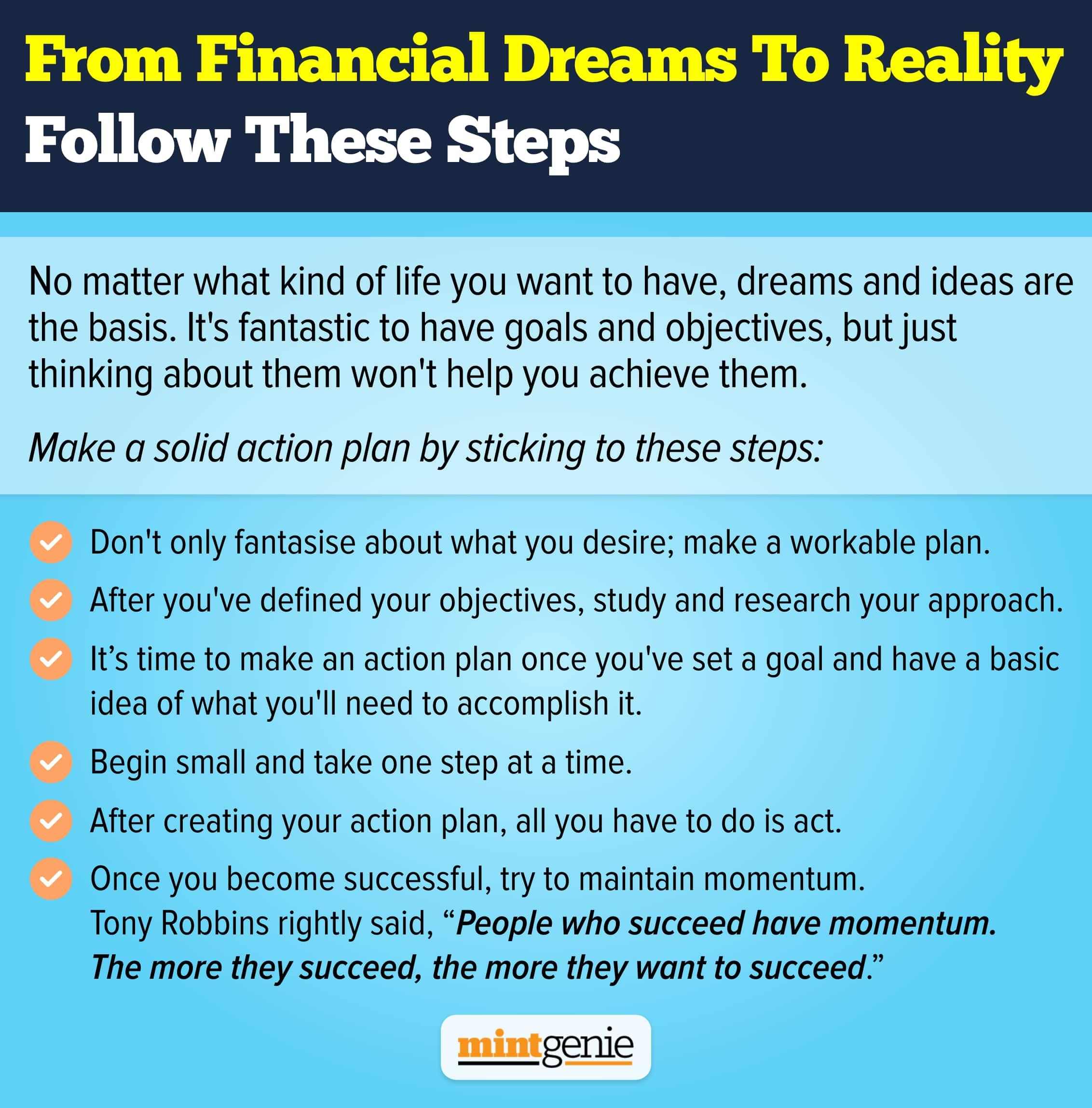

Talk to any financial advisor and they will tell you the key to building sustainable long-term wealth is diversifying your portfolio.

What diversification does, simply, is makes sure some part of your money keeps growing at all times. For example, if the stock market is faltering, then gold is likely to do better. If exports are expensive and your IT stocks are underperforming then maybe your FMCG stocks may come to the rescue.

The idea, as you may have guessed by now, is simple. Diversification is the go-to strategy.

Today, let's test a theory. What if you do not diversify and put all your eggs in one basket (cliche alert!).

Set your goals first

If you are in here for a “quick rich scheme”, putting money in equity funds with a short-term investment goal will only backfire. The reason is the constantly moving and oscillating state of the market. It may be flat one day, be up for some days and also slope down for many days. More than the intrinsic value of the shares and how the companies perform, there are other factors that can not only affect the market but shake it to the core. For example, the investors basking in the profits from the 2021 rally are in a state of shock as the market keeps plunging to new lows. For investors propose, but the market disposes; neither is the way of the market in your own hands. Timing the market is impossible and futile. It is the time spent in the market that will spell the extent of your returns.

Setting a goal is essential to asset allocation. If you have a short investment horizon, parking money in equities is not worth the risk. Ensure that you do not set a major part of the corpus in equity instruments then.

Staying invested

There is a gulf of difference between investing and staying invested. If you are planning to stay invested for the next 15-20 years of your life, it would do a lot of good to park a major part of your earnings in equity fund investments. The stock allocation rule says that you must deduct your current age from 100 to derive the percentage of your equity fund investments. For example, if you are 30 years old, you may invest 100-30 = 70 per cent of your earnings while the remaining money can be parked in debt funds or fixed income instruments earning moderate returns.

Many young investors willing to take risks invest their entire capital in equity instruments. While this may not be an entirely bad option, taking this kind of risk makes sense if they are willing to continue their investments for at least 20-30 years. However, you must have the necessary risk tolerance and keenness to get to grips with volatility in the long run. This is because all looks hunky-dory when the market is roaring and raging at new highs. The real test of your patience and grit comes only when the market is reeling under unforeseen and prolonged corrections.

A little bit of money set aside for short-term debt funds will do you much good as it will provide you with the much-needed liquidity as and when required. You may also park a small sum of money in fixed-income category instruments like bank deposits or bulk term deposits that you may redeem immediately when necessary.

Running full steam

Going full-throttle on equity has both benefits and downsides depending on how you look at the market and your investments. While in the initial years of your life, you may invest your entire earnings in equities after having paid for health insurance, life insurance and setting aside an emergency fund. However, this equation must change as you hit middle age to infuse some stability in your investments.

For example,

For the first 10-12 years, invest 100 per cent in equity

For the next 10 years, invest only 80 per cent in equity

For the next 12-15 years, invest only 60 per cent in equity

For the remaining number of years, invest not more than 20-30 per cent in equity.

Just start reducing your equity allocation and set aside some money for debt funds in your investment portfolio. The moderate returns will cushion you against sudden market falls, though, in the long run, the power of compounding in your equities will help you meet your financial goals.