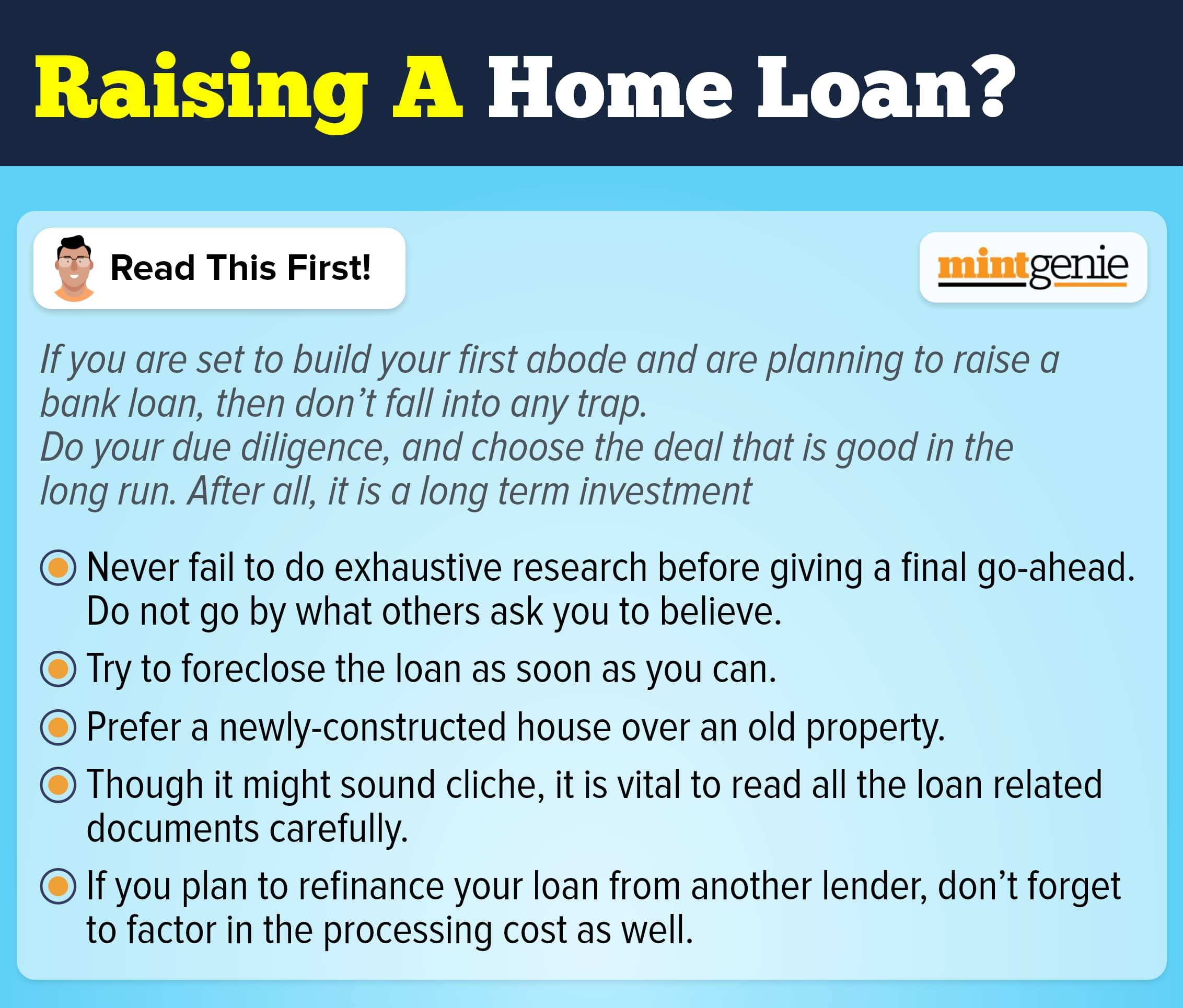

As the property rates keep on rising day by day, it has become nearly impossible to buy a house entirely from your savings. In such situations, home loans have become quite a popular and viable option. With these loans, one may comfortably pay off the mortgage amount over a period of 20 to 30 years by breaking it up into several modest payments, or EMIs.

An EMI is the set monthly payment that the borrower makes to the lender for the designated time. The principal loan amount as well as the interest on the loan, which will be spread out over a number of years until the loan repayment is fully paid off, are both included in the EMI.

EMIs are of two types- pre EMI and full EMI and it might be confusing for you to pick one while option for a home loan. We go through each of them in detail.

What is pre EMI?

The phrase "pre-EMI" refers to the borrower's payment of the interest rate that applies to the loan to the lender while the house is still being built. The majority of borrowers pick this option since lenders only issue a portion of the loan's principle, so they only have to pay the interest portion of the loan until the whole amount is disbursed.

As soon as the whole loan amount approved is fully disbursed, you can begin paying the full EMI amount. Pre-EMIs can often be paid for up to three years, during which time construction must be finished.

For instance, Mr. X took out a home loan which was disbursed in parts by the lender with first issue being Rs. 2,00,000. He only has to pay a monthly EMI of Rs. 1666 in pre EMI (calculated as Rs. 2,00,000 x 10% / 12) because the loan amount issued is just a portion of the total loan amount sanctioned.

Now, Mr. X must pay a pre-EMI of Rs. 16,666 (calculated as Rs. 2,000,000 x 10% / 12) if he accepts the subsequent payout of Rs. 2,000,000 after a period of 6 months. Only once he has received the whole loan amount does Mr. X's actual EMI, which includes principle and interest, start.

What is full EMI?

The phrase "full EMI" refers to the EMI payment made by borrowers as soon as the lender releases the principle loan amount. In this case, the principle amount may be paid in full or in part, but the borrower opts to pay the entire monthly EMI. If you choose full EMI option, you must pay the entire amount due rather than just the amount that has been released.

For instance, if Mr. X took out a house loan for Rs. 5,00,000 with a 10% interest rate and a 20-year repayment period, his monthly payment would be Rs. 48,251. The principal amount and the interest component are both included in this EMI sum. Mr. Kumar has chosen to have the loan amount delivered in instalments, however if he selects the full EMI option, he is still required to pay the full EMI amount.

Pre EMI vs full EMI

- Pre-EMI is used when the loan's sum is disbursed in instalments (usually done if the loan is taken for house construction). In contrast, the entire loan amount will be disbursed together in the case of the full EMI.

- In a pre-EMI arrangement, the interest rate is compounded based on the total loan amount paid to the builder. In contrast, the interest rate for a full EMI will be calculated using the principle amount of the loan.

- Monthly payments under a pre-EMI arrangement will commence during the construction phase. In the event of Full EMI, the EMI payment will begin only when the property has been constructed and occupied.

- The total number of loan periods will be longer if you choose the pre-EMI option since the loan amount that may be returned will only be the interest amount and the principle amount will stay unaffected. However, in the event of a full EMI, the repayment would include both the principle and interest payments, which would result in a significantly shorter loan term.

Examine your present and future financial circumstances carefully before selecting any EMI strategy, and make your decision in accordance with them. Pre-EMIs are an option if you don't mind paying less up front even if the overall sum will be considerably greater. If not, full EMIs will work great for you.