Fixed deposits (FDs) have been one of the most popular forms of investment especially for investors with a low-risk appetite. They are fixed-tenure investments that offer the benefit of assured returns.

There are two types of FDs. The first type is offered by banks and the second is corporate FDs. These are money-raising tools for such companies and they follow the same principle as bank FDs, fixed rate for a fixed tenure. These are fixed deposits offered by non-banking financial institutions like Bajaj Finance, HDFC, etc mainly to raise money.

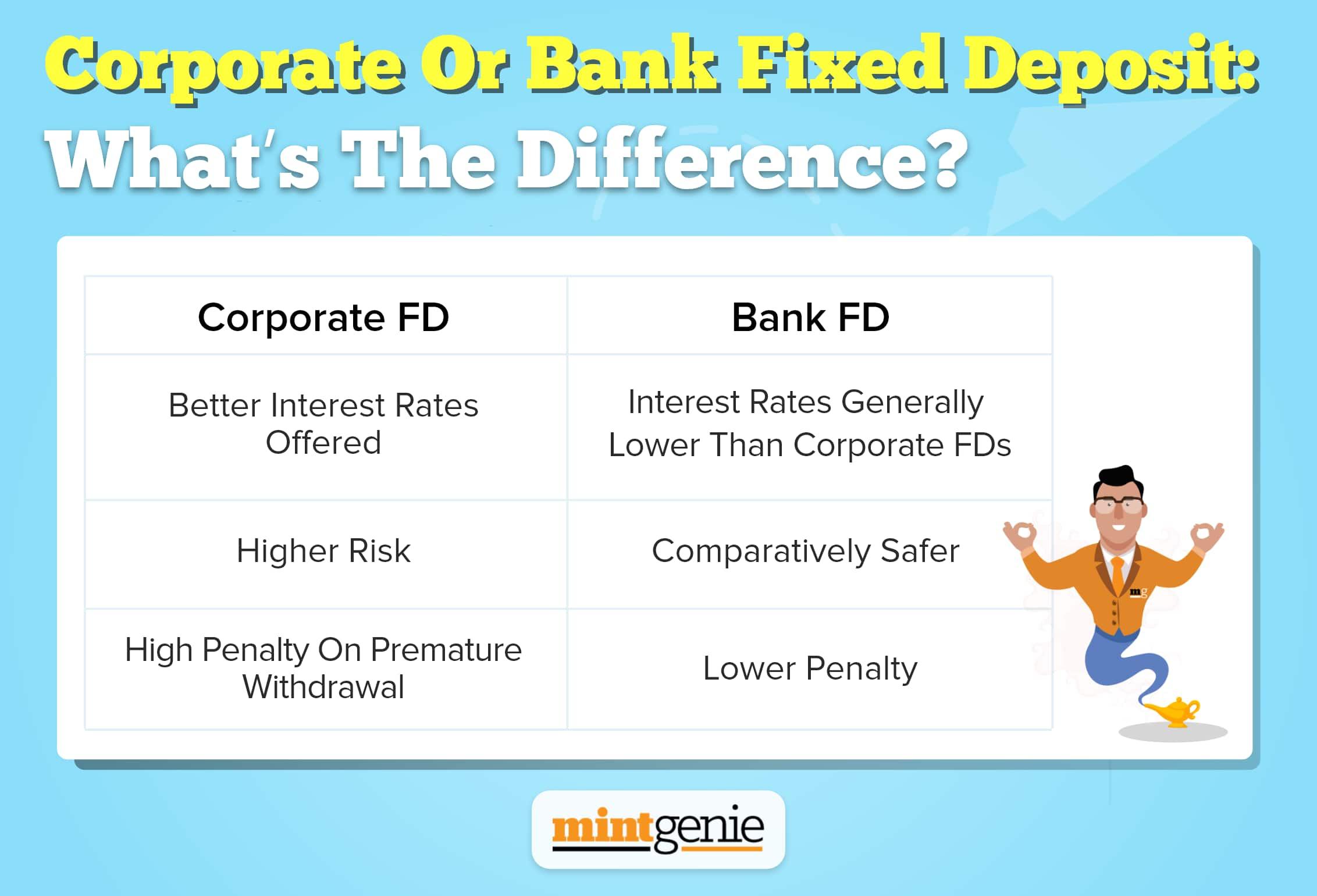

The maturities FDs vary for different companies. But corporate FDs offer better returns than bank FDs, however, the risks are also more. Generally, the minimum deposit tenure is 1 year for such FDs.

Types

There are two types of corporate FDs - cumulative and non-cumulative. In the cumulative option, the interest is paid directly on maturity while in the non-cumulative option, the interest is paid at regular intervals like quarterly or semi-annually or annually.

In the cumulative option, interest is payable on maturity & in the non-cumulative option, interest is paid on a periodical basis.

Things to look out for while choosing corporate FDs

1) The first thing to keep in mind is the credit rating of the NBFc offering the FD. One must offer for firms with higher credit ratings like AAA. A high credit rating implies a lower underlying risk.

2) One must properly research the company's background, past performances, businesses, management before opting for opening an FD.

3) Thirdly, it is important to look at the repayment history of the NBFC. It helps understand the stability and credibility of the firm.

Risks

Generally, both bank and corporate FDs have some basic risks like a lower return than markets or mutual funds, low liquidity, interest rate risk, etc. Another thing to keep in mind is inflation. Suppose you have a 6 percent interest rate for an FD but the inflation is 4 percent. Then the real rate of return will only be 2 percent.

However, corporate FDs have some more risks than a bank FD. Let's look at them:

Capital safety: Corporate FDs, unlike bank FDs, do not provide any guarantee of capital safety. AAA-rated corporate FDs may be safer than the ones with a lower credit rating but the risks are higher than bank FDs. In case of financial distress in the firm or bankruptcy, the investor can lose his/her entire money. There is no guarantee on capital protection as well as interest.

Unattractive post-tax returns: Interest on corporate FDs is taxable for investors and is taxed as per the investor's income tax slab.

Premature withdrawal attracts penalty: Generally, corporate FDs have a definitive lock-in period of three months in all tenures. An investor cannot withdraw his/her money for the first three months. However, corporate FDs levy a huge penalty on investors who withdraw money before maturity. It is more than what is levied on by banks. Also, there is no option of partial withdrawal as well.

While corporate FDs offer a higher rate of return than bank FDs, it is important to choose a company with a higher credit rating and a strong financial position to ensure the safety of the investment.