Tax season in India is a time of great stress and confusion for the average taxpayer, who may not be aware of all the tax deductions and exemptions that can be claimed. It is also a time when insurance traps can easily be encountered.

Insurance traps are those policies or plans that are offered to taxpayers with the intent of selling them an insurance product under the guise of tax savings. While these plans may provide some tax benefits, they are often more expensive than other types of investments and do not provide adequate returns on investment.

This article will discuss some of the common insurance traps that citizens should be aware of and avoid during tax season.

The “Guaranteed Return” trap

One of the most common traps that people fall into during tax season is the promise of guaranteed returns. Many insurers use this pitch to attract customers who are looking for safe investments with assured returns. They often try to sell traditional policies that promise a fixed rate of return, usually between 4-6%.

However, what these buyers fail to realise is that insurance is not about income or return but protection. Instead, they should buy a simple term insurance policy to protect their family financially. Term policies provide higher coverage at lower premiums, making them a much better option than traditional policies.

The “Money-back” trap

Money-back policies are a type of insurance trap that can lead to significant losses if not utilized properly. These policies are often sold as an easy way to save taxes and provide regular income over a certain period of time.

In reality, the returns on these policies are usually quite low and the premiums associated with them are high. To make matters worse, policyholders may be subject to surrender fees if they decide to exit the plan before it reaches maturity.

Before investing in a money-back policy, investors should carefully consider their overall financial goals and risk tolerance. Although these policies may offer the potential for tax savings and regular payments, the rewards may not outweigh the risks involved.

The “Triple Benefit” trap

Another popular sales pitch during tax season is the promise of triple benefit – life cover, tax benefits, and investments. People often rush to buy life insurance policies without assessing whether they really need it or not.

In a hurry to save on taxes under Section 80C, many end up buying policies they do not necessarily require. It is important to remember that your Employees’ Provident Fund contribution and children’s tuition fees, both eligible for deduction under Section 80C, can consume a large chunk or even exhaust the entire ₹1.5 lakh limit.

Thus, tax planning should be embedded into your overall financial planning. Start investing in April so that you can invest monthly instead of having to gather ₹1.5 lakh at one go in January or March.

The “long-term corpus” trap

Non-linked, non-participating, guaranteed endowment policies are another popular choice during the tax season due to the assured maturity proceeds they are promised. Although they guarantee secure returns, they offer lower returns of around 5 percent compared to ULIPs and participating policies.

Moreover, traditional policies mainly invest in debt instruments and the returns never exceed 4-6 percent. Thus, these policies may not be suitable for everyone and investors should consider their individual financial objectives before investing in them.

The “Lapsed Policy” trap

This is another common trap encountered during tax season. Unlicensed tele-callers often call individuals whose policies have lapsed and inform them that their policy has accumulated bonuses. They then ask them to pay a fee and buy a fresh policy in order to claim the bonus.

While mis-selling victims have a window of 15-30 days to return and cancel the policy, the callers often tutor them on responding to calls from insurers. Thus, it is important to verify any information that you receive from such callers and never ignore verification calls from insurance companies post-policy issuance.

How to avoid falling into these traps?

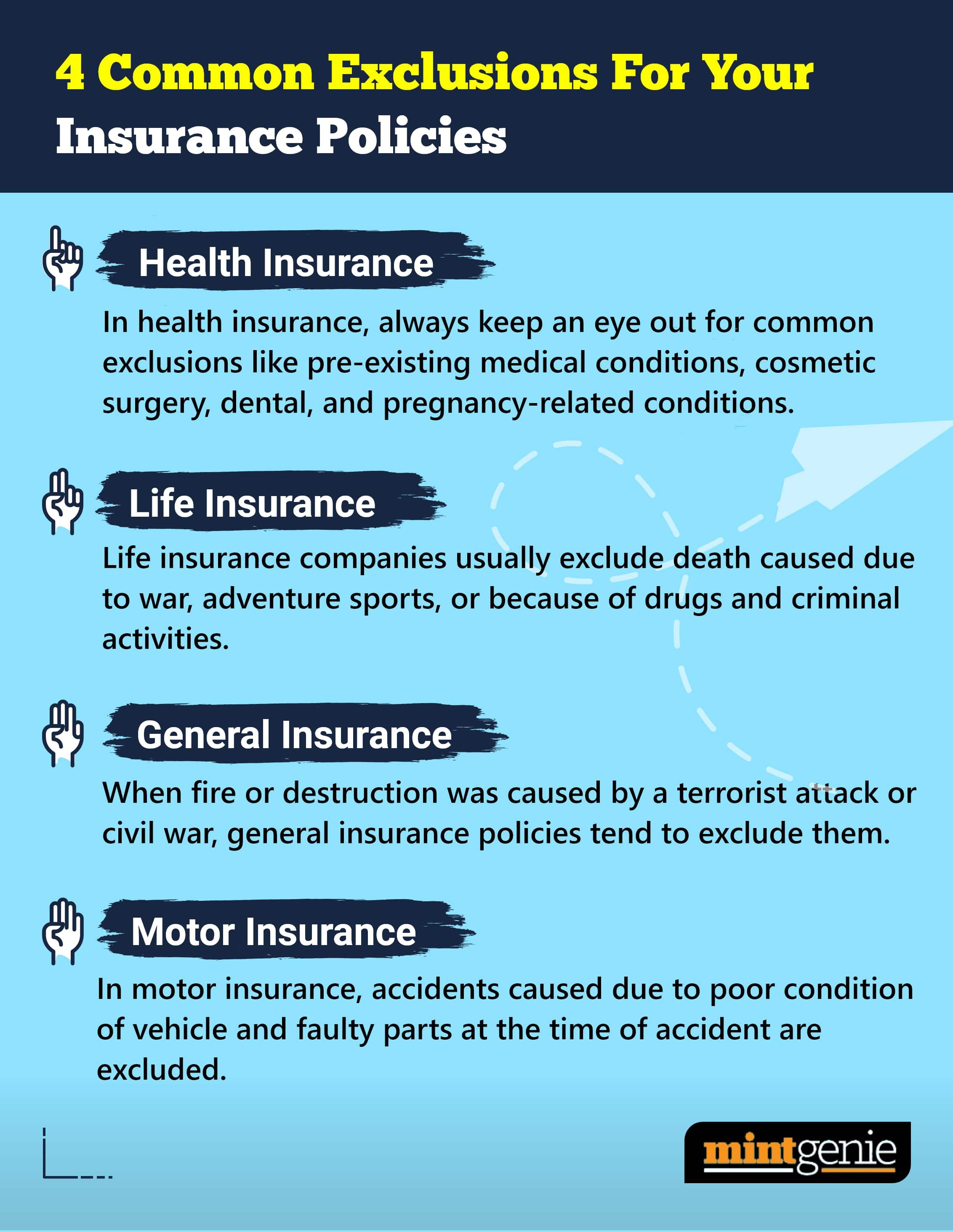

Understand your policy & coverage: When purchasing any type of insurance, it’s important to understand the details of your policy before signing anything. Make sure you know exactly what types of coverage you have, what is excluded, and what limits apply. Be sure to read the fine print and ask questions until you have a clear understanding of the terms and conditions.

Shop around for different options: Don’t fall into the trap of buying the first policy that you see. Take the time to compare different policies from different providers to ensure you’re getting the best coverage for your needs and budget. Look at the amount of coverage, deductibles, and additional features offered to determine which policy is the best fit for you.

Be wary of low prices: Many insurance companies offer low rates as an incentive to entice customers, but those low prices often come with limited coverage and high deductibles. It’s important to read through the details of a policy before signing anything to make sure you’re not sacrificing important coverage in exchange for lower prices.

Know what you're paying for: Many insurance policies contain payment terms that may seem beneficial at first, but in reality, they are really just a way for the company to make more money. For example, some policies require the policyholder to pay for all repairs up front and then receive reimbursement from the insurance company later. This type of arrangement can be very expensive, so make sure you review the payment terms before agreeing to them.

Tax season is a time of great stress and confusion for taxpayers and it’s important to be aware of the various insurance traps that might come your way. It is advisable to assess your overall financial goals and risk tolerance before investing in any policy and verify the information provided to them before taking any action.