Although Reserve Bank of India (RBI) did not throw any surprise, big or small, by raising the repo rate to 6.5 percent on Wednesday, yet it led to a sense of anxiety and gloom among home loan borrowers.

And the reasons are quite explicit.

Soon after the latest rate hike, sixth in a row, most lenders are expected to pass the burden of cost of borrowing to their customers by raising the rate of interest on home loans — further raising the equated monthly instalments (EMIs).

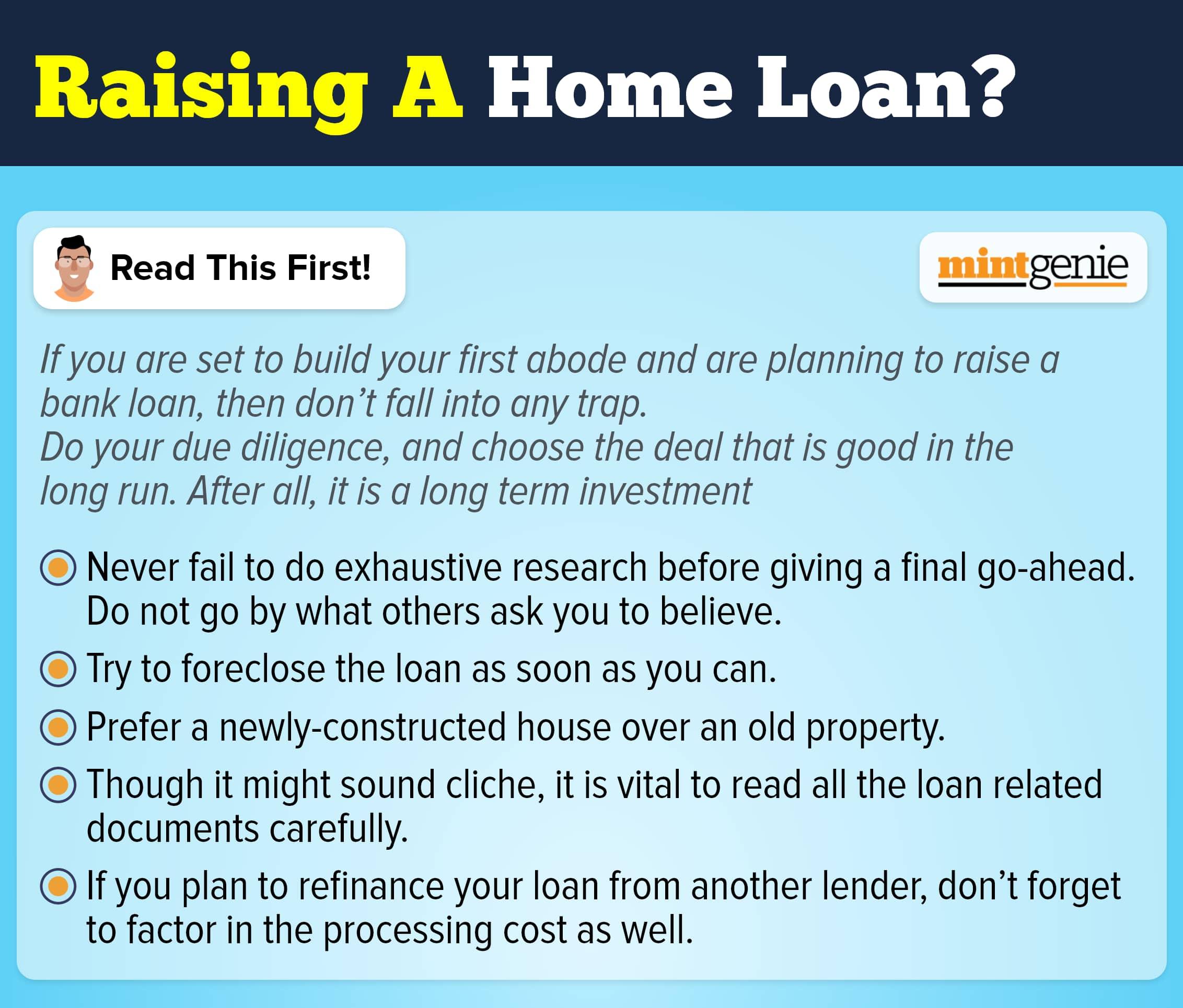

In such a scenario, what should a home loan borrower do? Although options left with them are few and far between — one of the most feasible ones is to prepay a part of the loan.

Let us understand more on this as to why it is an option worth dwelling upon!

It is axiomatic that higher repo rates ensue higher EMIs for home owners. Before RBI started the repo rate hike spree in May 2022, the lowest interest rate on home loans hovered around 6.7 percent per annum.

This means, if someone borrowed a home loan amounting to ₹40 lakh for 15 years, his monthly EMI was nearly ₹35,286. With successive rate hikes, the lowest interest rate that prevailed in the market in June 2022 was around 7.5 percent per annum. In other words, borrowers were paying a monthly EMI of ₹37,080 for the same amount of loan ( ₹40 lakh) for 15 years.

And now in February 2023, the banks and NBFCs are charging a minimum interest rate of 8.50 - 8.75 percent per annum from the borrowers.

In the table below, one can discern that a loan of ₹40 lakh taken for a period of 15 years now carries an EMI of ₹39,978, i.e., a total increase of ₹4,692 in less than a year.

| Month | Rate of interest | EMI (Rs) |

| Apr, 22 | 6.7% | 35,286 |

| June, 22 | 7.5 % | 37,080 |

| Feb, 23 | 8.75 % | 39,978 |

(When a home loan of ₹40 lakh is taken for 15 years)

Prepayment is feasible

Most wealth and investment advisors, therefore, suggest home loan borrowers to prepay their home loans as much as possible — particularly in the early part of the tenor.

Atul Monga, CEO and CO-Founder, BASIC Home Loan told MintGenie via email that it is best to prepay a part of home loan earlier in the loan tenure when the interest component is high.

Sreedharan Sundaram, Founder of Wealth Ladder Direct, also justifies prepaying the home loan because it is better than keeping money in a bank or even in a fixed deposit (FD) scheme since the debt returns are lower than the interest rate charged on home loan.

“This is the right time to prepay home loan. After all, interest rates are quite high, whereas returns on debt instruments are relatively lower. So, even if you keep surplus funds in term deposits, the net result will be negative. So, it is advisable to prepay a part of your liability as long as you have some disposable money,” says Sreedharan.

Preeti Zende, a Sebi-registered investment advisor and Founder of Apna Dhan Financial Services also concurs these views.

“A lot of home owners took loans during the pandemic when interest rate was low. But now that rates have risen substantially, it is important to prepay loan as much as possible. If you prepay the loan in the first seven years, then you can substantially save your interest outgo,” says Ms Zende.

She also says that borrowers can also use their annual bonus, quarterly incentives or even monthly extra saving to prepay your home loan. However, they should not do it at the expense of financial goals.

“Make sure you are also funding your financial goals. Make sure you are following the balance between debt repayment and investments towards financial goals” she adds.