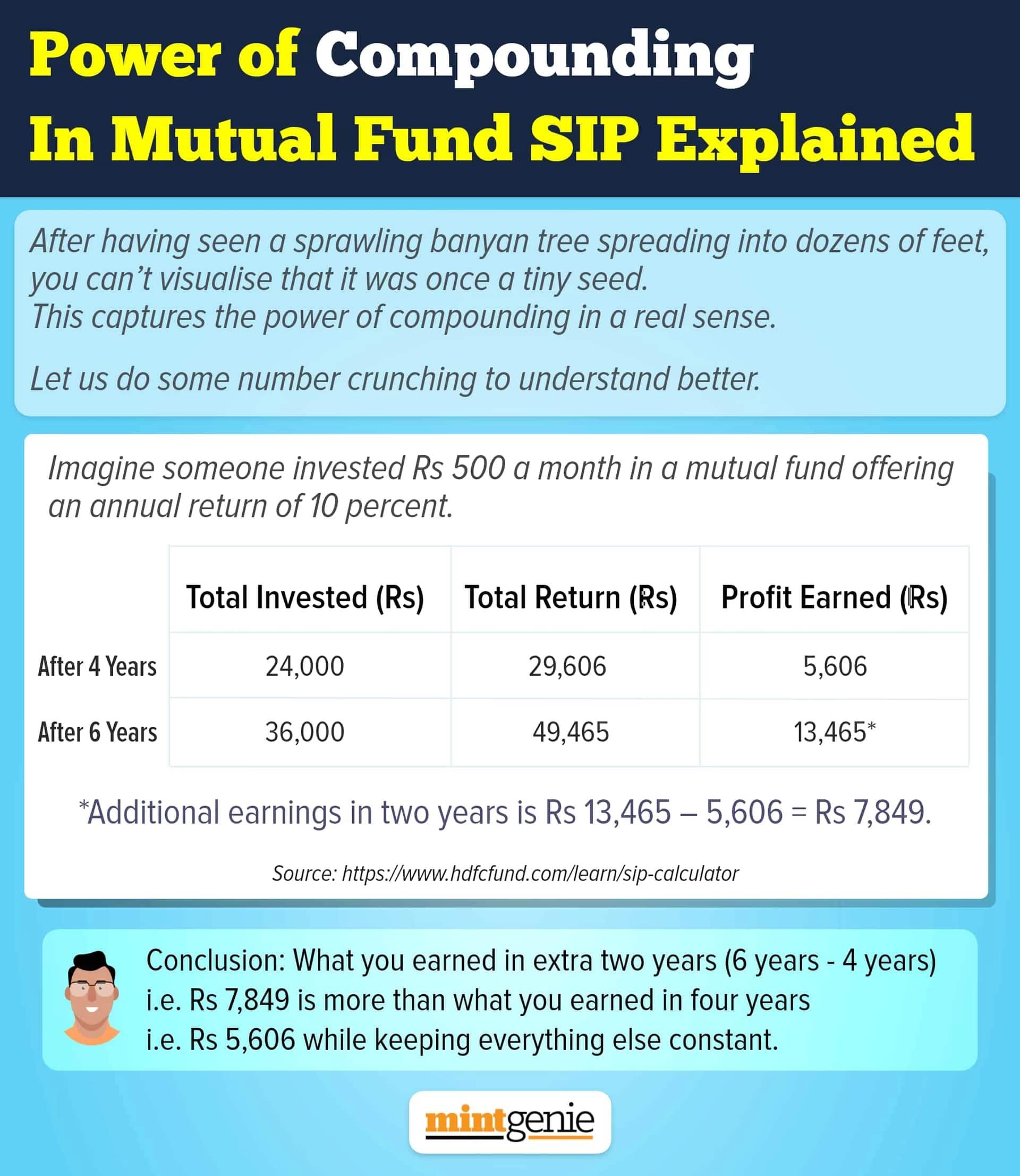

You surely would not want to mess with your financial goals, especially, if they are tied up to your post-retirement years. Hence, you must shift from equity funds to debt as you get closer to your retirement to avoid any risk of losing money.

Many investors continue to park their money in equity funds based on past returns and hope that the market-linked returns will help them create a decent corpus in the long run. However, market volatility can refrain them from reaching their goals which could include children’s marriage, starting a business in the later years, among others. To avoid suffering a dent in the amount, one must shift their money to safe havens like debt funds or fixed maturity plans or bank deposits. Extra cautious investors may start the process early.

Take, for example, you decide to invest ₹20,000 every month for 20 years for your children’s marriage. You must continue to invest the amount for 17 years in an equity fund, then redeem the corpus and reinvest the same in a debt fund for three years.

Step 1

Monthly investment: ₹20,000

Investment tenure: 17 years

Estimated rate of return: 12%

translates to

Total invested amount: ₹40,80,000

Estimated returns: ₹92,78,417

The total value of the corpus: ₹1,33,58,417

Step 2

Amount reinvested in debt fund: ₹1,33,58,417

Investment tenure: 3 years

Estimated rate of return: 7%

translates to

Estimated returns: ₹30,06,218.24

The total value of the corpus: ₹1,63,64,635.24

Sceptics often point out the inherent risk factor in debt funds too. Some question the effectiveness of debt mutual funds given the recent string of downgrades, defaults, and payment delays in this space. Though exceptions are always there, one cannot suggest these funds are futile investment options unless there is a major change that has impact on your investment portfolio. The ultra-conservative may opt for liquid funds too. Savings accounts and deposits including fixed or recurring deposits are also good options that one may put their money in while also benefiting from the ongoing interest rate.

Investors may also redeem their lump sum investments via a systematic transfer plan (STP). However, a lot depends on the market trend, market volatility, how close the goal is, whether the goal is negotiable, etc. The STP way is one way to seek redemption from a scheme though investors will be subject to taxation at the time of redemption.