The government should consider reducing GST on health insurance premiums to 5 percent from 18 percent in the upcoming Budget to make it more affordable for middle class, says Priya Deshmukh Gilbile, Chief Operating Officer, ManipalCigna Health Insurance Company.

"A GST rate cut from 18 percent to five percent on the health insurance premiums will be a huge respite, especially, for senior citizens who are struggling to meet the rising healthcare costs," she said in an interview with MineGenie.

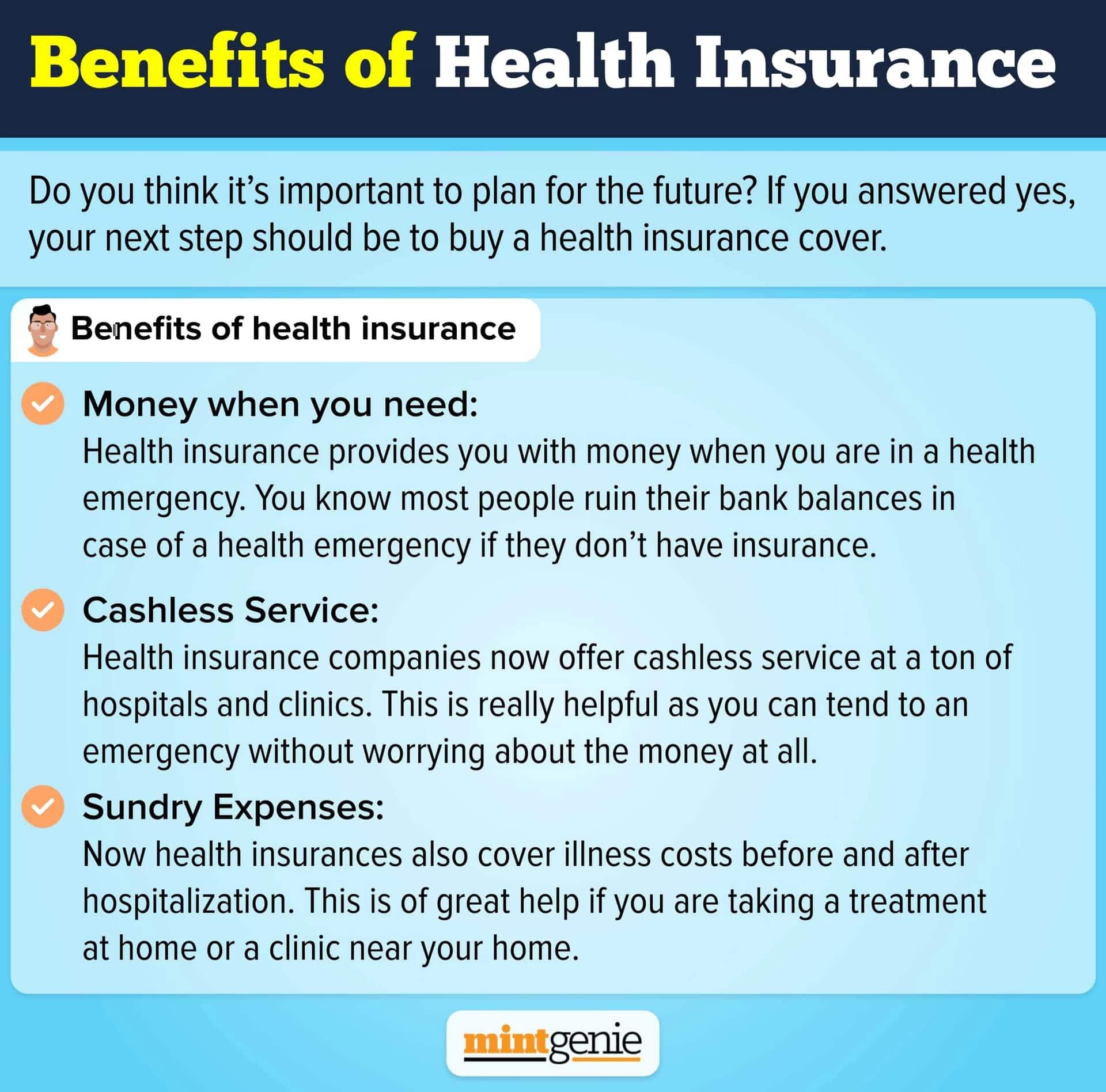

According to her, one needs to have a health insurance coverage of at least ₹10 - ₹20 lakh to meet any form of treatment or hospitalisation costs of significant illnesses.

Edited excerpts:

Q. The IRDAI has asked health insurers to access a national list of doctors. How will this practice help people who have bought health insurance?

Answer: The practice will essentially ensure that there is a repository of doctors available with insurers which can be further used to ensure that a consistent level of medical care is delivered to the customers. Customers can be steered into the hospitals and centres where these doctors are available to ensure an appropriate level of medical care is administered. It will also help mitigate the risk of fraud and abuse along with the risk of poor quality of care for the consumer.

Q. Do you think Indians take adequate health coverage? What should be the average health coverage for an individual in different age groups or a nuclear family?

Answer: Given the constantly rising healthcare costs and lifestyle diseases, it has become essential for individuals to buy a higher sum insured health insurance plan. A family floater health insurance policy of around ₹5 lakh was a common cover before COVID-19. However, people have come to realise that it may not be sufficient in the post-pandemic world. Hence, the conversation has shifted now from 'whether one needs health insurance' to 'how much health insurance one needs'. Considering the continuously rising medical inflation over the past decade, one needs to have health coverage of at least ₹10 - ₹20 lakh to meet any treatment or hospitalisation costs of significant illnesses.

Most insurers also offer a restoration or recharge benefit in their core product proposition which works really well in a floater cover and acts as a backup for the family. Alternatively, you may increase the sum insured by purchasing a super top-up plan. However, you should always consider the growing inflation and be ready for it. The policy you opt for should be from a long-term perspective. Also, it is important to opt for a health insurance plan at the earliest and not let any unforeseen hospitalisation claims eat up your hard-earned retirement savings.

Q. A lot of people don’t take health insurance because they feel coverage from their employer is enough. What do you have to say about it?

Answer: The advantage of a group policy is that it doesn’t have any waiting period for its members. However, if your employer decides to stop the group cover or asks you to bear the price for the same or you switch jobs, you may end up with no cover. This is why, it is important to opt for an individual health insurance policy in addition to group coverage, to stay sufficiently covered for unforeseen exigencies and protect your hard-earned savings. Further, employers can only cover up to a specific amount in a group health coverage policy. So, medical treatment or hospitalisation costs may become unaffordable if critical illnesses, such as kidney failure, cancer, or heart issues need to be addressed.

While group health insurance plans are cost-effective for your organisation, it only works as long as you are employed with your current employer. As time passes, you may find it challenging to purchase an individual health cover, especially when meeting your post-retirement health issues. Therefore, having individual health insurance coverage, even if your employer covers you, can be a smart decision to safeguard your health. You have the power of choosing the expert health insurance company and peace of mind knowing that you still have coverage even when you are no longer employed.

Q. Many people opt for deductibles to lower the premiums on their policies. However, this translates to higher out-of-pocket expenses during claim settlement. What is your advice in this regard?

Answer: Deductible as a tool is not just used for reducing the premiums under health insurance policies, it is an effective method to increase health insurance coverage with minimal additional premiums.

We recommend people opt for the deductible in line with their base policy sum insured. This will assist the person to increase the overall coverage at an attractive premium, in comparison to buying a full-fledged cover.

The customers who are covered through their company policies, or the ones who already have their own health insurance coverage may look at deductibles as an effective way to reduce the premiums while enhancing the overall overage. Those who buy the policies with an aim of only reducing the premium (without having a base cover), may run into the risk of spending a lot of money from their own pocket at the time of claim. While the premium savings can be a few thousand, the risk of out-of-pocket expenses may run into lakhs for those customers.

Q. Many people opt for lower health insurance coverage. They then opt for enhanced cover at added costs. Do you think this behaviour helps or do you advise people to opt for adequate health coverage at the start?

Answer: Comprehensive health insurance coverage is a necessity today. With the rise of chronic diseases, declining health and rapidly escalating healthcare costs, which continue to grow at an unsustainable rate, comprehensive individual coverage with a higher sum insured is important to take care of increasing medical expenses and protect the wealth of individuals.

Indians today suffer from various lifestyle-related health conditions such as hypertension, diabetes, and cardiovascular diseases owing to poor management of lifestyle regimes. Not to mention the pandemic situation, which created a huge dent in the savings of the people.

Therefore, it’s imperative to look at upgrading your health coverage from time to time. There are multiple ways in which you can upgrade your healthcare plan. From merely increasing the cover of the existing policy to adding a new one to your portfolio, there are various ways that one can consider. However, the best option has to be opting for a Super Top Up Health Insurance plan. While increasing the insurance cover or going for a new plan can cost you heavily, a Super Top Up plan offers an extra security blanket over your existing health insurance plan, which can save the day in cases of uncertainties, but at a comparatively lower cost.

Q. The Union Budget 2023 would soon be tabled. What are your expectations from the forthcoming budget session?

Answer: Access to health insurance can help more people become part of the healthcare system and get access to quality treatment. Thus, we are hopeful in the upcoming Union Budget 2023, the government looks at considering a five percent GST tax slab on health insurance premiums to make it more affordable for the people living in the middle-income group to get access to quality healthcare they need. A GST rate cut from 18 percent to five percent on the health insurance premiums will be a huge respite, especially, for senior citizens who are struggling to meet the rising healthcare costs. Currently, on most insurance products the GST is 18 percent which thrusts the premium to 118 percent for the end-user. The abolition or at least a sizeable reduction in the GST on all personal lines of products – from the existing 18 percent to five percent will encourage more people to buy health insurance.

Further, the increase in the limit of tax deduction in Section 80D can help boost the overall health insurance penetration in the country. Currently, under Section 80D, an individual can claim up to ₹25,000 deduction for self and family. This limit should be increased substantially. It is a fact that one major illness in the family can drain entire savings, and can push the family into a debt trap. Thus, in today's world of growing medical inflation, lifestyle diseases, and non-communicable diseases, having a high-sum insured health insurance policy has become a necessity. Therefore, in the budget ahead, we expect the government to announce initiatives to increase the limit for health coverage under Section 80D and GST rate cut, to help millions of people access quality healthcare at an affordable cost.