Investments in mutual funds are common, especially, among those looking for earnings in sync with the market, but are unable to trade in stocks and shares. However, when it comes to showing their earnings while filing their Income Tax Returns (ITRs), many of us feel lost. Not all gains are similar considering how you may invest in equity and debt mutual funds depending on your financial goals. Then, there are dividend mutual funds too that promise regular returns, thus, enabling many to receive a continued income source. Redeeming mutual funds is another aspect that we dare not ignore while assessing and including income from mutual funds in our ITRs.

Many are trying to wade through the sections regarding the taxation of returns and gains from mutual funds. Besides, there is also the need to disclose income sources too while filing your ITR. The following is the list of rules regarding the various kinds of incomes from mutual fund investments and their concerning tax implications.

Dividend income

Dividend income is always taxable in the hands of the investors. This is irrespective of whether you have earned dividends from equity funds or debt mutual funds. You must include dividend income under the tab “Income from Other Sources”. This means that even salaried taxpayers earning dividend income from the market, be it from stocks or mutual funds must club dividend earnings under “Income from Other Sources”.

Mutual fund redemption

The rules concerning mutual fund redemption are different for equity and debt mutual funds. This is because the holding period regarding short-term gains differs. Consequently, the taxation rules are no more the same.

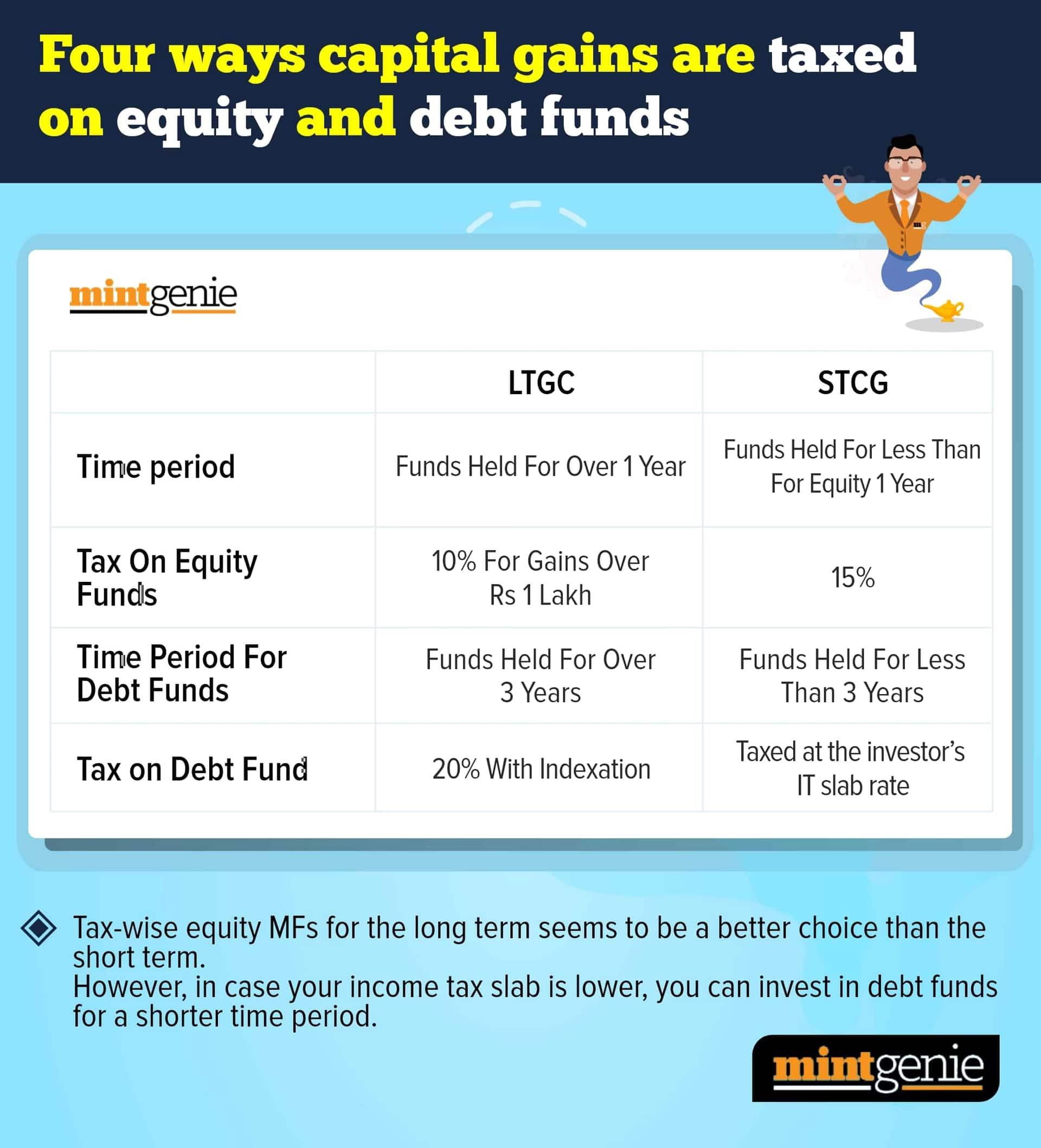

Short-term capital gains

The income from the redemption of debt funds within three years of purchase is deemed as short-term capital gains. If the redemption of equity funds is made within a year of purchase, then the income from these funds is again classified as short-term capital gains. Though the nature of gains comes from the same source, i.e., the redemption of the mutual fund units, the holding period in debt funds is different from their equity counterparts. Short-term capital gains from equity-oriented funds are taxed at 15 percent. The tax rate on short-term capital gains on debt funds is as per the income tax slab of the investor.

Long-term capital gains

Some people prefer to stay invested in mutual funds for prolonged tenures. The earnings from the redemption of these funds are classified as long-term capital gains (LTCG). The holding period and consequently the taxation rules on long-term gains differ across both debt and equity funds.

The earnings from the redemption of debt funds after three years of their purchase are long-term capital gains. Such gains are taxed at 20 per cent post indexation. Similarly, the money earned from the sale of equity-oriented schemes a year after their purchases is classified as long-term capital gains that are taxed at 10 per cent sans indexation if it is more than ₹1 lakh in a financial year.

In both debt and equity funds, redemption may be done either in a lump sum or regularly through systematic withdrawal plans (SWPs).

Disclosing mutual fund income in ITR

You cannot club all kinds of income under one roof in the ITR. This explains why salaried taxpayers cannot disclose capital gains in ITR-1. They must fill in the details regarding dividend income, and short-term and long-term capital gains in ITR-2. Assessees can fill up the Page 112A specifically included in ITR-2 for disclosing capital gains or losses from both equity and debt mutual fund schemes.