In the first part of this series on Emergency Fund, MintGenie gave you a simple guide on how to go about building your emergency fund.

------------------------------

As we are all aware about the importance of emergency corpus in order to provide financial stability & cushion to one’s life. The wide range of investment options available to park the funds kept aside for emergency could be confusing at times. Further the important question about the returns that this corpus would generate is a tricky one. Keep in mind that you may never face a situation where you have to withdraw your emergency funds and actually use it. Also beyond a certain extent, keeping money in form of cash or in a basic savings bank account could mean a compromise of potential return in long-term.

Let us first analyse various options available to build an emergency corpus:

1) Cash: Cash is the simplest form of maintaining emergency corpus. It is readily available for disposal. However, if the size of emergency corpus is high, keeping a major portion or even entire portion of it in form of cash could bear a potential loss by theft.

2) Savings Bank Account: Parking the funds in savings account is one of the great ways to maintain emergency corpus. Saving account with a debit card linked to it provides easy access to the money in case of emergency. This card can be swiped or used for cash withdrawal purposes at ATMs to meet the funds requirement. Saving account also provides interest on money lying in the account, therefore, is better than cash. In India, we have banks offering interest on savings accounts ranging from 2.5%-6% per annum. Furthermore, there is an income tax deduction up to Rs. 10,000 per annum on interest earned on savings account under section 80TTA. The amount of interest beyond Rs. 10,000 per annum will be taxed as per your slab rates. All of these features make a compelling case for parking your emergency corpus in savings bank accounts.

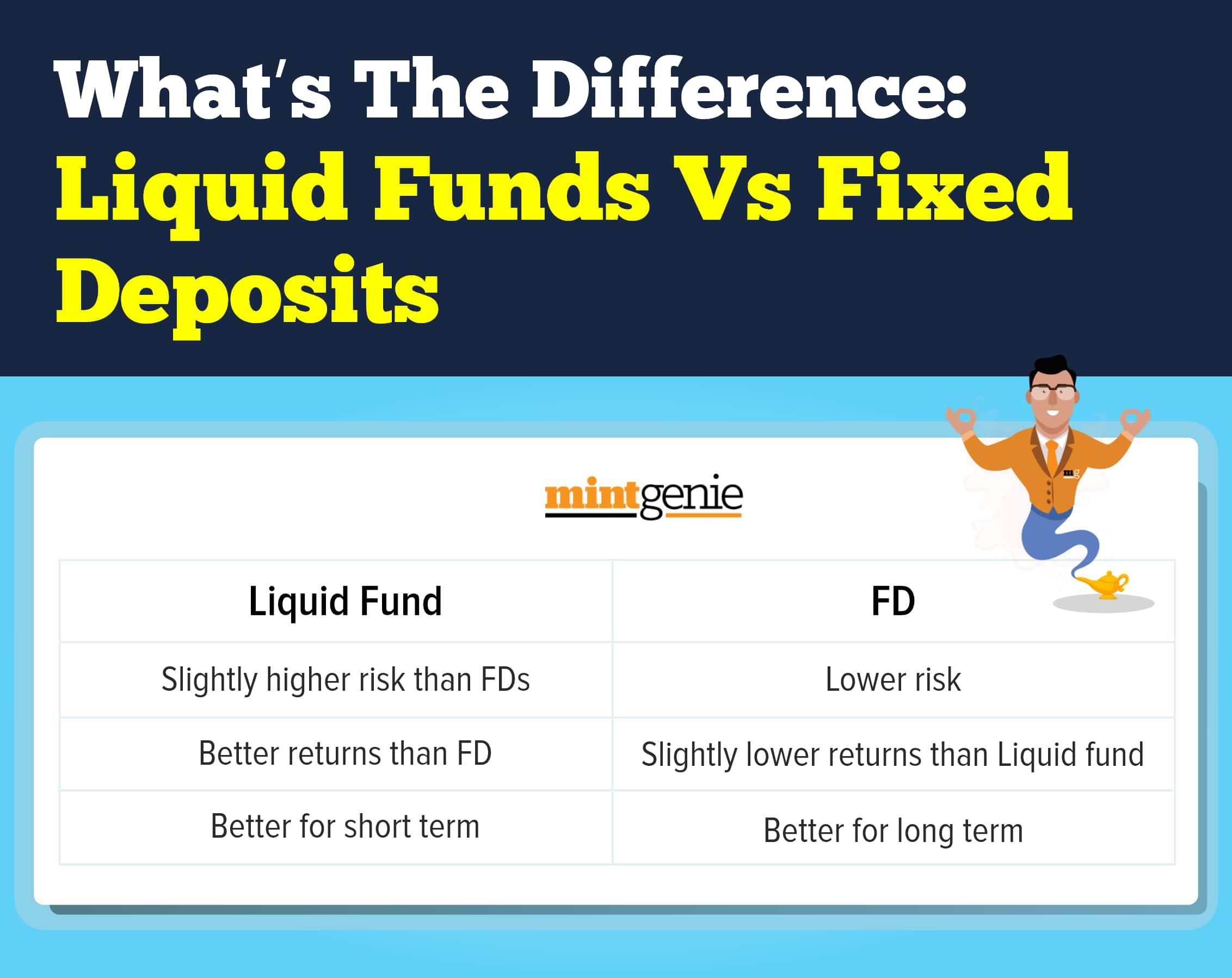

3) Bank Fixed Deposits: Fixed Deposit provides higher interest than savings account but comes with a lock-in period based on the preference of investor. However, fixed deposit can be withdrawn at short notice by paying a small penalty. In case of some banks, fixed deposits can be withdrawn without penalty. Interest earned on fixed deposits can range from 3%-7% per annum. Interest earned on fixed deposits is fully taxable in the hands of individual at his respective slab rate. There is a deduction under section 80TTB of Rs. 50,000 per annum in case the fixed deposit is made by senior citizen.

4) Liquid Funds: Liquid funds are a category of mutual funds where the fund manager has a mandate to invest the money in very short term fixed income instruments like commercial papers issued by corporates. An investor in liquid funds has complete flexibility to invest and withdraw anytime without an significant charges. Returns on liquid funds are in the range of 3%-4% per annum. Income earned from liquid funds is taxed at slab rate of individual. However, if the money is withdraw after 3 years from the date on investment then the returns are taxed at a concessional rate of 20% with the benefit of indexation.

5) Conservative Hybrid Funds: A category of mutual funds where the fund manager has a mandate to invest the money in a mix of equity & debt. However, these funds invest major chunk (70-80%) in debt instruments and remaining in equity & REITs. Having some equity in the scheme provides a kicker to returns over long-term. A lot of traditional knowledge would suggest otherwise, but this is an option that can be considered if the emergency corpus is very high. Some exposure to conservative hybrid funds would generate extra returns & this allocation should be redeem as a last resort in case the emergency arises. Income earned from liquid funds is taxed at slab rate of individual. If the money is withdrawn after 3 years from the date on investment then the returns are taxed at a concessional rate of 20% with the benefit of indexation.

Before we begin with the numbers, Keep in mind that these numbers can vary from person to person. You can have a more conservative approach or aggressive approach.

Let us take few examples to understand the possible allocation methods for emergency corpus:

Case I:

Mr. K is 24 years old (unmarried & no dependents), earns a salary of Rs. 50,000/month with following expenses:

- Necessities: Rs. 8,000 per month for hostel rent & food expenses

- Discretionary: Rs. 4,000 per month on entertainment & sports

- Fixed financial commitments: Rs. 3,000 per month of EMI for his mobile phone

Mr. K should have a minimum of six months of expenses relating to necessities & fixed financial commitments set aside as emergency corpus. This comes to Rs. 66,000 (Rs. 11,000 X 6 months). Since the amount of emergency corpus is not very high, Mr. K can park this amount in a higher interest yielding savings bank account. The interest earned here would not be taxed as same will be covered as deduction under section 80TTA.

Case II:

Mr. J is 40 years old (married & 2 kids), earns a salary of Rs. 2,00,000/month with following expenses:

- Necessities: Rs. 65,000 per month

- Discretionary: Rs. 15,000 per month

- Fixed financial commitments: Rs. 85,000 per month of EMI for his home & vehicle loan

Mr. J should have a minimum of twelve months of expenses relating to necessities & fixed financial commitments set aside as emergency corpus. This comes to Rs. 18,00,000 (Rs. 1,50,000 X 12 months). Since the amount of emergency corpus is very high, here is how he should allocate this amount:

Rs. 2,50,000 in a savings bank account that could yield him 4% per annum. The interest would be Rs. 10,000/year & will be tax free under section 80TTA.

Rs. 5,00,000 in a liquid fund

Rs. 7,50,000 in a fixed deposit

Rs. 3,00,000 in a conservative hybrid fund (this forms only 20% of total corpus, but yields better than the above options in long-term)

A credit card can also be used in case some urgent situation arises & you don't have access to above means immediately. This is a much underrated tool which can also be used as emergency corpus in tough times. However, one should pay off the credit card bill immediately once the above sources are liquidated.

CA Rohit J. Gyanchandani is Managing Director, Nandi Nivesh Private Limited, A Pune based Wealth Management Company.

Follow the entire series on Emergency Funds here.