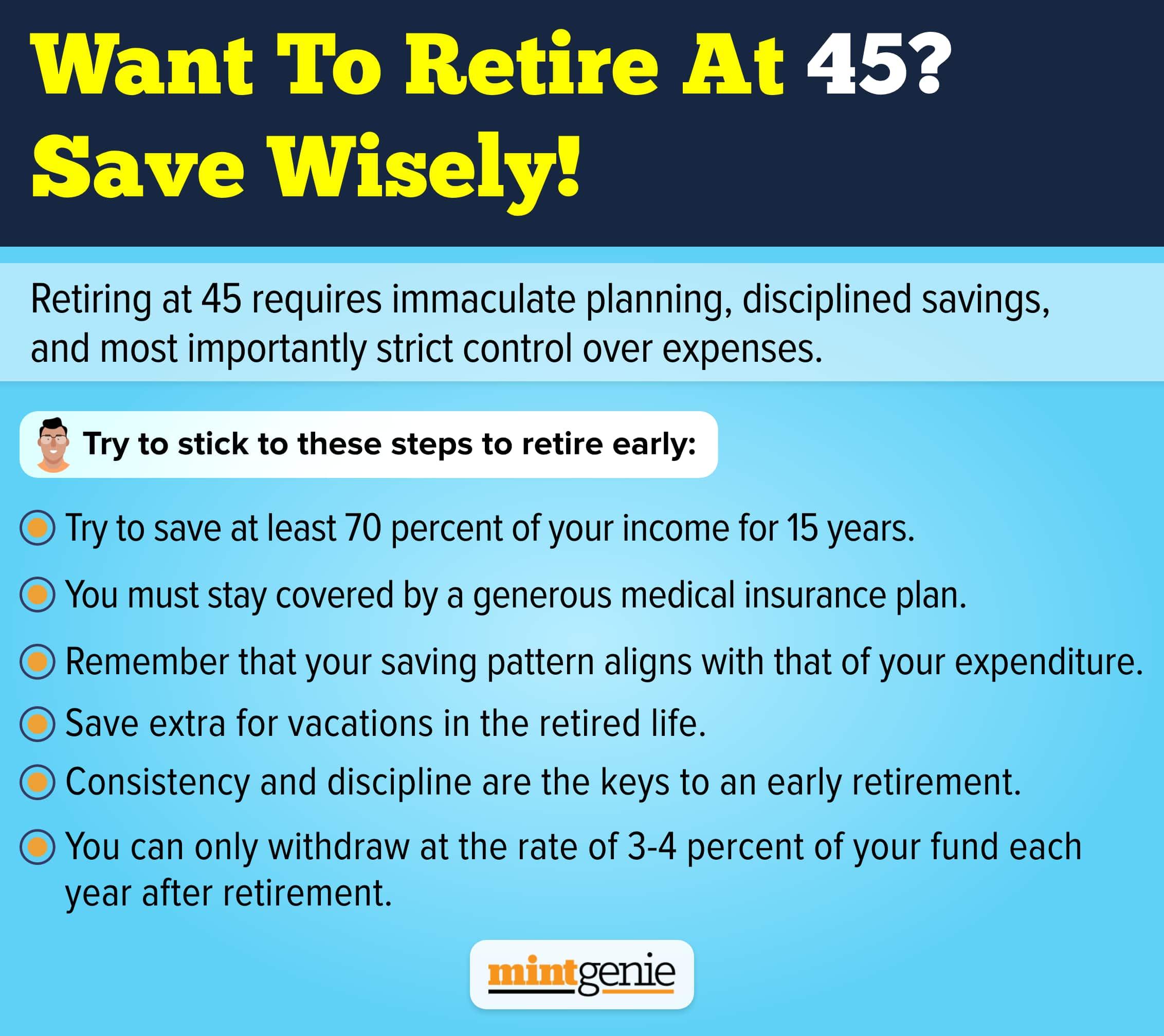

Not planning for retirement is a gross mistake. Inadequate planning for retirement is an equally grievous mistake. Saving enough for those years of your life where you would have no access to regular income coupled with the possibility of greater expenses due to old-age problems and the desire to finally pursue your dreams is a must. However, in the melee of everyday responsibilities, many people like you may tend to ignore their retirement needs, which explains the common mistakes they make while planning their retirement corpus.

Retirement planning is not an easy job. Even if you are in a job that avails you the benefit of a handsome pension as you retire, you may still want to steer away from making unwarranted mistakes while preparing for the silver years of your life.

Common mistakes during retirement planning

Most people attribute their botched-up retirement plans to their lack of knowledge and understanding of personal finance. Still, others make mistakes as they ape others’ plans without realizing how their needs may be distinct from their peers.

Relying on safe avenues alone

Agreed that sticking to fixed-income plans ensures fixed income generation for those years. But considering the interest rates that most of these plans offer, would the resulting corpus be enough to look after you, especially, when you would have no or limited income? Apart, should you focus on corpus accumulation alone when clearly rising prices clearly indicate the need to focus on the size of the corpus too? Most people focus on saving more from their earnings. Rarely do they consider the decreasing value of the rupee and the need to invest to earn returns that beat inflation in the long run. While the safety of your savings and resulting corpus is paramount, take some time out to learn about some equity investment options that you can invest in the early years of your lives. Investing at an early age avails you the benefit of compounding your money so that you earn returns not only on the principal but also on the returns earned.

The fear of falling victim to the stock markets refrains many people like you from parking money in well-performing equity mutual funds, hybrid funds with dual benefits of both debt and equity and the National Pension Scheme (NPS) that invests in market-linked instruments and allows you to withdraw some money in a lump sum and the rest through regular pensions. If at all, you are still apprehensive about investing in markets, you can resort to investing through systematic investment plans (SIPs) in diversified mutual funds and index funds.

Depending on rental income

Investing in real estate can be a great way to grow your money multifold within a few years. Some also buy properties to earn regular income through rent. While the rental income may be an excellent and continued source of ringing in constant income, a lot depends on the type of property you have bought and its location. For example, buying a property (residential or commercial) too early in life means that you must bear the costs of maintaining it later. Maintenance costs may be significantly higher than the rental yields, thus, putting you in a tight spot regarding cash in hand.

Short-sighted planning

Did you plan enough? You may have started planning well in advance, but did you plan for the later stages of your life? Did you realize how a major chunk of your savings might get wiped off on paying your hospital bills? This explains why you must also include health insurance in your investment portfolio. Unfortunately, many people realize it much later in their lives. This disrupts their entire retirement planning process as they are then left with very little money to fall back on.

This apart, you might outlive your savings. Though there is no harm in living long, you can only age happily when you have enough to pay for your living. This means that you must save an amount equal to at least 30 times your annual expenses. Don’t forget the impact of inflation, which means that the corpus you are looking to save must be enough to beat the inflation index while leaving enough for your heirs.

Mismanagement of assets

If you are careful about managing your liabilities, why not harvest the same concern for your assets? This starts with having the necessary papers in order. Make a will while there is still time so that your children are aware of the corpus that you had created. If you had bought a life insurance plan, check if all the nomination details are in order so that there is no scope of discrepancy later in life.

Planning early also involves planning well so that you do not harbour any regrets later. It is good to live in the present. However, you must also look at the present from a futuristic point of view. While apprehensions regarding a secure future may create unwarranted stress now, it will also prompt you to take care of your earnings, savings, assets and liabilities accordingly.