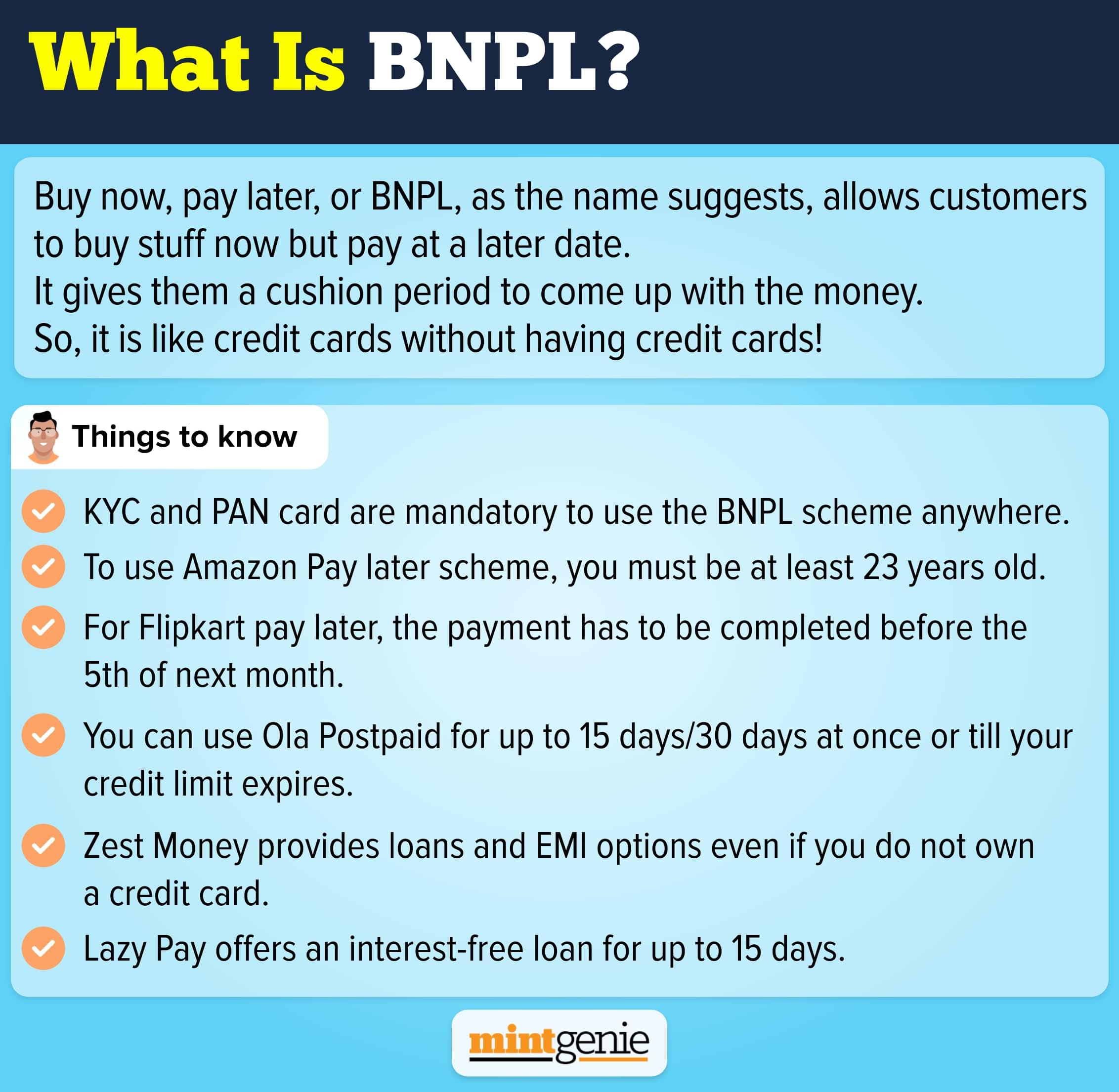

_1639560676401_1648464616068.jpg&w=3840&q=75)

Will payments using the Unified Payments Interface (UPI) mark the end of Buy Now, Pay Later (BNPL) schemes? The BNPL scheme that came in as a feasible alternative to credit card payments was preferred by people who wanted to pay for their purchases in instalments sans the high-interest rate or penalties that credit card companies charge.

Once hailed as the greatest innovation in payment solutions owing to its accessibility, the BNPL scheme was set to change the way lending companies work.

The race to stay ahead comes in the wake of data revealing how mobile payments continue to occupy an incremental market share rapidly. Currently, mobile payments constitute 52 per cent of retail digital payment-to-merchant (P2M) payments during the FY22. With the number of overall UPI payments going up at a rapid pace, the overall payments fee yields are now much lower.

Spending through credit cards has also been going up steadily, though the portfolio re-leveraging has been much lower. Though the number of people warming up to BNPL schemes has gone up considerably over the past few years as few players have begun to clock meaningful scale in Gross Merchandise Value (GMV). Numbers cite increasing adoption by customers and increased number of use cases as the propelling force behind rising BNPL volumes.

BNPL players face the heat

Despite being on a high by as much as six times in FY21 alone, the earning profiles of new-age BNPL players are still developing gradually. This can be attributed to the high growth that continues to affect their earnings either as increased investments or extreme negligence. Besides, BNPL players feel marred owing to the lack of customer-driven revenues accompanied by high credit costs and cost of capital, thus, denting business viability to a huge extent. Companies are now trying to recover their losses by focusing on selling products like equated monthly instalments (EMIs), personal loans and other financial products.

Relying on traditional card payments

BNPL players faced with limited sources to earn profits are now slowly moving toward traditional products including virtual credit cards, digital savings accounts (with debit cards), etc. The tilt towards credit card use is to drive customer-driven income along expected lines.

The current market volatility has resulted in a steep correction in the share prices of Fintech companies both in India and abroad, thus, resulting in a spillover impact on the valuations of unlisted BNPL players apart from their listed counterparts. However, smaller companies in this industry will show a greater likelihood of achieving economies of scale.

The Reserve Bank of India is now contemplating the need to regulate the working of BNPL and consumer lending apps.