As the deadline to file income looms closer on July 31, taxpayers must be busy arranging the essential documents to be able to meet the deadline. These documents serve as proofs of different sources of income which entail salary, rental income, business income, and the gains made from the sale of assets such as land and securities — also known as capital gains.

What are capital gains?

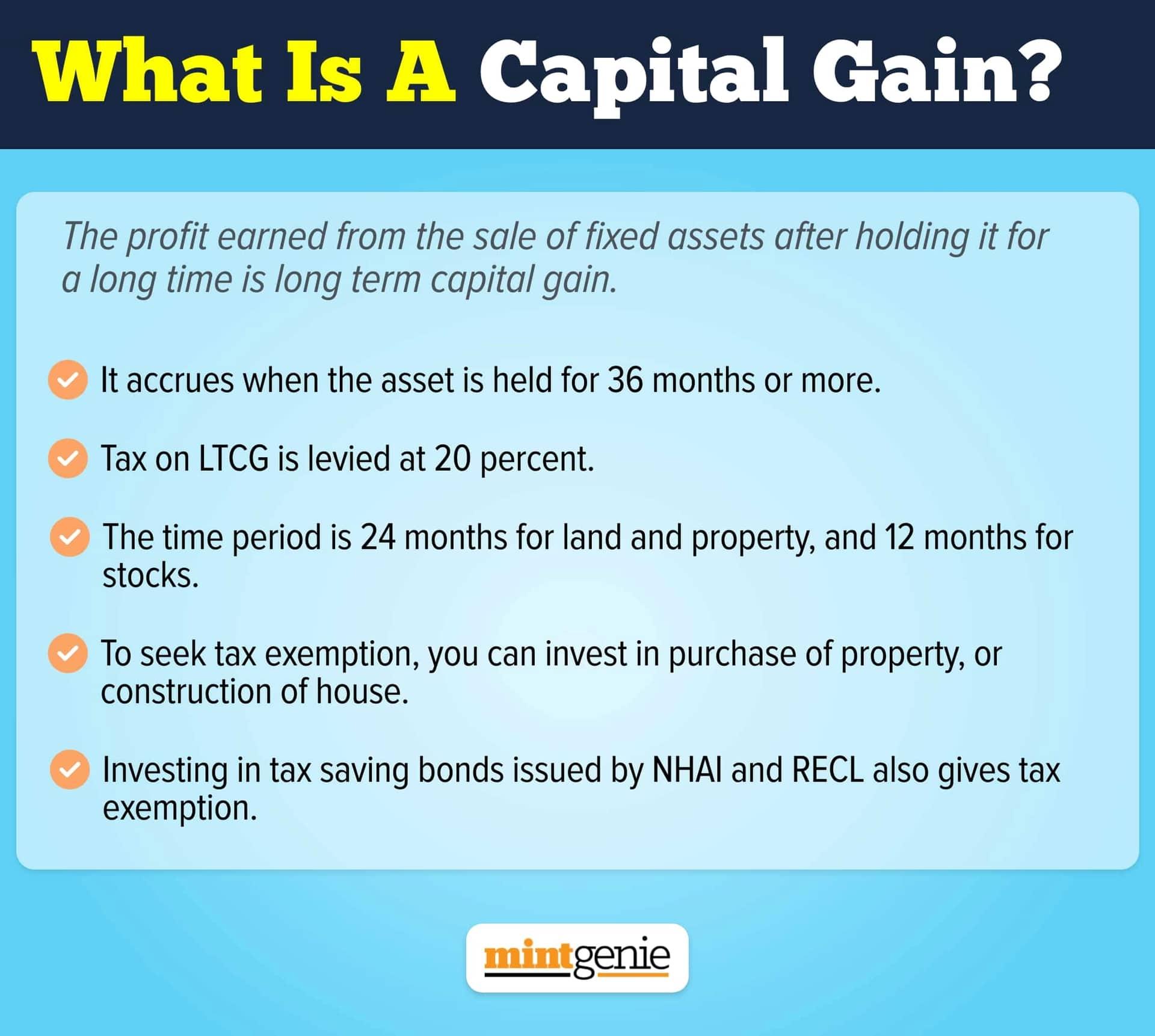

When you transfer an asset such as investments or real estate or debt funds, the income accruing from it is known as capital gain. There are provisions in the tax legislation defining the type of capital gains as long term or short term — depending on the tenure for which these assets were held before selling them off.

For instance, the sale of immovable assets comes under long term capital gains if sold after two years (w.e.f. 2017-18) and the time period reduces to one year in case of securities and mutual funds.

How to seek tax exemption?

To save capital gains tax, you can essentially do one of the two things: first is to buy a property and second is to invest in bonds under section 54EC of the Income Tax Act.

To seek exemption, tax payers under section 54EC of the Income Tax Act should invest in tax saving bonds issued by REC. Until March 31, tax payers could invest in NHAI bonds as well but on April 1, 2022, the national highway authority of India discontinued these bonds where REC rolled out the new series of 54EC capital gains bonds.

Limits that apply

It is vital for tax payers to know that this investment ought to be made in less than six months of the sale that accrued capital gains. Also, the maximum exemption allowed in one financial year is ₹50 lakh.

These bonds offer safety of capital for investors as they are AAA-rated.

The tenure of these bonds is five years and after the completion of five years, the proceeds are not meant to be invested anywhere and the cash received is tax-free but the interest received on the bonds is not.

One can also buy bonds for a part of the capital gains proceeds and pay tax on the remaining sum. Let us understand this with the help of an illustration below:

Example: Let’s imagine that you sold a house for ₹60 lakh after owing it for more than two years and the capital gains accrued on it is ₹30 lakh because its price was ₹30 lakh. Since you don’t want to buy another property with the proceeds, you will have to pay tax on the gains. To be able to save tax, you have two options

Scenario A: Invest all the proceeds in REC bonds and save tax on entire ₹30 lakh taxable income.

Scenario B: Invest a portion of capital gains proceeds, say, ₹15 lakh in the bonds, and pay tax on the remaining sum i.e., ₹15 lakh.

So, these bonds are quite useful since they offer interest each year, help you save income tax and needless to mention that your investment will be immune from the default of any kind.