Paytm Money recently started the process to move its direct mutual fund transactions to an exchange platform at the backend. They will now use their broking code instead of RIA (registered investment advisor) code to process direct mutual fund transactions.

Paytm Money integrates its direct mutual fund platform with BSE StAR

TL;DR.

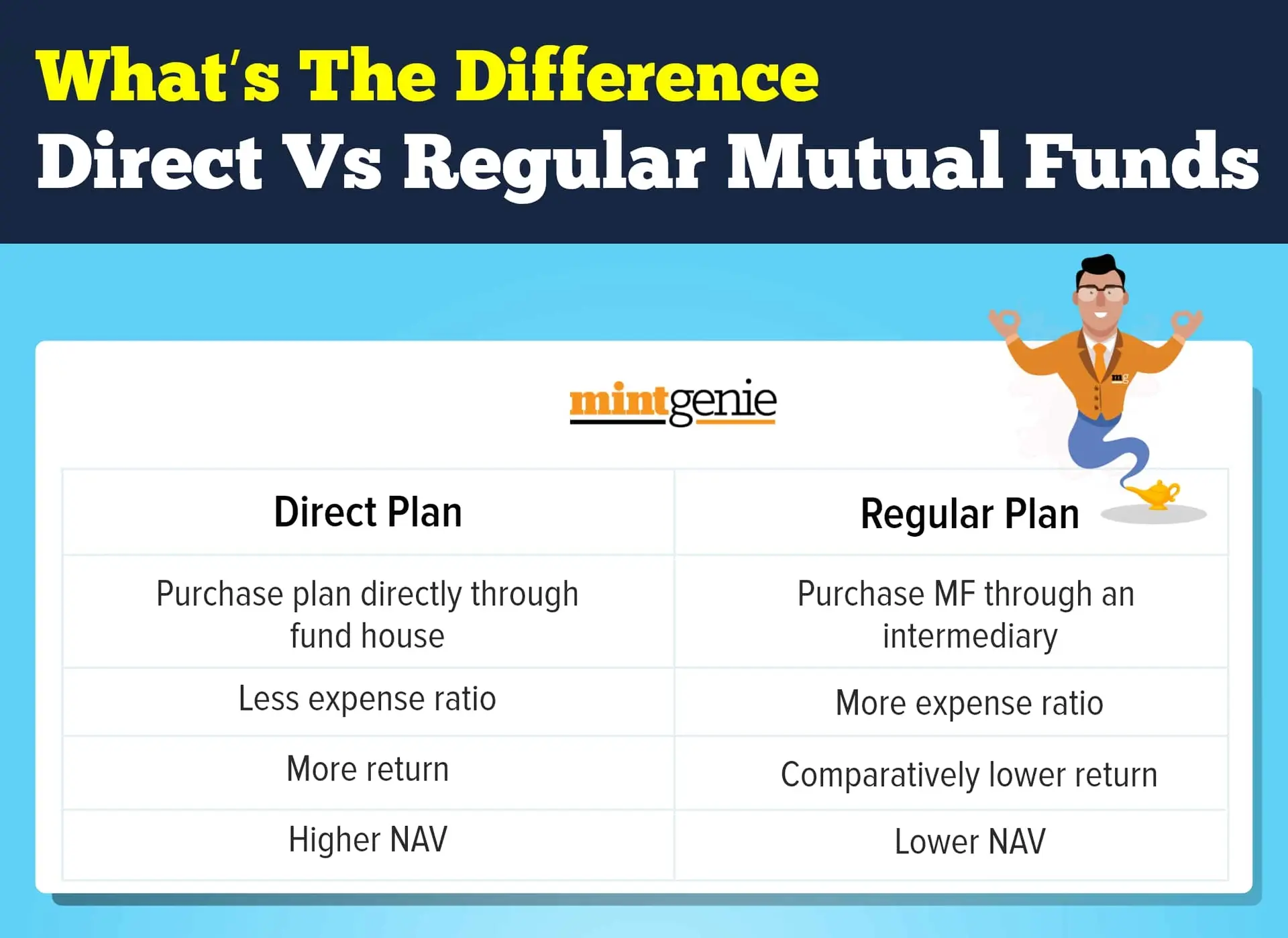

A direct plan is the one where you buy a mutual fund scheme directly from the fund house, whereas in a regular plan, you buy the same fund units through an intermediary

Platform has enabled a process for investors to complete the formalities and continue their investments.

The investors need to comply with additional Know Your Customer (KYC) norms by July 25.

This brings to focus the impact on the retail investors who, at times, get lured to join a direct platform to earn higher returns and lower expense ratio instead of choosing a broker and forego a proportion of returns.

First of all, we try to explain the key difference between direct and regular mutual fund investment options:

Direct plan Vs regular plan

A direct plan is the one where you buy a mutual fund scheme directly from the fund house, whereas in a regular plan, you buy the same fund units through an intermediary such as banks, brokers, financial institutions. For example, when you buy Tata Large Cap Fund units directly from Tata Mutual fund, it will be called direct investing.

Alternatively, if you buy the units from a broker such as Motilal Oswal, or a bank -- it will be a regular plan.

A famous online organic veggies platform promotes its products as 'straight from the farm'. Although the vegetables will be the same, but the absence of middlemen is likely to cut down the cost for buyers.

The same rule applies in direct mutual funds too.

Since there are no intermediaries, investors do not have to pay any commission or distribution fee, thus bringing the expense ratio down. Consequently, the net asset value (NAV) as well as rate of return will be different for the two categories.

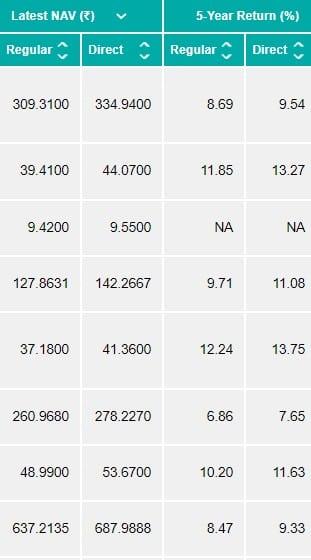

AMFI data as on July 5 for large cap mutual funds

And as one would expect, the returns for the investors of direct mutual fund would be comparatively higher vis-a-vis regular mutual funds. This difference can be anywhere between 1-1.25 percent per annum, as one can see the chart above.

Direct plan for DIY investors

The main difference between direct and regular investing is that in the former you make your investing decisions, exercise your caution, comprise your portfolio by analysing the past returns and financial statements, and finally choose a mutual fund based on what you think will perform and what you think will not.

“To be able to invest on their own, it is vital to know the nuances of investment. Some people come to me and say that if one category of mutual funds gave 80 percent return in one year then next year, even 40 percent is enough, not knowing even the fundamentals of investing – the overheated nature of markets, global scenarios that impact them, macro factors, so on and so forth,” said Amol Joshi, Founder of PlanRupee Investment Services.

"Investors should go direct if they are a DIY investor and can do their own research, do re-balancing, don't chase returns, maintain asset allocation, and execute own transactions. But direct platforms with advert that throws a random 'save 1 percent on your mutual fund' number is not the solution," says Amol Joshi.

While underscoring the similar sentiments, Abhishek Dev, Co-Founder and CEO, Epsilon Money, says: “Direct Plans of Mutual Funds are suitable for investors who are well versed with intricacies of investments, are able to plan, transact and track their investments without the need for any distributor’s guidance or assistance.”

Seek assistance if you must

Wealth advisors say there is no harm in seeking an expert’s advice if you do not understand investments.

“Let’s suppose you want to get your fan repaired, either you know how to do it or you call an electrician. In a similar vein, if you are not well acquainted about investments, you can go for regular mutual fund,” said Mr Joshi.

Abhishek Dey from Epsilon money also says that it is better to get assistance of a qualified distributor if you are unsure of the suitability of investment products as well as of your investment goals.

“If an investor is not sure of their risk profile, investment goals, asset allocation and product suitability then perhaps it is best to get assistance of a qualified distributor who can guide you on suitability and help with transactions and post transaction servicing and monitoring. So, one needs to ask whether the difference in fee is more important than the value of such guidance and service support,” Dev adds.

Direct investing platforms

Some wealth advisors wonder as to why – between two broad options of direct & regular —these ‘direct’ investing platforms even exist in the first place. These platforms work like aggregators.

But it is vital to mention that the investors interested in the direct investing can straight away log into AMC website and start investing instead of going via these ‘aggregators’.

Now since these platforms offer ‘direct’ services, one tends to get suspicious of their revenue model.

While shedding light on this, Amol Joshi says “The platform will obviously sell the product that earns them more commission. After all, they have to make up for direct mutual fund sunk cost. In other words, all users of direct mf portals and platforms become ready to listen to same old insurance sales pitch. Sooner or later, it is going to happen: same pitch you ran away from in last decade because you already know that insurance is not an investment.”

However, the ones who go via these unified platforms do so perhaps because they don't want to maintain six to eight account details in as many AMCs.

Multiple options for investors

As a matter of fact, there are multiple options for the investors who are unsure as to what to choose: direct or regular mutual funds.

The first option that they have is that they can choose a financial institution broker if you are heavily invested into too many mutual funds.

Key differences between direct and regular mutual fund plans

Second option is to approach the AMCs directly if you are invested into two or three or maximum four fund houses.

Third option, say wealth advisors, is to choose a neutral platform maintained by the industry such as Mutual Fund Utilities.

And finally, one can also approach a registered investment advisor (RIA) or a distributor where investors will pay a fee, but these agents will never surprise you with some changes in plan at a later stage.

But remember that even engaging an investment advisor is no guarantee of success. The fan, sometimes can’t be fixed, even if you summon an electrician.

First Published: 06 Jul 2022, 04:34 PM IST

Topics to follow

Related Stories

personal finance

Mutual Fund Investing: These flexi cap funds gave over 15 percent return in past three years

Team MintGenie

Explain Like I am 5

personal finance

What are direct mutual funds? Are they better than their regular counterparts?

Kirti Jha