The new range of Apple iPhones is finally here. Unveiled at a glitzy event on September 07 this year, the new iPhone 14 series includes iPhone 14, iPhone 14 Plus, iPhone 14 Pro and iPhone 14 Pro Ma. Apple iPhone 14 Pro is available with a whopping starting price tag of $999 (79701.42 INR). The costlier version is the iPhone 14 Pro Max which can be bought at $1,999 (159482.62 INR) onwards. For sports enthusiasts, the company also launched the Apple Watch Ultra along with the next-generation Apple AirPods.

New iPhone 14: Do you need it or do you want it? Here's how you can multiply your wealth if you learn the difference

TL;DR.

The new version of iPhones and AirPods is the new buzzword. However, the craze for these new gadgets does not necessarily have to bring about a financial storm in your life or create that unwanted dent in your pocket.

While all these launches highlight the love for technology and the new generation’s love for gadgets, the price tag is a cause of concern. The biggest underlying question “Is it worth the money that you would spend on them?” What matters is whether the watch would be an investment or just another gadget that would lose its value and utility over time.

Many youngsters feel tempted to buy the new range of iPhones released regularly. While there is nothing wrong with harbouring a love for innovative tech gadgets, many fail to understand the thin line of difference that distinguishes needs from wants. Think of how much you stand to gain if you invest the same money in a mutual fund instead of wasting it on a gadget that would lose its sheen and shine with time.

Not everyone has knowledge of how to earn from the market. This brings forth the utility of mutual funds that do much good in helping investors park money in the market without having to dabble in stocks. Take for example the Mirae Asset Large Cap Fund which has earned over 40 per cent returns in the past five years. Then, there is the Kotak Bluechip Fund which boasts of more than 50 per cent returns in the last five years. There are more such large-cap funds that expose your money to investments in companies with huge capitalization, thus, helping you earn returns with comparatively lesser risk.

Earning from large-cap fund investments

Assuming that you would be paying for the phone in a lump sum, let us check how much you would earn if you were to put the same money into some of the top-performing mutual funds. Instead of buying the Apple iPhone 14 Pro at roughly ₹80,000, let us assume that we invest the same amount in a large cap mutual fund. The iPhone 14 Pro Max is available at approximately ₹1,60,000. Let us check how much we would earn in the next five years on parking the same amount in some of the top-performing large-cap mutual funds that have helped investors create a corpus in the past five years.

| Name of the large-cap fund | Underlying index | Rate of returns over the past five years (in %) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) |

| Axis Bluechip Fund | S&P BSE 100 Total Return Index | 14.36 | 80,000 | 1,56,481 | 1,60,000 | 3,12,961 |

| ICICI Prudential Bluechip Fund | NIFTY 100 Total Return Index | 12.21 | 80,000 | 1,42,314 | 1,60,000 | 2,84,628 |

| Mirae Asset Large Cap Fund | NIFTY 100 Total Return Index | 13.00 | 80,000 | 1,47,395 | 1,60,000 | 2,94,790 |

| Nippon India Large Cap Fund | S&P BSE 100 Total Return Index | 13.26 | 80,000 | 1,49,098 | 1,60,000 | 2,98,197 |

| SBI Bluechip Fund | S&P BSE 100 Total Return Index | 12.16 | 80,000 | 1,41,997 | 1,60,000 | 2,83,995 |

Earning from mid-cap fund investments

No doubt these funds are risky owing to their investments in companies with a market capitalization in the middle range of listed stocks. Mid-cap stocks have been found to earn more wealth than their large-cap peers, though their volatility has caused many investors unwanted heartache. However, they are still less volatile and assume much lesser risk than funds parking money in small-cap stocks.

| Name of the mid-cap fund | Underlying index | Rate of returns over the past five years (in %) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) |

| Axis Midcap Fund | S&P BSE 150 Midcap Total Return Index | 18.81 | 80,000 | 1,89,389 | 1,60,000 | 3,78,778 |

| Edelweiss Mid Cap Fund | NIFTY Midcap 150 Total Return Index | 17.24 | 80,000 | 1,77,202 | 1,60,000 | 3,54,404 |

| Kotak Emerging Equity Fund | NIFTY Midcap 150 Total Return Index | 17.01 | 80,000 | 1,75,471 | 1,60,000 | 3,50,942 |

| SBI Magnum Midcap Fund | NIFTY Midcap 150 Total Return Index | 15.72 | 80,000 | 1,66,009 | 1,60,000 | 3,32,018 |

| UTI Mid Cap Fund | NIFTY Midcap 150 Total Return Index | 13.55 | 80,000 | 1,51,017 | 1,60,000 | 3,02,034 |

Earning from small-cap fund investments

Observe the historic returns from small-cap funds, and you will realize they are worth the innate stress and extremely volatile movement. These funds park money in stocks from the small-cap category that includes all the stocks listed in the markets, barring the largest 250 stocks (by market capitalization). Avoid these funds if you are risk-averse. However, if you are in here for high returns irrespective of how the market behaves or which way it sways, they may just be the right investment vehicle for you.

| Name of the small-cap fund | Underlying index | Rate of returns over the past five years (in %) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) |

| Quant Active Fund | Nifty 500 Multicap 50:25:25 Total Return Index | 23.30 | 80,000 | 2,27,985 | 1,60,000 | 4,55,969 |

| Invesco India Multicap Fund | Nifty 500 Multicap 50:25:25 Total Return Index | 12.70 | 80,000 | 1,45,449 | 1,60,000 | 2,90,897 |

| Sundaram Multi Cap Fund | Nifty 500 Multicap 50:25:25 Total Return Index | 13.59 | 80,000 | 1,51,283 | 1,60,000 | 3,02,566 |

| ICICI Prudential Multicap Fund | Nifty 500 Multicap 50:25:25 Total Return Index | 13.22 | 80,000 | 1,48,835 | 1,60,000 | 2,97,670 |

| Nippon India Multi Cap Fund | Nifty 500 Multicap 50:25:25 Total Return Index | 14.66 | 80,000 | 1,58,544 | 1,60,000 | 3,17,088 |

Earning from hybrid fund investments

Investing in a fund that parks in stocks of myriad market capitalizations can help you earn over every business cycle. This is because not all stocks perform always. Putting money in hybrid funds allows you to put money in stocks that perform over various business cycles, thus, allowing you to earn every quarter.

| Name of the balanced advantage fund | Underlying index | Rate of returns over the past five years (in %) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) | Lump sum investment (in Rs) | The total value of the investment after five years (in Rs) |

| HDFC Balanced Advantage Fund | NIFTY 50 Hybrid Composite debt 50:50 Index | 13.38 | 80,000 | 1,49,890 | 1,60,000 | 2,99,780 |

| DSP Flexi Cap Fund | NIFTY 500 Total Return Index | 13.29 | 80,000 | 1,49,296 | 1,60,000 | 2,98,592 |

| Edelweiss Balanced Advantage Fund | NIFTY 50 Hybrid Composite debt 50:50 Index | 12.52 | 80,000 | 1,44,291 | 1,60,000 | 2,88,582 |

| ICICI Prudential Balanced Advantage Fund | CRISIL Hybrid 50+50 Moderate Index | 10.93 | 80,000 | 1,34,380 | 1,60,000 | 2,68,760 |

| Nippon India Balanced Advantage Fund | CRISIL Hybrid 50+50 Moderate Index | 9.93 | 80,000 | 1,28,431 | 1,60,000 | 2,56,863 |

Compounding over time

Time is the biggest factor other than the return rate for investments. If you have an amount equivalent to the cost of the new iPhones lying in your bank and are not willing to dabble much in the market, you can always consider buying a corporate bond with your money and wait to see your returns unfold during the period. However, these bonds are time bound, which means that you cannot withdraw the money before the stipulated period without incurring a penalty as mentioned in the bond documents.

| Name of the corporate bond | Returns rate over five years (in %) | Lump sum investment (in Rs) | Total value of the investment after five years (in Rs) | Returns rate over 10 years (in %) | Lump sum investment (in Rs) | The total value of the investment after 10 years (in Rs) |

| Aditya Birla SL Corporate Bond | 7.13 | 80,000 | 1,12,887 | 8.28

| 80,000 | 1,77,244 |

| 1,60,000 | 2,25,775 | 1,60,000 | 3,54,489 | |||

| L&T Triple Ace Bond | 7.01 | 80,000 | 1,12,257 | 7.30

| 80,000 | 1,61,840 |

| 1,60,000 | 2,24,513 | 1,60,000 | 3,23,681 | |||

| HDFC Corporate Bond | 6.92 | 80,000 | 1,11,785 | 8.18

| 80,000 | 1,75,614 |

| 1,60,000 | 2,23,571 | 1,60,000 | 3,51,229 | |||

ICICI Pru Corporate Bond

| 6.80 | 80,000 | 1,11,159 | 7.85

| 80,000 | 1,70,330 |

| 1,60,000 | 2,22,319 | 1,60,000 | 3,40,660 | |||

Kotak Corporate Bond

| 6.77 | 80,000 | 1,11,0031 | 7.75

| 80,000 | 1,68,757 |

| 1,60,000 | 2,22,007 | 1,60,000 | 3,37,515 |

Knowing what you need and then curtailing spending on your wants to secure your financial health is the first step to ensuring financial success. Unfortunately, due to a lack of financial literacy, many youngsters are relying on credit cards to make such purchases. Apart from the money getting wasted on gadgets rooted in status consciousness and brand loyalty, they incur debt at high-interest rates, thus, forcing them to repay loans or opt for debt consolidation to escape the high-interest burden.

Money makes money. Living a debt-free life is quite underrated. Not carrying the most updated version of the iPhone will not kill you nor will dent your position in front of your peers. You can save yourself from many financial miseries if you stop worrying about what other people think of you.

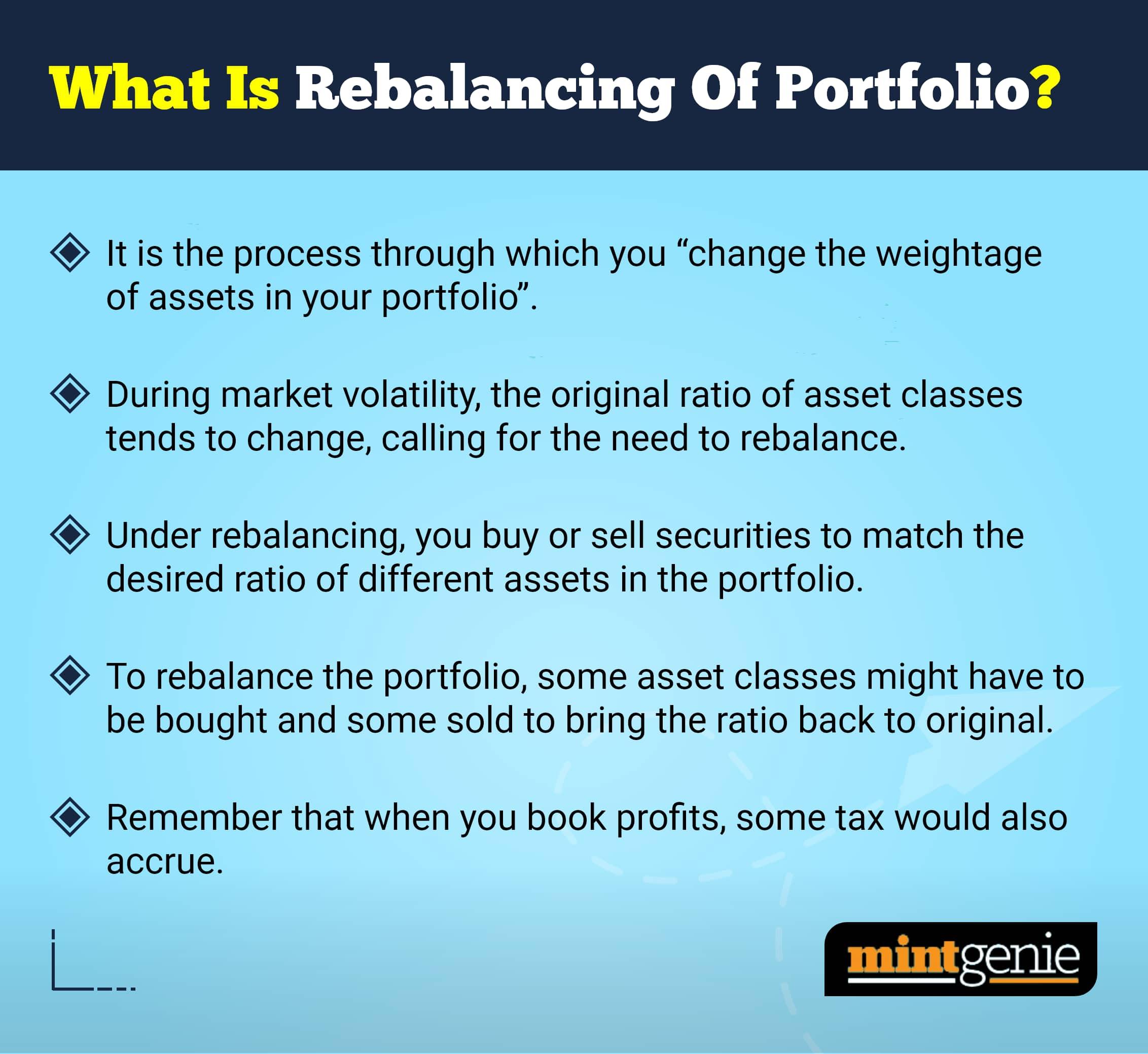

Rebalancing of a portfolio is the process through which you change the weightage of assets in your portfolio.

First Published: 08 Sep 2022, 02:22 PM IST

Related Stories

personal finance

Ganesh Chaturthi: Follow the Lord of new beginnings and start your investments early to make the most of compounding

Team MintGenie