Tax saving is one of the key components of smart investing. Your portfolio must have good tax-saving choices along with other may be riskier assets. Equity Linked Savings Scheme (ELSS) and the Public Provident Fund (PPF) are two very suited choices for the same. However, investors may need more clarity on which one to opt for.

Let's break down both these tax-saving instruments on the basis of risks and returns to see which one is a better option:

The main difference between PPF and ELSS is that PPF is a debt scheme issued by the government while ELSS is an equity-based tool issued by asset management companies.

PPF has been a tax-saving instrument for a very long time and one of the most popular as well, however, ELSS is now catching up.

ELSS

ELSS is a type of mutual fund that is specially designed to save tax. Investing in ELSS can be used for a deduction of up to ₹1.5 lakh under section 80C of the Income-tax Act, 1961. It is more favoured with investors who have a high-risk appetite since the majority of the fund is invested in stocks and is prone to market volatility. However, in the long term, it has proven to be a good tool for wealth creation.

PPF

PPF, on the other hand, is a long-term fixed-income scheme that is backed by the government. It is one of the safest forms of investment since it has the guarantee of the government and gives assured returns. It is not linked to any market fluctuations. The interest rate is set by the government and the investor receives returns on the basis of that.

Let's now look at some salient features of these two tax-saving instruments and how they differ.

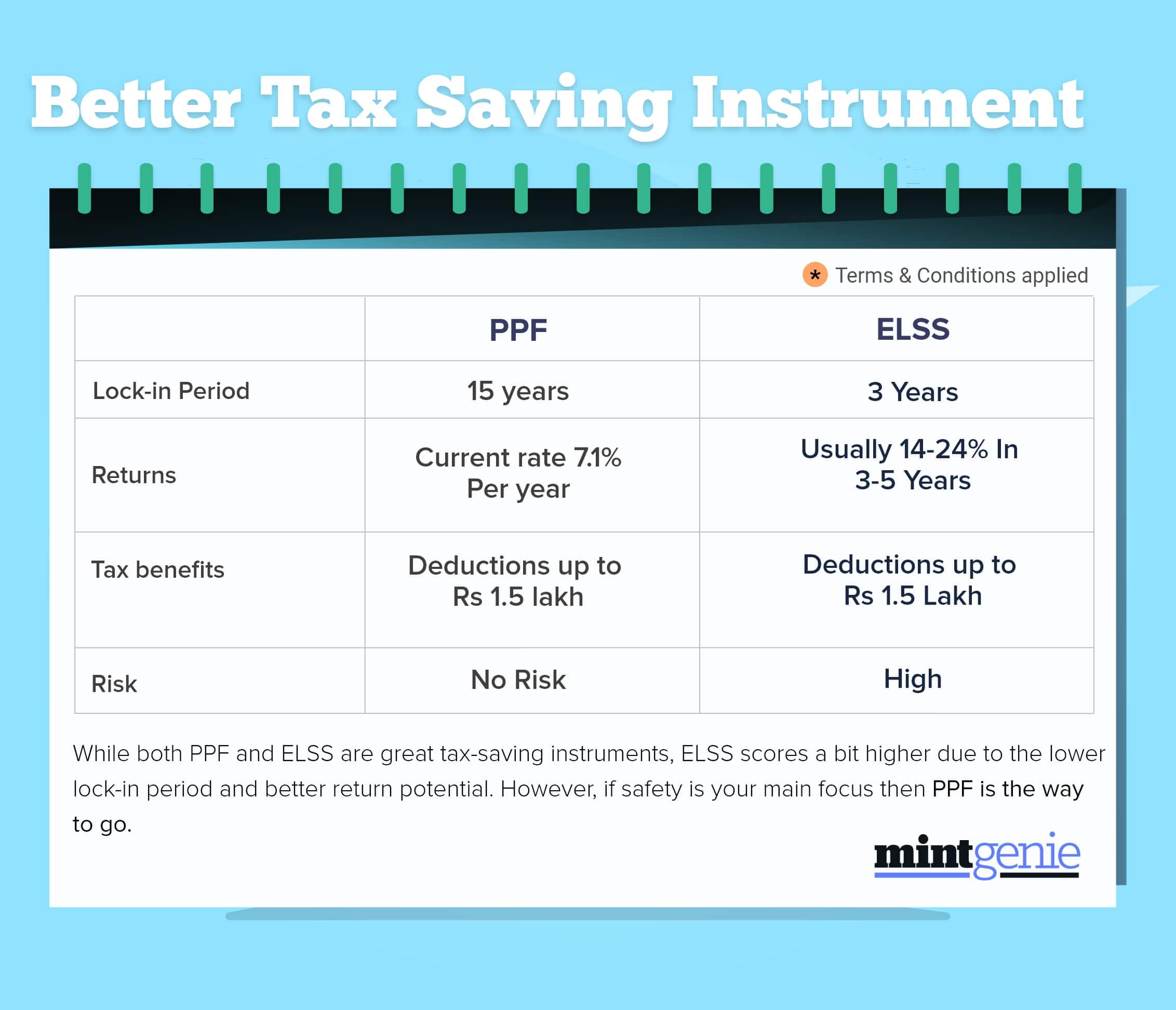

Lock-in period: ELSS offers one of the smallest lock-in periods among tax saving schemes which is three years. An individual cannot withdraw from the ELSS fund for this period. Once it is complete you can decide to continue investing or withdraw depending on your investment needs.

PPF on the other hand has a lock-in period of 15 years, which is also one of the major drawbacks of PPF. However, partial withdrawals are allowed after 7 years while after 5 years, you can close the account in case of an emergency.

Returns: Among tax-saving investments, ELSS has one of the best rates of returns. Historically, ELSS gives 14-24 percent returns over 3 and 5 years but these returns are market-linked and hence are not fixed and have significant risks. Meanwhile, in the case of PPF, the interest rate is fixed and decided by the government. It is revised on a quarterly basis and the current rate stands at 7.1 percent.

One must note that, in the last 5-years, ELSS funds have outperformed PPFs in terms of returns.

Tax benefits: Both ELSS and PPF investors are eligible for tax deductions up to ₹1.5 lakh under Section 80C of the Income Tax Act, 1961. However, ELSS returns exceeding ₹1 lakh are taxable at the long-term capital gains tax rate which is 10 percent at the time of withdrawal. The same is not applicable for PPF returns. The interest earned by a PPF is completely tax-free.

Mode of payment: For both ELSS and PPF you can invest as little as ₹500 per month. Both have the option of investing in lump sum as well as in SIP format. However, in PPF it is mandatory to make a minimum payment of ₹500 every year which is not the same for ELSS. You can stop payment whenever you like without attracting fines.

Risk: Since ELSS funds mainly invest in shares they are more vulnerable to the uncertainty of the stock market. Investors need a higher risk appetite to invest in ELSS as compared to PPF. PPF has a sovereign-backed guarantee on the principal as well as interest amount based on a fixed rate since it is backed by the government. It is one of the safest tax-saving instruments available to investors.