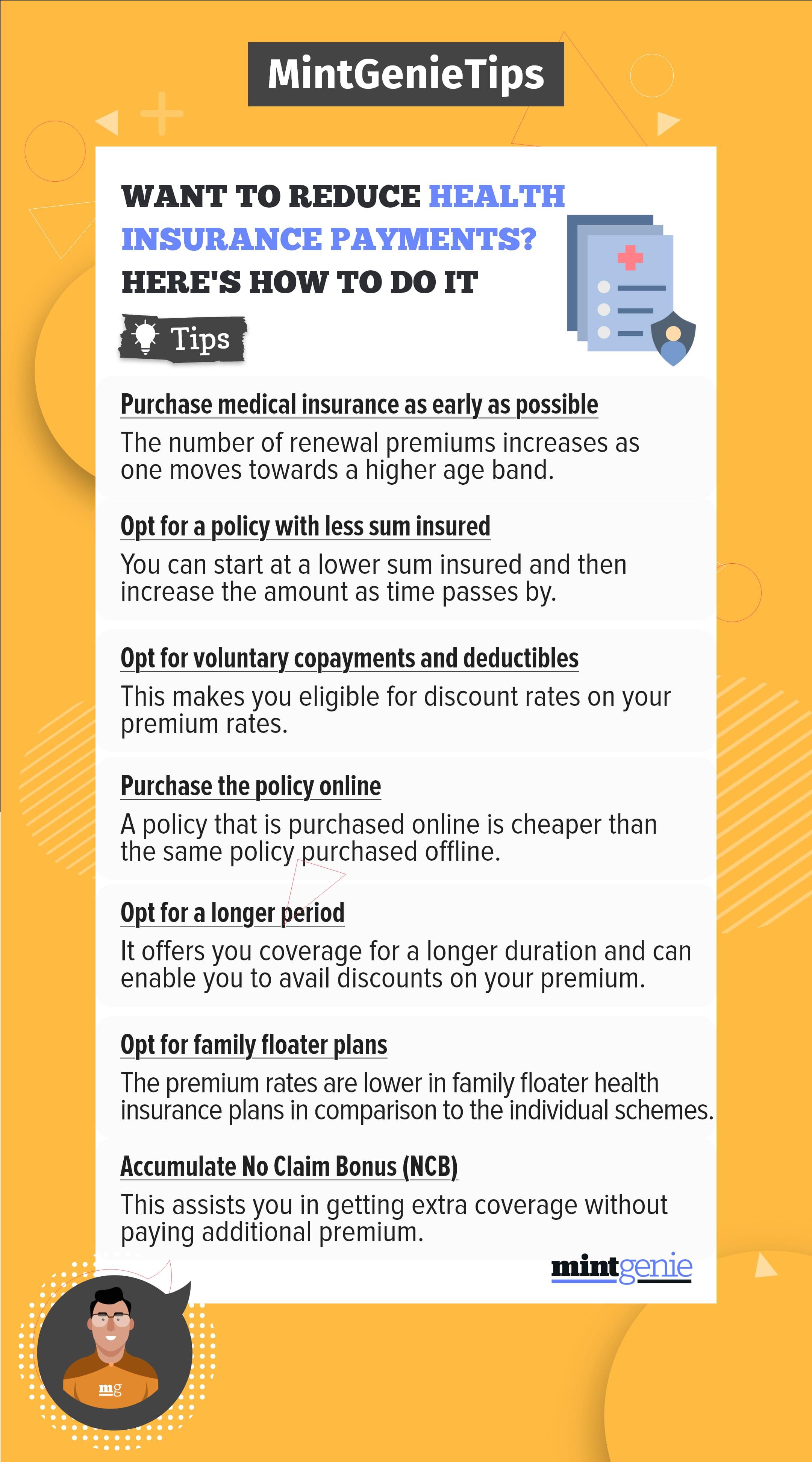

How many times have we heard our friends complaining about how their health insurance companies denied settling their claims citing one reason or the other? The most common reason that health insurers reiterate is the disease wise sub-limits written in the policy that most policyholders tend to ignore.

To understand why many policyholders fail to make health insurance claims, we need to understand some essential components like “sub-limits”. This is also important as they do not go beyond reading the extent of insurance coverage, premium amount and the network hospitals listed with the insurance company.

Understanding sub-limits in health insurance

You do not always get what you pay for. There are limits and then there are sub-limits. The latter is essential and inherent to correctly evaluating the quality of a health insurance policy. To start with, there are two types of sub-limits in any kind of health plan – one pertaining to hospital room rent while the other is on the sum assured on a particular disease. This means that the insurance company fixes a value on the treatment of a particular disease or as a percentage of the total sum insured.

For example, when it comes to securing a room on rent during treatment, many insurance companies put a cap on the daily room rent, the type of room to be secured and hospital charges linked to taking the room on rent. Also, some insurance companies may require their customers to pay the charges over and above the sub-limits mentioned in the policy documents.

Not realizing how sub-limits can affect your health insurance claim can affect someone dearly. For example, Alok Jain, Founder of Weekend Investing and a Delhi-based research analyst recently tweeted how his friend had received only ₹40,000 for a ₹4 lakh insurance claim as his policy had disease wise sub-limits. Sad but true! Ignorance about sub-limits can cost you in the long run as insurance plans fail to compensate you for the money spent on treatment. With hospital bills going up with every passing year, seeking treatment can make a huge dent in your savings unless you are covered by an adequate health insurance plan.

While buying a health cover, check the details mentioned under the sub-limits section on a specific treatment. There is a cap mentioned on the maximum amount you can claim depending on what kind of disease you suffer from or the treatment you opt for. The remaining billed amount must be borne by the patient. This means that a high insurance cover neither promises you complete coverage nor shields you completely from having to pay your hospital bills.

Yogesh Agarwal, Founder, Onsurity says, "Sub-limits are determined on the basis of a specific disease or treatment procedure. For example, the sub-limit for cataracts is ₹40,000, while for knee replacement it has been placed at ₹1,50,000, even though the sum assured is ₹5,00,000.

Typically, an insurance company benchmarks the market price of treatment and then sets the sub-limit to ensure that it is sufficient to cover the price of such treatment. These limits are placed to ensure that hospitals and customers don’t dramatically increase costs. Through this mechanism, the insurance company is able to avoid misuse of the insurance cover and most importantly restrict their claims cost.

However, the biggest flaw in setting the sub-limit is that they become outdated very quickly. With medical inflation roughly at 14 per cent in India, chances are that these sub-limits will always be lower than the current market price of such treatments. This means that even if the current sum insured is ₹5,00,000, the customer remains underinsured.

Sub-limits are predetermined for a particular claim. They are generally framed depending on the prevailing market rates for a particular procedure. In addition, they help reduce instances of fraud and considerably curtail the cost inflation of procedures."

Buying health insurance sans sub-limits

Since sub-limits refer to the monetary caps placed by insurance companies on your health policy, you may find them an unnecessary inclusion that prevents you from recovering the coverage mentioned in the document. In that case, you may opt for a comprehensive health cover without sub-limits, though the premiums to be paid on it would be considerably higher. Since the inclusion of the sub-limits translates to low premium charges, you must be aware of how much you have to pay over and above what the bills your insurer would cover in the event of hospitalization and subsequent treatment.

Know your insurer

The policy document you are signing is essentially a contract between you and the insurer. So, you must be well aware of the insurance company from whom you are seeking the necessary services. Agarwal adds, “Choosing the right insurer is as important as choosing the right product. Before buying insurance, make sure to understand the company’s claim settlement ratio. Also, the company must have an efficient customer support team and offer best-in-class customer experiences. The right insurance policy should be able to effectively mitigate unforeseen financial losses and so it is crucial to understand a policy’s terms and conditions before its selection.”

You may as well go to the Insurance Regulatory Development Authority of India (IRDAI) website to check the claim settlement ratio of the different insurance companies and then decide accordingly.

Credibility matters, and so you must avoid insurance companies in the constant limelight for failure to pay the coverage amount as and when required. Your insurance company must have an impressive track record, a good network of hospital coverage for you to seek cashless treatment, a high claim settlement ratio and a decent incurred claims ratio. Numbers matter, so a high incurred claims ratio of more than 100 implies that the company may not be financially stable while the same ratio on the lower end may imply that the company may not be paying out the high-value claims.

Beware of disease wise sub-limits that some companies include in fine print to avoid paying a high coverage amount on the treatments mentioned in the policy.