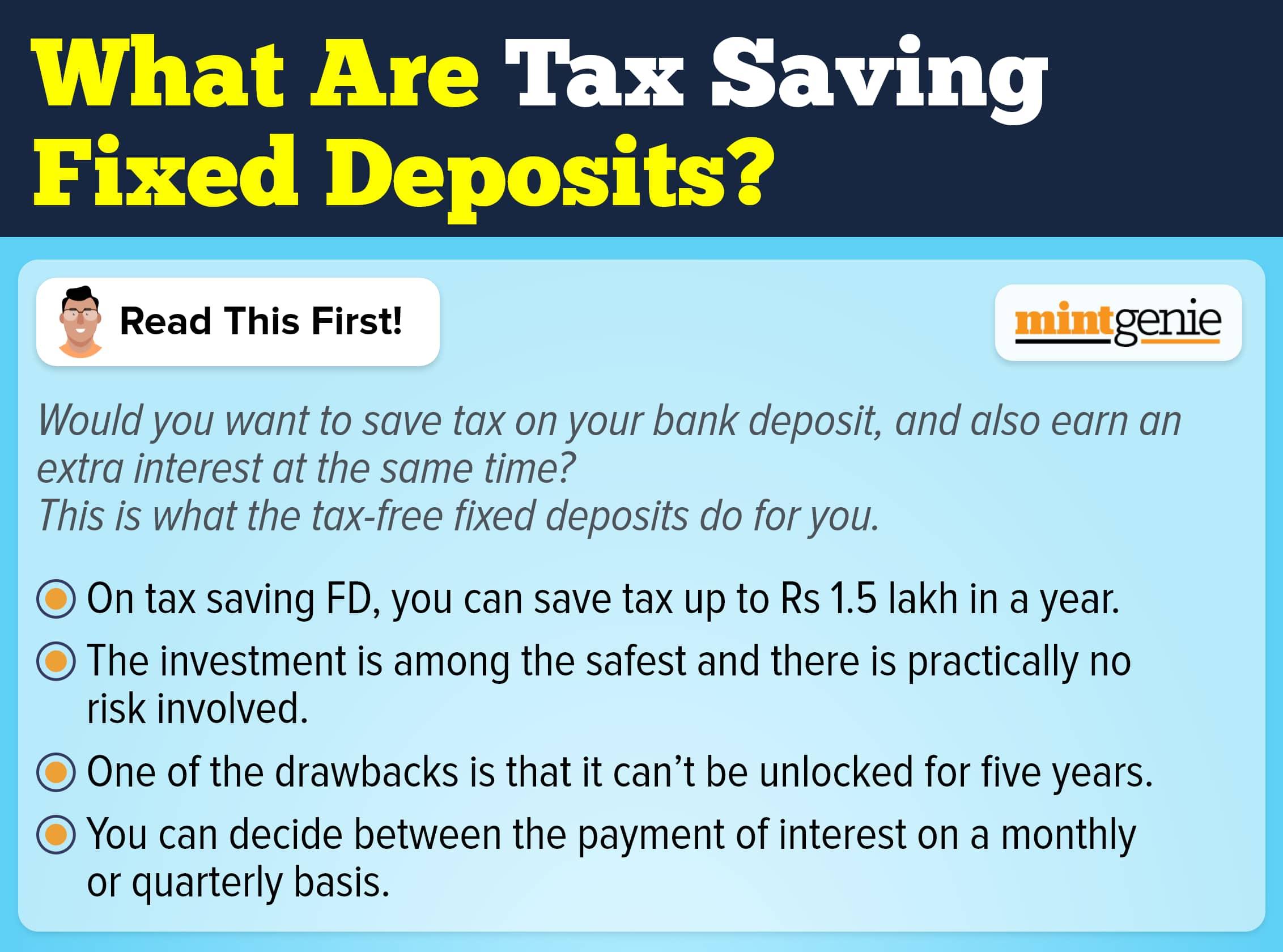

In case you happened to under-report your income in the financial year 2019-20, then you are allowed to file an updated income tax return (ITR) prior to March 31, 2023 to incorporate the changes.

The provision of filing an updated return was introduced in the Finance Act, 2022.

At the time of introduction of this provision, a new sub-section 8(A) was inserted to Section 139 of the Income-Tax (I-T) under which a tax payer is allowed to file an updated return of Income Tax (I-T). The deadline for filing an updated return is two years from the end of the relevant assessment year.

So, the taxpayers who inadvertently reported less income while in filing the original return, belated return or revised return can file an updated return of income tax (ITR-U). An updated return can be filed even if the original return is filed by the tax payer or not.

It is vital to understand that there is a difference between a revised return and an updated return. Let us understand the key difference between the two:

A revised return is filed under section 139(5) where a tax payer can file a return to correct the previously filed return within a stipulated time i.e., before December 31 of the relevant assessment year.

On the other hand, an updated return can be filed after the end of the relevant assessment year. Tax payers are given a maximum of two years to file an updated return.

Why should you file an updated return?

An updated return is a provision extended to tax payers who lately discovered an additional income previously not disclosed by them.

The taxpayer must have accrued an additional income tax (I-T) as a result of updated return. Conversely, if there is a tax refund arising out of the new return, then filing an updated tax return is not allowed.

So, to be able to file an updated return, the following three conditions must be fulfilled:

1. An updated return can be filed to pay additional tax liability.

2. Taxpayer cannot file an updated return to report loss, leading to lower tax liability.

3. One can file an updated only once for one assessment year.

Importantly, tax payers must be aware of the fact that an updated return comes with additional tax penalty.

“When an updated return is filed within 12 months of the end of relevant assessment year, there is an additional tax liability of 25 percent. After more than 12 months but before the expiry of 24 months from the end of the relevant assessment year, an additional tax liability of 50 percent is to be paid,” said Delhi-based chartered accountant Deepak Aggarwal.

Also, one can file an updated return in case a proceeding of assessment, search, or survey is pending against the tax payer.

Although the additional tax penalty is too high when seen in isolation but it is still affordable when compared with 300 percent penalty that can be levied in case tax authorities assess the income at a later stage.