apply for transfer of loan. For instance, the rate of interest advertised by the bank is usually meant for loans under ₹30 lakh and that too for borrowers with a high credit score in the range of 800.

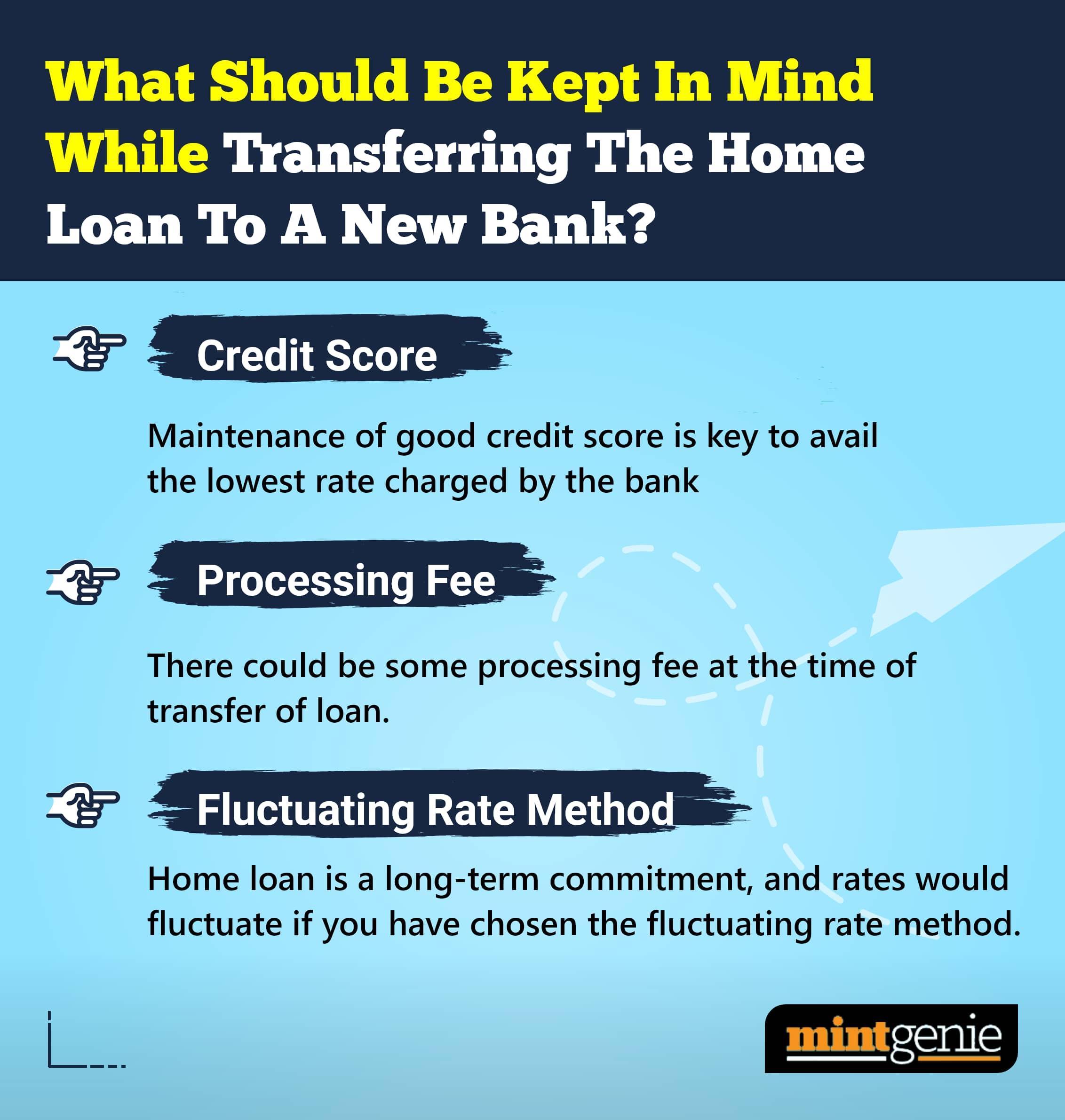

Things to keep in mind when you go for loan transfer:

1. Maintain good credit score: Make sure your CIBIL score is good, if not impressive, to be able to fetch a good loan deal from another bank. Remember that the lowest interest charged by banks are meant for borrowers with a good credit score. Those with bad credit score may find it hard to get loan approval, especially at a low rate of interest.

For instance, HDFC’s lowest home loan rate of 6.7 percent is offered to borrowers whose CIBIL score is above 800. For others, the rate of interest ranges between 6.8 percent to 7.65 percent based on the amount of loan borrowed. The higher the loan amount, the higher the interest.

SBI has also earmarked its lowest rate of 6.7 percent for borrowers with 800 and above CIBIL score. For others, the minimum rate is 6.8 percent.

2. Rates keep fluctuating: Remember that if a loan is taken at a floating rate of interest, then the rate might increase with change in market situation. So, if your loan will be outstanding for the next 10-15 years, the current rate will not remain stable for all these years.

3. Processing cost: When you go for refinancing your loan, remember that you factor in loan processing cost. And it will make sense to transfer the loan only when your savings are more than your processing cost.

In summary, existing home loan borrowers can contemplate transferring their loan to a new lender which is offering an attractive rate of interest. But remember that the loan transfer may involve cost, and on the top of it, home loan is a long-term decision, so it may not be prudent to transfer it for small savings.