Car loans have made it very simple to afford a car. Earlier buying a car was a lot of work, but with banks now offering multiple incentives and digitization of most processes, taking a car loan has become a pretty uncomplicated process.

An RBI report dated 1st July 2021 shows encouraging growth in the personal loan category, especially housing and vehicle loans. Moreover, the growth in vehicle loans exceeded its pre-COVID-19 levels for both public and private banks, the report added.

Now an individual can take ownership of the car at just a fraction of the cost and pay the remaining through EMIs over a period of time.

While there are a variety of options available, there are still a few checks and balances an individual has to undergo, in order to get a car loan.

READ MORE: Is it prudent to opt for fixed rate on car loans in the rising interest rate scenario?

Eligibility

In order to get a car loan, the first and foremost thing is to check the car loan eligibility criteria for your desired bank. These include minimum age, minimum annual income, employment status, and/or any other criteria that the bank may have.

For instance, in Axis Bank, for a salaried person, the minimum age must be 21, the minimum annual income should be Rs. 2.4 lakhs and must be employed for at least 1 year, while for a self-employed person, the minimum age is 18, minimum annual income is Rs. 1.8 lakhs- 2.4 lakhs and should be in the same line of business for at least 3 years. Similarly, one can check the eligibility criteria for their respective banks.

Verification

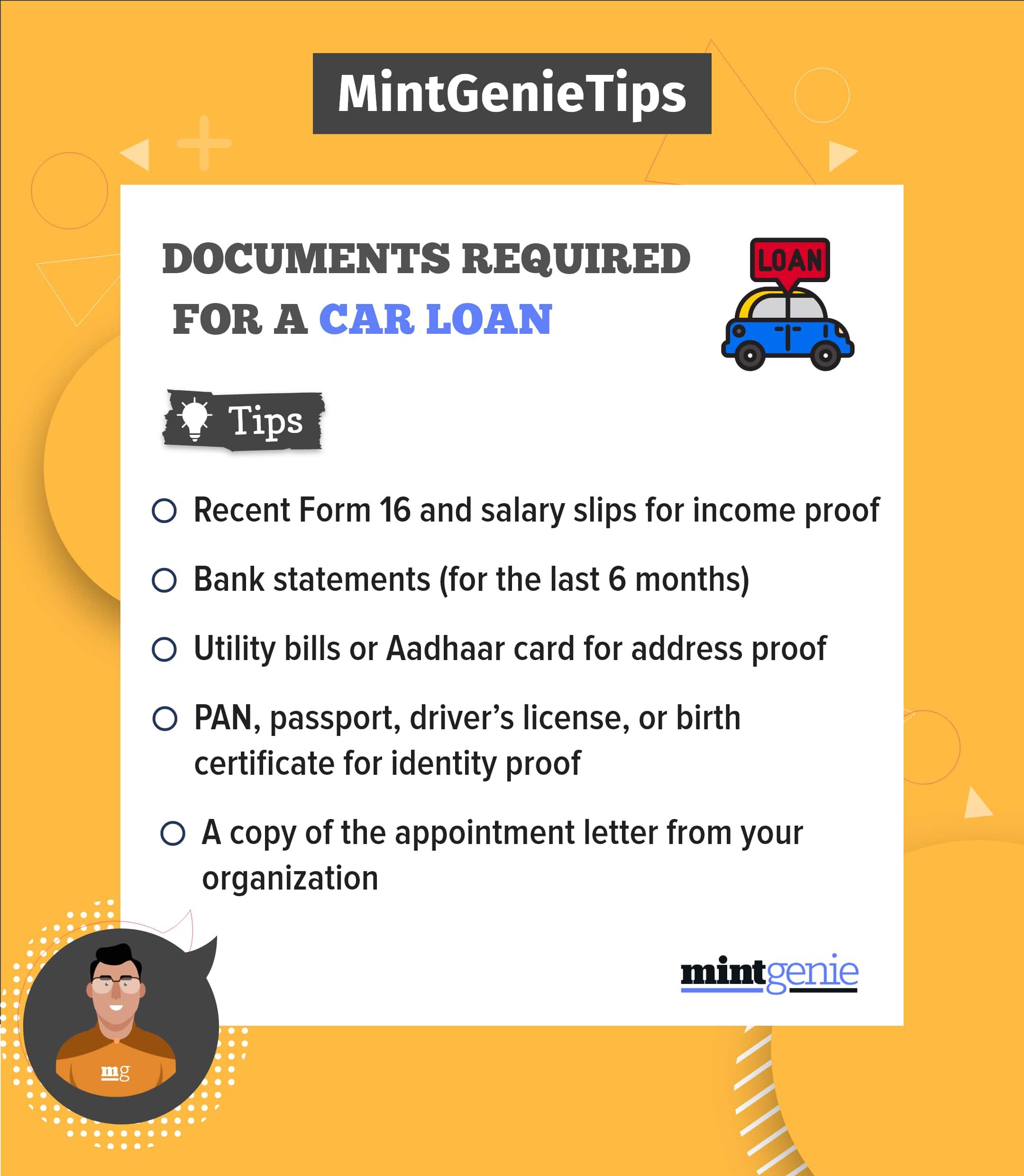

If you are eligible for a car loan, the next step is to verify your identity. In order to do that, you have to submit identity proof which could be PAN, Passport, Aadhar card, Voter ID as well as address proof which could be utility bills or bank passbooks to your lender.

READ MORE: Thinking of taking out a car loan? Analyze these 6 factors first

Apart from these, you also have to submit some other basic documents. These include:

Application form- To apply for a car loan, one must fill out the application form requesting the same.

KYC- This process requires the applicant to further submit their photographs, Identity Proof (like Aadhaar Card, etc.), Address Proof (like Aadhaar Card, Driver’s License, etc.), and Age Proof.

Bank Statement- Applicants must submit their bank statements for signature verification.

Income Proof- For a salaried person, the bank requires to submit the latest salary slip or Form 16. For a self-employed person, the income proof shall be the Income Tax Returns for the previous 2 years.

Other Documents- Some banks may also ask for employment stability proof from salaried persons or business ownership proof from self-employed persons.

Credit history

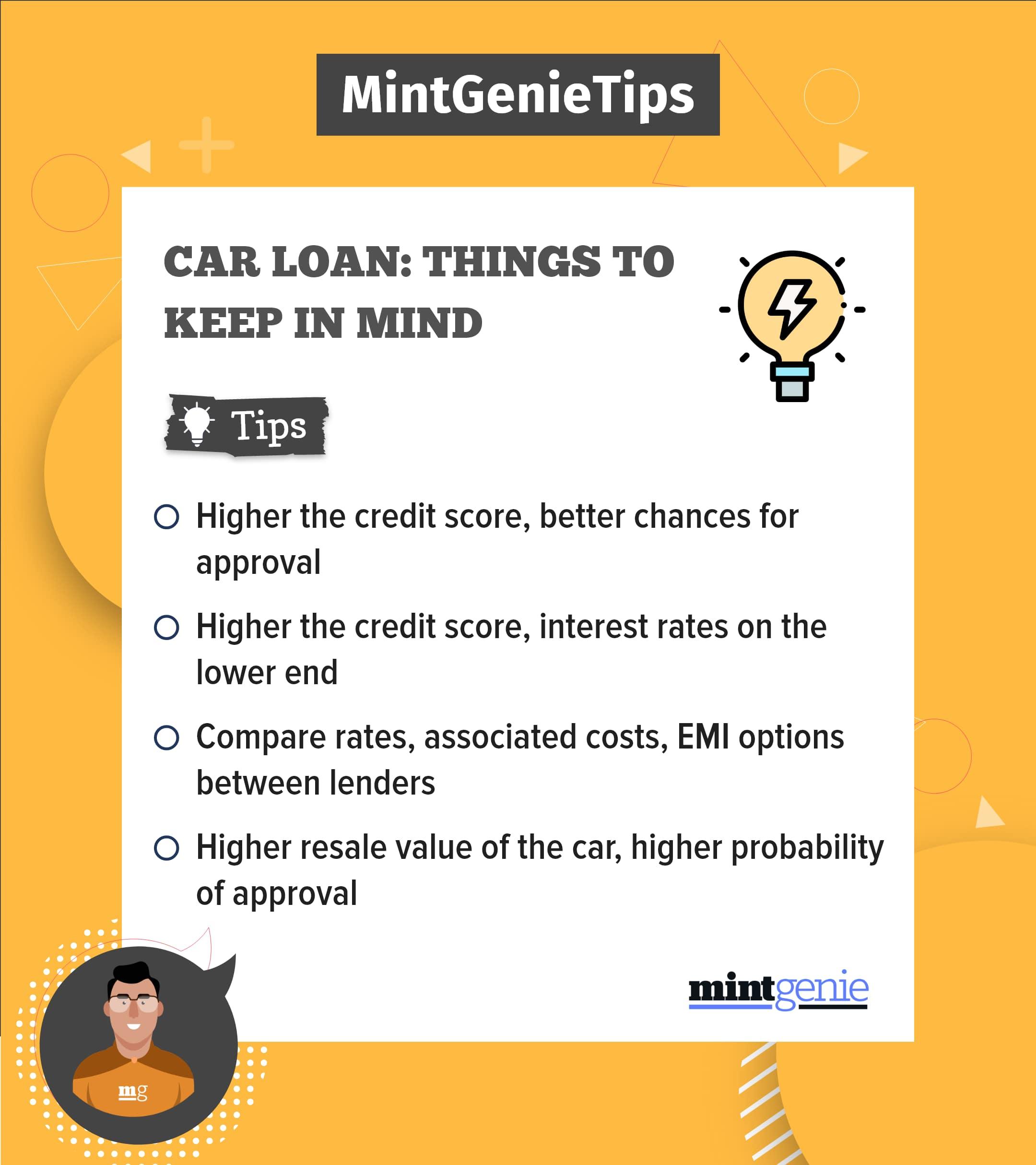

This is a very important aspect to get any kind of loan. This reflects your financial stability and gives a clear view to your lender regarding your financial history. The credit score depicts the creditworthiness of the applicant and is based on a number of factors, for example, the number of open accounts, total levels of debt, and repayment history, etc. Lenders always check the credit score to evaluate the capacity of the Applicant to repay loans.

The credit score is numbered between 300-850, and the higher the score, the higher the chances for approval on your loan application. It also helps in determining your interest rate for the loan. The higher the credit score, the more you can negotiate for a lower interest rate with your lender.

Driver's license

If you are applying for a car loan, you must have a valid driver's license. This showcases that you are legally allowed to drive before owning a car. Your car loan can get canceled if you have lost your license, or it has expired or been canceled. The lender has to verify you are a responsible driver before approving the car loan.

Type of car

The type of car you want to buy also determines one’s car loan eligibility as well. Since the value of a car depreciates with time, and every car has an estimated resale value based on features and specifications, the resale value of the car also determines the car loan eligibility. Therefore, the higher the resale value of the car, the higher the car loan eligibility.

Your employer’s reputation

It may not always affect one’s eligibility, but sometimes, the brand and the company name help in improving the car loan eligibility. An employee of a high-ranking company or a tier-1 firm may be able to receive a higher loan amount than an employee of another company. So, to get a higher loan amount approved, it is important to have a higher income.

While these are the basic checks that are done before approving a car loan by a lender. There are certain things the applicant must keep in mind before taking a car loan.

1) It is very important to compare interest rates, EMIs, and other associated costs between lenders. Do not just go with your first option. Shop for competitive rates and choose the one which suits you the most.

2) If you have a corpus saved then it is advisable to pay as much as possible in the downpayment. While most auto companies just require 10 percent of the entire vehicle cost as the down payment, your loan amount, as well as the incurred interest, will decrease drastically if suppose you pay 25-30 percent of the vehicle cost as your down payment.

3) Lenders usually offer tenure of 1-7 years for the repayment of a car loan. But the smaller your loan period is, the lesser interest you will be charged.

Applying for a car loan has become pretty easy with more and more banks and financial institutions offering various deals to their customers. However, before applying for a car loan, make sure you compare rates between the lenders as well as fix a budget so that it doesn’t become a burden in the future.