_1639738429268_1639738438155.jpg&w=3840&q=75)

If you urgently need some money for your house repair or for an unexpected contingency, then there are a dozen ways to borrow money these days. If you have to use the money to buy a product or gadget, you can even use your credit card. Alternatively, you can also borrow money from a fintech app or neo banks. But any expert would advise you blindfolded to first explore the available options with your own bank before jumping onto the new app on the Play Store or App Store.

The bank where your monthly salary is credited can give you a good deal without levying too many hidden charges – a usual occurrence in case of a new app or neo bank.

What is an Insta loan

This is another name for instant loan which is already approved by your bank based on your credit card limit and your past credit history.

For instance, ICICI Bank gives the insta top up loan in mere three clicks without having to coordinate with a banking agent. The repayment can be done in a maximum of 10 years. And the best part is that the entire transaction takes place digitally without any document submission.

Similarly, HDFC Bank gives insta loans to its customers. The repayment can happen in a maximum of five years.

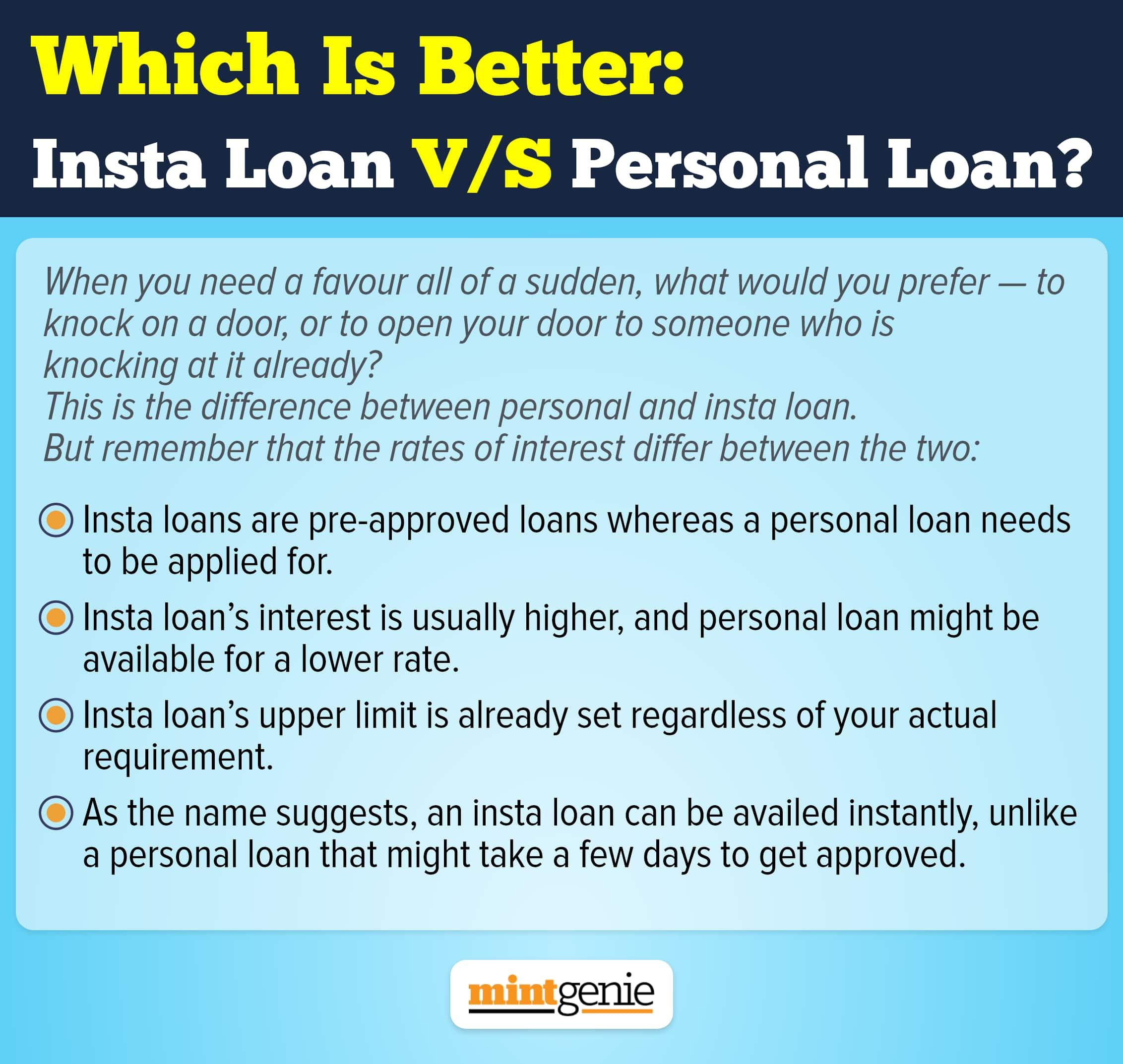

Insta loan V/s Personal loan

Insta loan is a pre-approved loan given up to a certain limit which does not need to be applied for. On the other hand, a borrower needs to apply for a personal loan. A borrower needs to show their income tax returns for the past three years, or salary slips for past three months.

The lending bank also checks the credit worthiness of the borrower before their application for personal loan is approved.

For example, if a customer Mr Suhas has a pre-approved insta loan offer of ₹5 lakh at the rate of 15 percent per annum, then Suhas can borrow any amount up to the maximum limit of ₹lakh at the given rate. There is no application that needs to be submitted, and no documents to be shown. Just a few clicks, and the loan money will be transferred to the bank account.

On the other hand, if Suhas needs ₹12 lakh, he has two options: the first is to borrow ₹5 lakh from the pre-approved offer and to borrow the remaining ₹7 lakh as personal loan. The second option is to borrow ₹12 lakh as personal loan. The second option can be better so long as he gets a lower rate of interest. But if his personal loan offer is approved for a maximum of 7 lakh, then he can take both the loans to meet his ₹12 lakh requirement.

In both the options, the customer has a pre-approved loan offer which he can avail. Upon the acceptance of the offer, the loan amount is directly credited to the customer’s account.

Rate of interest

One key difference between insta loan and personal loan is the rate of interest. Insta loans are usually linked to the credit card and hence, its rate of interest is relatively higher, whereas the personal loan’s interest is slightly lower, which depends on an interplay of factors including your credit worthiness and the organization you work for.

“One can get a personal loan for a rate which is slightly higher than 10 percent per annum, whereas the rate on insta loan can be as high as 20 percent. But it can vary depending on the bank or the customer,” says Deepak Kumar Aggarwal, Delhi-based chartered accountant and finance advisor.

So, we can summarise that insta loan and personal loan both have their unique features and can be chosen over one another depending on the borrower’s prevailing circumstances and the rate of interest offered by the bank.