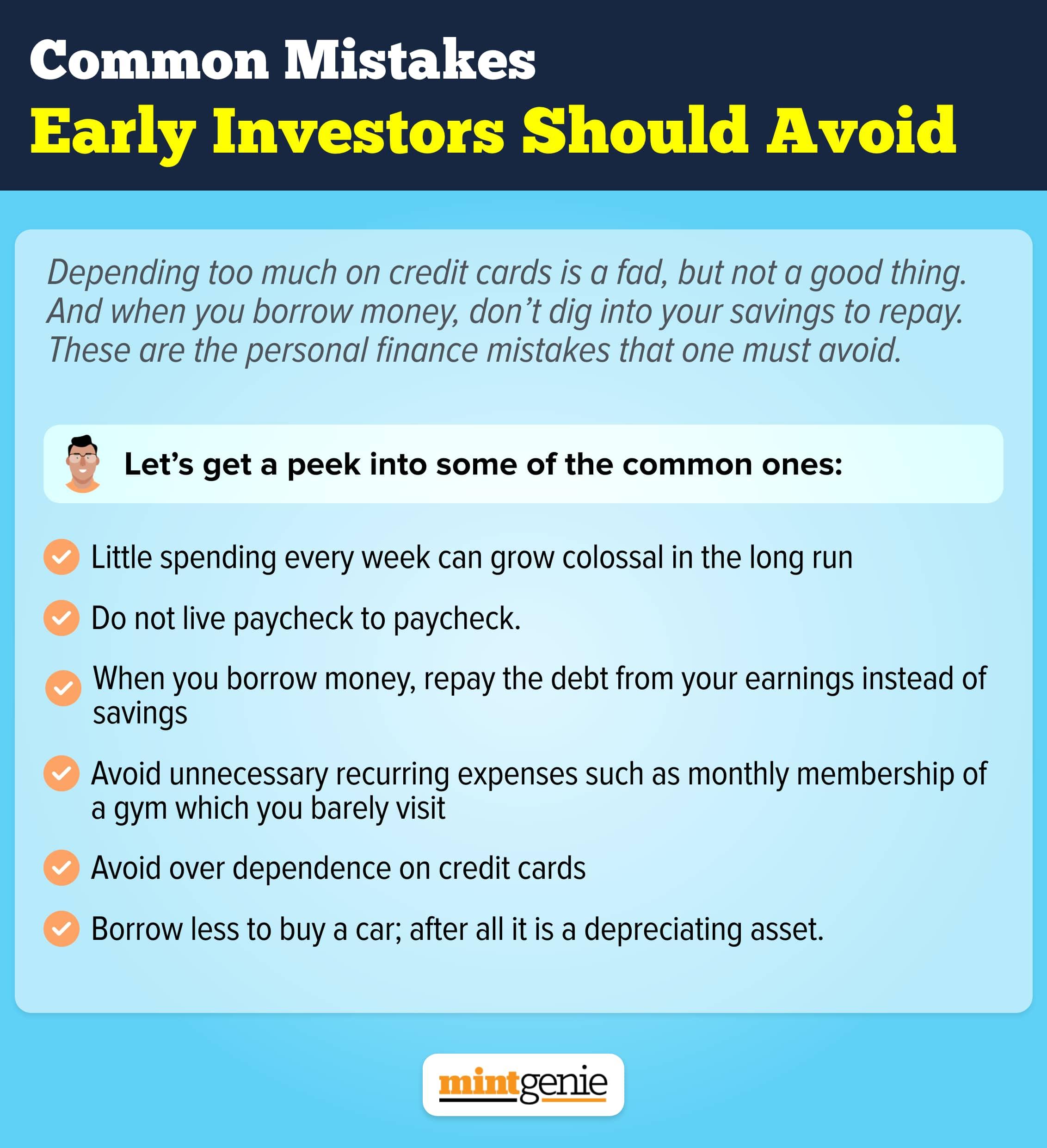

What will you do when the market is expected to rise after it bottomed out, and a further market correction may not be on a horizon — at least not in the near future? In such a scenario, instead of investing via SIPs (systematic investment plan), one could invest lumpsum to make the most of correction.

Short term market corrections

There is no denying the fact that SIPs enable investors to make the most of rupee cost averaging. Buying funds at different price points lead to averaging out of buying price, thus increasing the chances of profit-booking.

Since timing the market is not possible, the tried-and-tested technique of SIP spares investors from buying during the bull market and selling during the correction.

However, there could be some occasions when the market correction is steep, and is expected to stay like that only for a short while. During such times, one can invest via lumpsum over and above of regular SIPs.

“When the market is down by 10 to 15 percent, it is ideal to invest in lumpsum but when there is a correction of anywhere between 4 to 5 percent, you can make your investment in advance,” says Sreeedharan Sundaram, a SEBI-registered investment advisor and founder of Wealth Ladder Direct.

However, the other alternative would be to go via systematic transfer plan (STPs), advises Mr Sreedharan.

“If you have some spare money, then one can invest in liquid funds or money market funds and transfer that money systematically from liquid funds to equity funds,” he adds.

Ravi Saraogi, Co-founder of Samasthiti Advisors, also shares a similar advice when he says, “If somebody feels the market has bottomed out, then one can invest the lumpsum but via STPs (systematic transfer plans) over a period of 6 months because it is not possible to time the market correctly. Let us say, someone has ₹5 lakh spare, one can invest in the five or six instalments.”

Debt Vs equity

Usually the age-old doctrine of rupee-cost averaging is given in reference to equity investment because points of entry and exit of investment determine the quantum of returns.

On the contrary, the same benefits are not accrued in debt funds because they are not as volatile as their equity counterparts. Although long term debt funds are volatile, the same is not true for most liquid and short-term debt funds.

“If it is a debt fund investment, then investing in one shot is absolutely fine,” says Mr Saraogi.

Factors to consider before choosing lumpsum

One of the factors that should be weighed is the proportion of total investment that is being invested. For instance, if you want to invest ₹50,000 and your total portfolio amounts to ₹10 lakh then it is just 5 percent of your overall investment, then any volatility that follows immediately after your lumpsum investment will not have a significant impact on your total profit or loss.

On the other hand, if you have an investible corpus of ₹one lakh and your total investment portfolio amounts to ₹5 lakh then instead of investing via lumpsum, one should ideally invest via STPs.

To sum up, we can reiterate that investing via SIP is a time-tested technique to curb the investment risk, but there are a few occasions when investing via lump sum is advisable e.g., when the market witnesses a steep fall, say up to 15 percent.

Alternatively, when you have a large sum to invest over and above your regular investment, then you can park that money in liquid funds for the time being, and transfer the same to equity funds via systematic transfer plans.