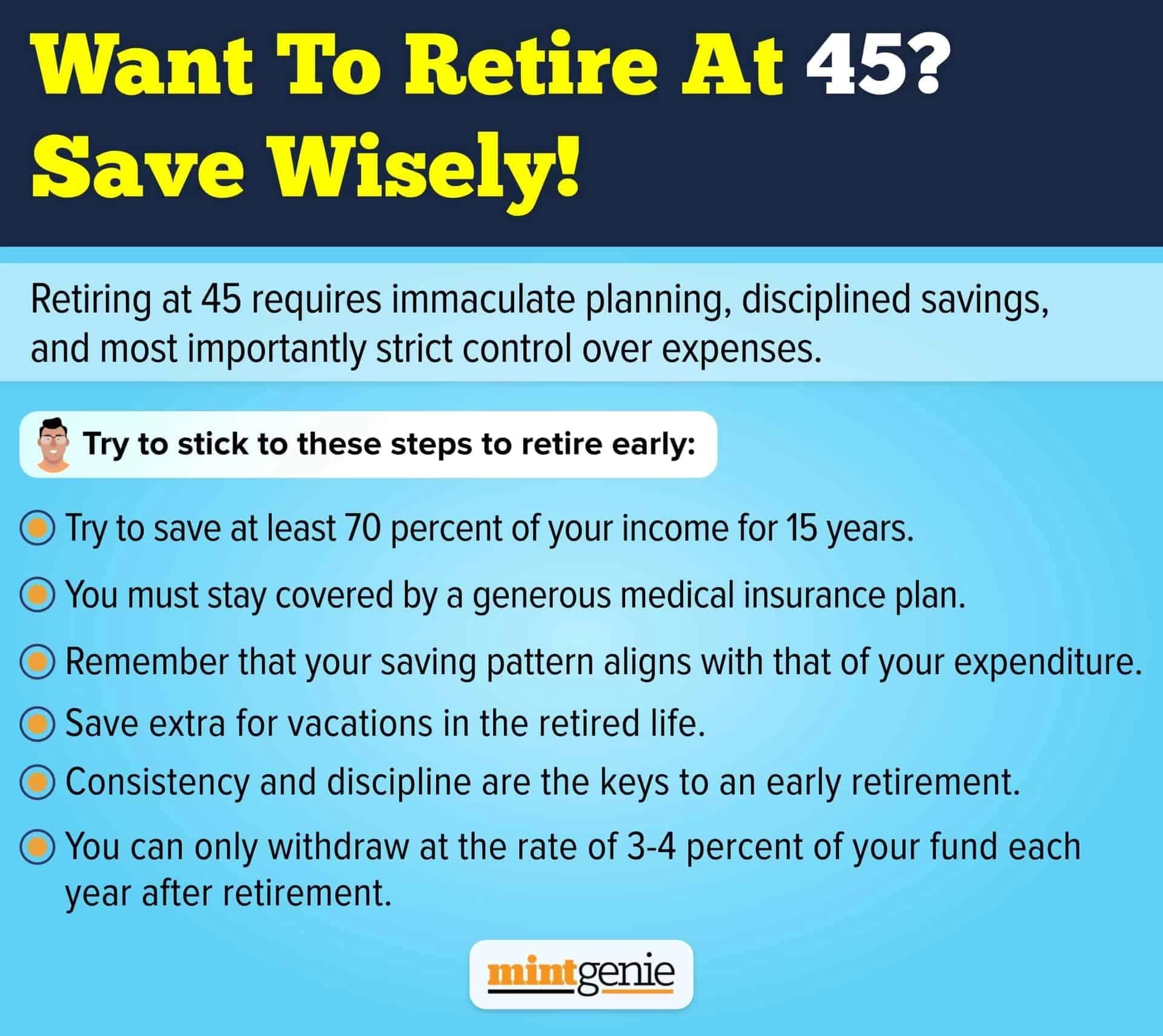

We all have heard our parents and grandparents talk about investing and saving money for retirement. But mostly, senior folks rely on fixed deposit products in the face of dropping interest rates because they provide safety while seeking for better risk-free investing possibilities.

Now, there are two major government schemes that are specifically designed to provide old age benefits and can be used for retirement planning- Senior Citizen Saving Scheme and Pradhan Mantri Vaya Vandana Yojana. However, both the schemes aim at a similar objective, there are some significant differences between the two one must understand before choosing.

Let's briefly grasp each before moving on to explore how the two are different.

Senior Citizen Saving Scheme(SCSS)

Senior Citizen Saving Scheme is a savings option promoted by the government with the primary purpose of ensuring the country's elderly people' financial stability. Even after retirement, Indian citizens 60 years of age and older can get a regular income under the Senior Citizen Savings Scheme. Deposits made under the plan are invested for a period of five years, with the option of a single three-year extension.

Pradhan Mantri Vaya Vandana Yojana(PMVVY)

The Pradhan Mantri Vaya Vandana Yojana is a non-participating, non-linked pension system introduced by the Government of India. The updated plan includes increased pension rates and a three-year extension of the policy's selling term, starting with the fiscal year 2020–21 and ending on March 31, 2023.

The Pradhan Mantri Vaya Vandana Yojana provides a loan, with the interest paid from the plan's pension fund. Based on choices that the IRDAI has authorized, the relevant rate of interest should be determined.

SCSS vs PMVVY

- For all plans acquired up until March 31st, 2022, the PMVVY's guaranteed rate of pension shall be paid for the whole ten-year insurance period. After the first three policy years have passed, the borrowing facility is also accessible. In contrast, the SCSS has a 5-year investment term with a 3-year extension option.

- Investors in the SCSS plan get regular payments in the form of quarterly pensions. However, investors in the PMVVY scheme might earn income on a monthly, quarterly, semi-annual, or annual basis.

- PMVVY provides a 7.4% yearly return. The interest rate may change quarterly in SCSS, though. Moreover, SCSS provides a 7.4% interest rate for the current quarter. Therefore, these plans offer greater yields than fixed deposits held in banks.

- Withdrawing funds from the PMVVY program prior to its 10-year maturity is challenging. Investors may, however, incur a penalty and withdraw money from the SCSS plan prior to the five-year maturity period.

- Under Section 80C, contributions to the SCSS program are tax deductible up to ₹1.5 lakh. The PMVVY program does not offer any tax advantages for investment. Additionally, neither plan is immune from taxes on income received after maturity.

While Pradhan Mantri Vaya Vandana Yojana (PMVVY) might be taken into consideration if the goal is to seek a monthly income, investment experts believe Senior Citizen Saving Scheme (SCSS) are effective at giving certain investment return.

Both SCSS and PMVVY have advantages and disadvantages. While they have some key differences, both systems work toward the same financial goal. You must first comprehend these contrasts and parallels before you can analyze.