The pension system is an integral part of the economic and social security system of a country. It provides financial security to elderly citizens and helps them meet their daily expenses. In India, the pension system has gone through several changes over the years, from the Old Pension Scheme (OPS) to the New Pension Scheme (NPS).

The old pension scheme and the new pension scheme are both retirement savings plans, but they differ in terms of their approach to creating a secure financial future.

While the old pension scheme provides a guaranteed stream of income after retirement, NPS goes one step further by investing part of the money in the stock market, thus providing the potential for higher returns.

However, with this increase in potential comes increased risk, as the performance of the investments is not guaranteed and the returns depend on the subscriber's ability to make wise asset allocation decisions throughout their employment years.

Let us understand it in detail.

What is Old Pension Scheme?

The old pension scheme was introduced in the 1950s and is applicable only to government employees. Under this scheme, government employees are entitled to receive 50% of their last drawn basic salary plus a dearness allowance upon retirement or an average of their wages over the previous ten months of employment, whichever is more favourable to them.

Additionally, they must satisfy a 10-year service requirement in order to become eligible for the pension benefits. This scheme does not require any employee contributions and provides a guaranteed income after retirement.

What is New Pension Scheme?

The new pension scheme was introduced by the National Democratic Alliance (NDA) government in December 2003 and came into effect on April 1, 2004. It is applicable to both government and private sector employees. Under the NPS, employees contribute 10% of their base pay, while their employers can contribute up to 14%.

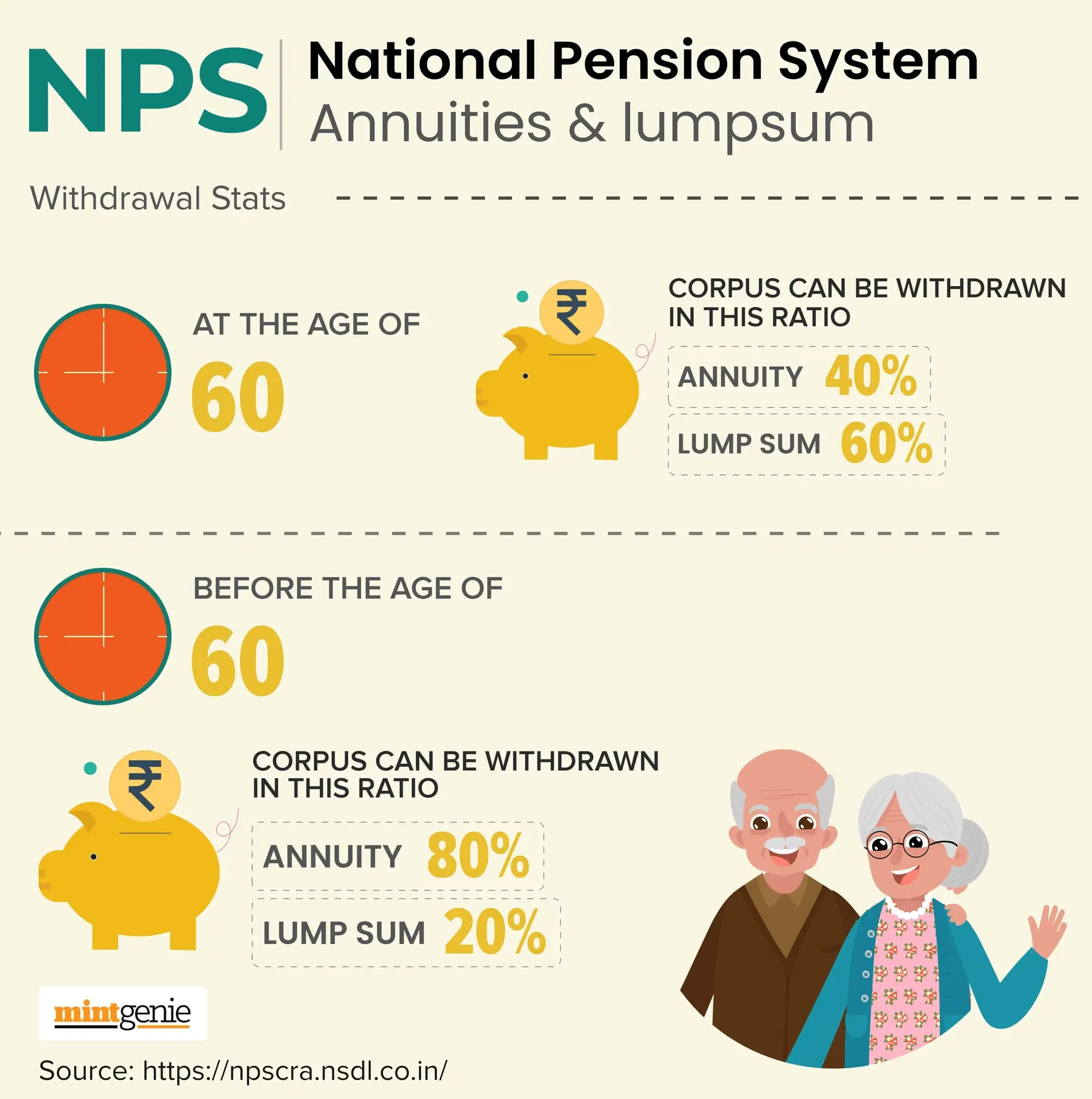

Private sector employees also have the option to actively participate in the NPS. With this scheme, consumers have more freedom and control over their destiny, as they can benefit from market-linked returns without any guarantee of returns. Additionally, 60% of the corpus on maturity is tax-free, while the remaining 40% must be invested in annuities that are 100% taxable.

How is old pension scheme different from new pension scheme?

Return Certainty: The old pension scheme provides return certainty, as it bases the monthly pension on the last wage received by the employee. On the other hand, the new pension scheme offers market-linked returns without any guarantee.

Tax Benefits: Under the old pension scheme, income is not subject to taxation. However, under the new pension scheme, 60% of the corpus on maturity is tax-free, while the remaining 40% is taxable when invested in annuities.

Eligibility: Only government employees are eligible for receiving a pension under the old pension scheme after retirement. On the other hand, the new pension scheme can be availed by all citizens between 18 and 65 years.

Contributions: Monthly payments under the old pension scheme are equivalent to 50% of the last salary drawn. In the new pension scheme, employees are required to contribute 10% of their salaries, while employers can contribute up to 14%.

Flexibility: The old pension scheme did not have much flexibility as it provided a fixed monthly income. The new pension scheme, however, gives the subscriber more freedom and control over their finances. They have the option to choose their asset allocation, allowing them to generate higher returns and build a larger retirement corpus.

Both the old pension scheme and the new pension scheme have their own advantages and disadvantages. While the OPS provides return certainty and income that is not subject to taxation, the NPS offers more freedom, control, and potentially higher returns. It is important to understand these schemes and compare them before deciding which one is best suited for your needs.