As financial year draws to a close, investors are taking the last-minute decisions to make investments to save tax. Some are geared to invest in the tax-saving schemes such as NSC, PPF, NPS, ELSS and SSY, among others; whereas others are more inclined to buy insurance products.

In the run up to the end of financial year, small investors tend to take wrong calls in a haste to save tax. For the uninitiated, investors can invest up to a maximum of ₹1.5 lakh under a slew of saving instruments to claim deduction in their taxable income.

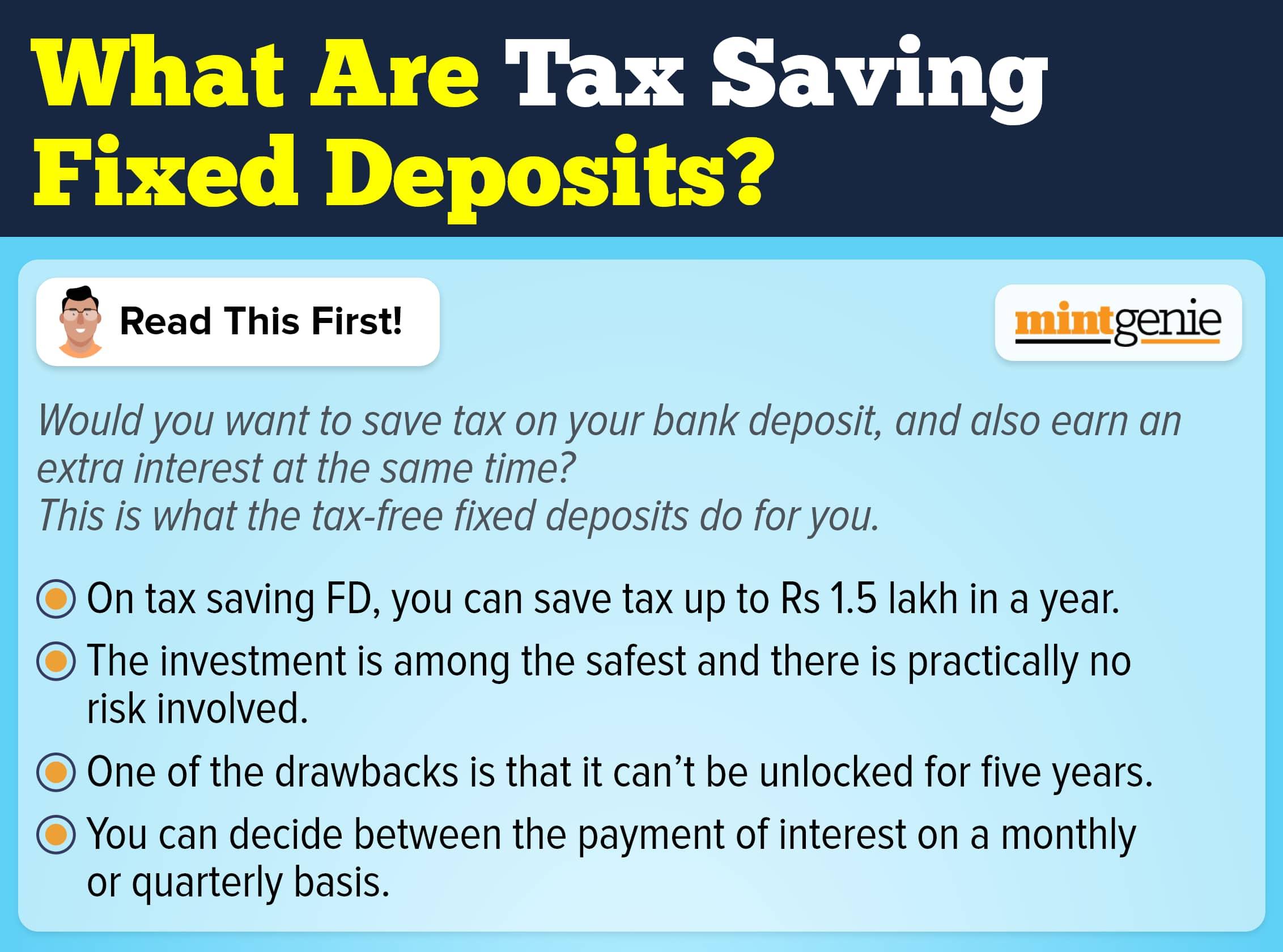

Over and above, investors can also claim an additional deduction of up to ₹50,000 by investing in National Pension System (NPS) under section 80CCD(1b).

What steps can be taken

Financial experts have a slew of advice for the new investors who want to invest only to save their tax. First and foremost, investors are advised to make online payment rather than sending a cheque during the last few days.

Secondly, investors should be mindful of the fact that the investment scheme should meet their portfolio allocation.

Investors shouldn’t choose an investment scheme merely for tax saving, it should meet their portfolio allocation as well. say experts

Financial advisors advise new investors to be mindful of their financial goals before investing in a financial product only to save tax.

“First and foremost, investors should see if they already have an insurance product. If they don’t have an insurance, you should first buy it. Later, they can buy equity products based on their allocation and financial goals,” says Deepesh Raghaw, Founder of PersonalFinancePlan.

Financial experts assert that tax saving at the eleventh hour can trigger irrational moves, leading to wrong asset allocation and poor liquidity. So, it would be better if investors take these decisions at the start of the year.

“Investing for tax savings at the last minute can lead to the wrong investment decision. This can impact much more to those investors who have started their investment journey as their portfolio at this stage is just about to get in order. It is better to plan tax saving investments at the beginning of the financial year after looking at the overall portfolio. It is not just that the asset allocation can get impacted but an incorrect decision can also impact liquidity depending on the instrument of investment,” says Harshad Chetanwala, Co-Founder, MywealthGrowth.com.

He adds, “Tax savings through ELSS is locked for 3 years and after that you can take the money back if required. Investment in PPF or Life Insurance can have a longer lock-in period. Another factor to keep in mind is there is a possibility of some investment in EPF by default which is a debt-based investment.”

Need for diversification

It is quite common to find a lot of financial products being sold vigorously during the tax saving season. Investors are told to buy these products only when they need them.

“Small investors should make sure that they diversify their investments instead of investing all their investible corpus in one asset class just to save tax,” says Deepak Aggarwal, chartered accountant and financial advisor.

ALSO READ: Income Tax: Last few days to invest in tax-saving instruments; Here's a checklist

“Usually, tax saving instruments should not be used to meet short term goals because these instruments have a long lock-in periods – sometimes as long as 15 years. For short term financial goals, one can invest in ELSS which has a three-year lock-in,” says Aggarwal.

Another advice which financial experts give is that one should not take a personal loan to buy tax saving products since the interest on loans, more often than not, outpaces the return on these investments.

While most banks charge personal loan anywhere in the range of 12-14 percent per annum, tax saving schemes give return in the range of 7- 8.5 percent.