Note: This is an ongoing series on insurance.

----------------------------

We all love to have extra benefits in a single product even if it has some incremental cost. While booking flight tickets, we usually add meals to make sure we enjoy our journey with nice food. Similarly, in case of term life insurance policies, you can add such provisions or features known as riders.

What are riders?

Riders are types of features that give you an option to gain additional benefits with your existing term insurance cover. These are low cost extensions to your policy for specific circumstances.

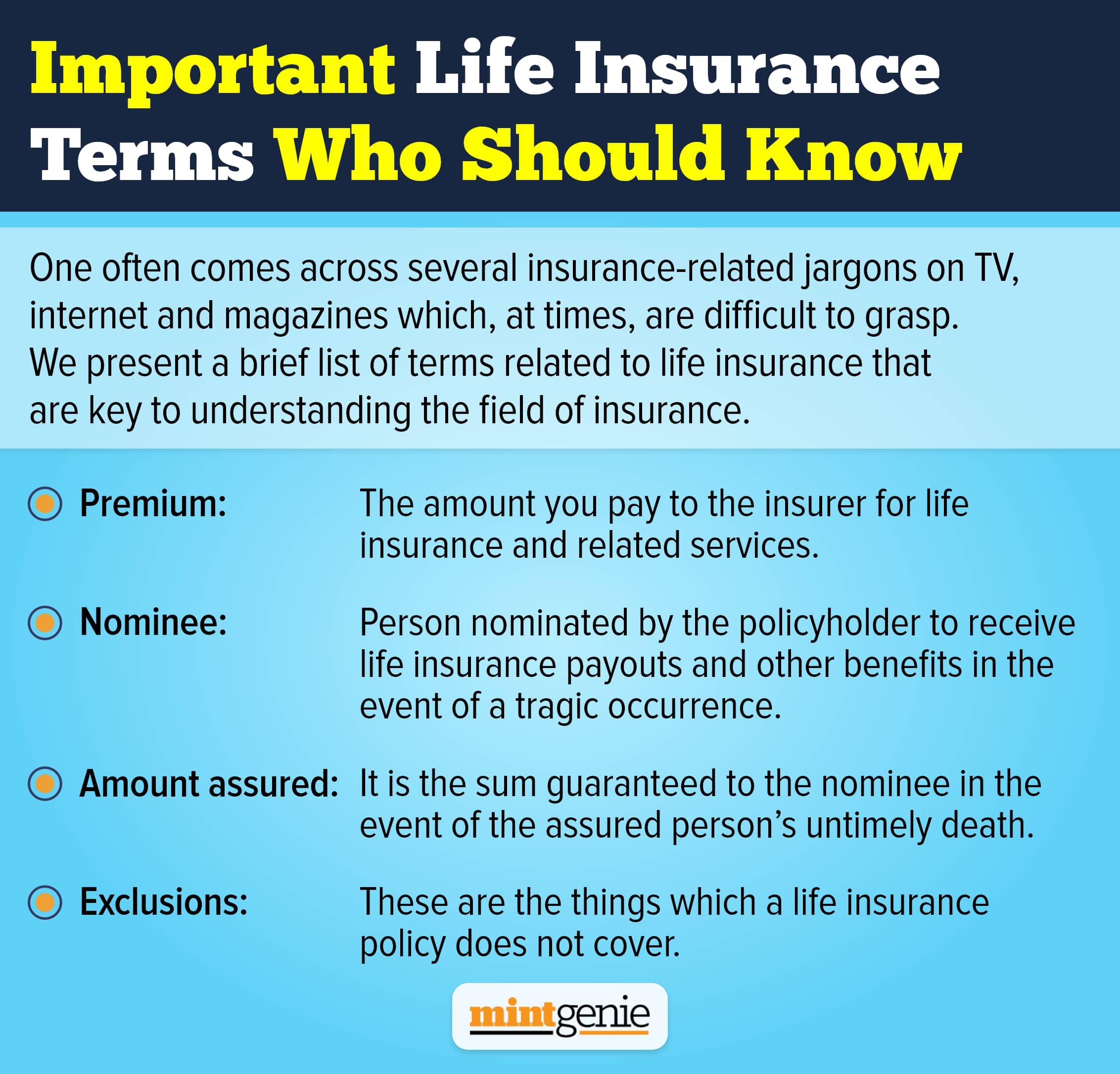

In the earlier posts we discussed about basics of term life insurance, who should buy term life insurance & when you one buy it in our previous posts.

In the current post, we are going to discuss everything about the riders that you can buy as a combo with your term life insurance policy.

There are four types of riders available with a term life insurance policy:

1) Critical illness rider

2) Accidental death benefit rider

3) Accidental disability rider

4) Waiver of premium rider

Let's try to understand each one of these riders in details.

1) Critical illness rider: In the current scenario of fast-paced and stressful lifestyle, the risk of encountering any of the critical illness is quite high as we grow old. This could create a severe dent on the physical health of insured. Also, rising healthcare costs could drain the financial resources if at one is diagnosed with critical illness. A critical illness rider pays fixed cash benefit to the policy holder in case they are diagnosed with any of the serious illness covered under term insurance policy. This rider can be enabled by paying extra premium along with the basic premium for pure term insurance to cover the risk of encountering critical illness during the policy term.

However, one should check the following things before buying a critical illness rider:

The rider should pay cash benefit apart from the death benefit offered by term insurance policy. Sometimes this rider is just an accelerated cover and it merely pays you a portion from your base term insurance in advance. Make a note that this rider should pay cash benefit separately.

Check the list of diseases covered carefully, insurance agent might give you a very big number of diseases that are being covered but go through the list and ensure that most common diseases like cancer, cardiac, kidney related diseases, paralysis etc are covered.

There are also standalone policies available critical illnesses, one should check those policies too & compare if they offer benefit coverage & benefits.

2) Accidental death benefit rider: As the name suggests, accidental death benefit rider pays out an additional cash benefit in case of death due to accident. Eg: Ms. K has a base term insurance cover of ₹1,00,00,000 and also has an accidental death benefit rider of ₹25,00,000. In case of demise of Ms. K caused due to an accident during the policy term, her family will be entitled to a claim of ₹1,25,00,000 (Base cover + Accidental death benefit). However, in case of natural death, the claim amount would be ₹1,00,00,000 (Base cover). Before adding this cover to your base policy, compare the premium of equivalent amount of base cover and see if there is any major difference. A higher base cover should be preferred if there is very little difference in the premium as it would be wiser to get fully covered.

3) Accidental disability rider: Another outcome of accidents could be disability. Disability caused due to accident can not only cost for treatment of injuries but also lead to loss of earning potential in case one does not remain fit to work to earn a living. This rider provides a fixed cash benefit to cover all the costs relating to treatment of injuries. One can avail this rider along with the base term insurance policy or one can look for a standalone comprehensive personal accident policy that has much wider coverage. A comparison with respect to premiums of rider and a standalone policy must be done to take a call on whether to go for a combo or a standalone policy.

4) Waiver of premium rider: This is an add-on feature that waives off future premiums in case you are diagnosed with listed critical illness or permanent disability due to accident. It is a very low cost rider and should be taken with base policy without much thought. It costs around ₹200 - ₹400 per annum for a base term policy of ₹1,00,00,000 for a person aged 30 years for a cover till the age of 60 years.

No-brainer right?

Tip: Take help from an investment advisor or financial advisor in determining the riders required in your case & also ask them to give you comparison of premiums on combo riders & standalone riders before buying them.

CA Rohit J. Gyanchandani is Managing Director, Nandi Nivesh Private Limited, A Pune based Wealth Management Company.