Two years have gone by, and some of us are still reeling under the grief of losing our loved ones. Many are trying to rejig their lives back to normal with the death benefits received on the death of the deceased. The effect of the Covid-19 pandemic highlighted the uncertainty of life, thus, bringing forth the importance of buying life insurance. The perspective surrounding life insurance has changed with many people now including it in their investment portfolio than relegating it to the list of expenses involving regular premium payments. Still, there are many who may have missed out on their premium payments due to many reasons including inattention to the need for insurance, unemployment, etc.

Policy lapses

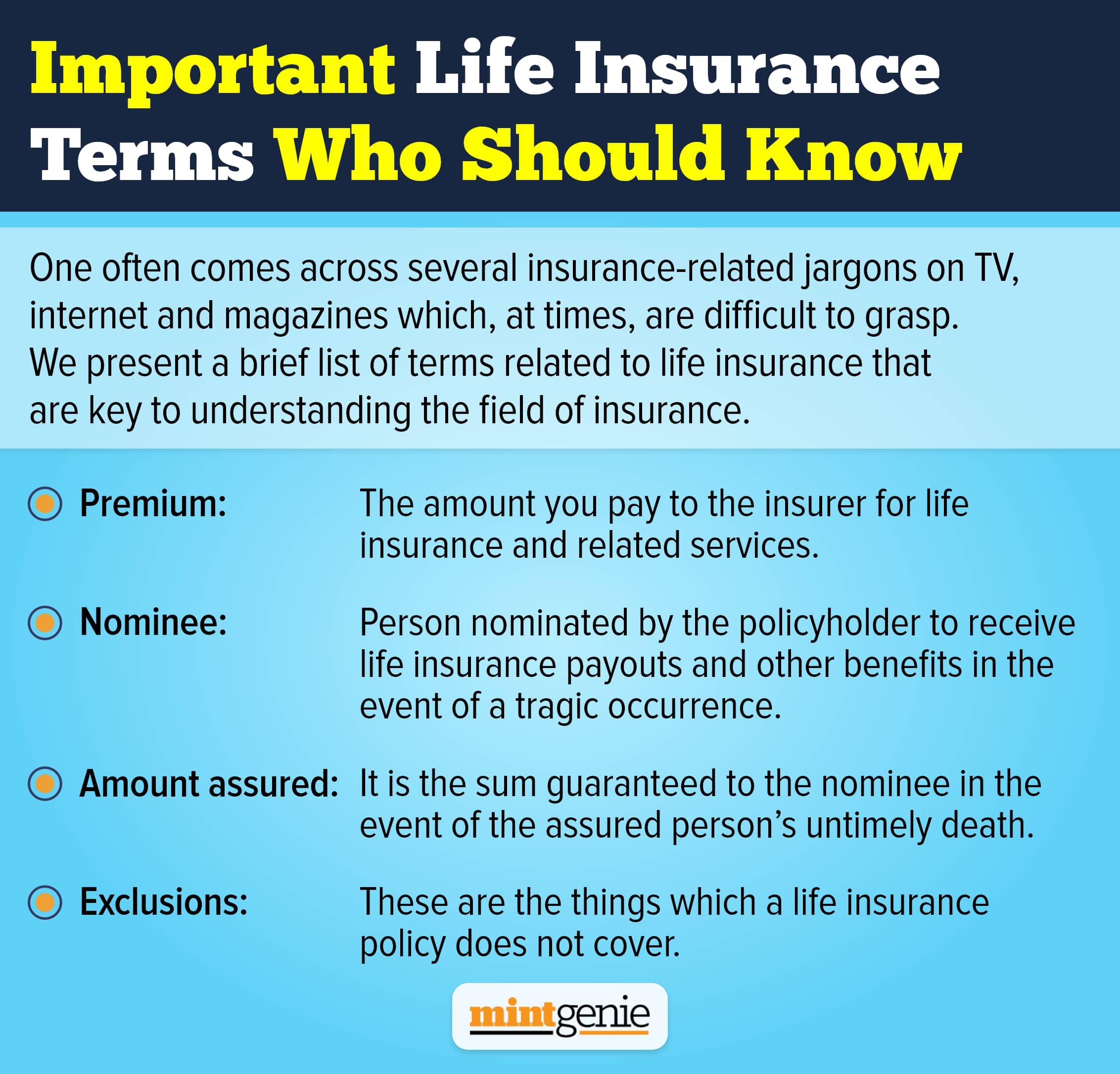

There is no second questioning the fact that life insurance is an utmost need that you cannot do without. You cannot surely think of progressing without considering the need to secure your loved ones against a possible financial crisis in your absence. Still, many people miss a premium payment or two causing the policy to lapse.

However, missing out on premium payments does not spell complete policy lapse as insurance companies allow a leeway to their customers to seek revival of their policies. Still, many are unsure of whether to seek policy revival or buy a new life insurance plan altogether.

Why revive your old policy?

Many of us take life insurance for granted not realizing how regular premium payments are necessary to continue the policy for a secure financial future. You do not buy a life insurance policy to gain from it while you live. The idea is to ensure that your nominees benefit from the policy when you are no more to bear their expenses. As long as premiums get paid on time, the policy remains active. The policyholder must ensure to pay the premiums within the due date, post which they are allowed a grace period between 15 and 30 days. It is only when you fail to premiums even during the grace period that the policy lapses.

Seeking policy revival

How much time is allowed prior to policy revival is a common question that many ask. Sajja Praveen Chowdary, Head of Term Life Insurance, Policybazaar.com says, “When you purchase a term life insurance policy, you have the option of paying the premium in monthly, quarterly, or half-yearly instalments, or in one lump sum each year. You may select any of the options based on your financial resources. When you stop paying your term life insurance premiums, the policy becomes inactive. To reactivate your term plan, the insurer gives you a grace period of 15 days if you pay the premium in monthly instalments and a grace period of 30 days if you pay the premium quarterly, half-yearly, or yearly. However, if you do not pay the renewal premium for your term insurance, the policy will lapse.

According to the insurance regulator's guidelines, the maximum revival period for term insurance policies issued prior to December 2019 is two years, while the maximum revival period for policies issued after December 2019 is 5 years, after which the policy is terminated. To resurrect a lapsed term life insurance policy, the policyholder must pay all outstanding premiums – from the date of the first unpaid premium to the revival date – as well as interest on outstanding premiums and any applicable taxes and levies. In some cases, the insurance company may even request a medical examination again if the policy is revived.”

Reviving a lapsed policy is not too difficult as you just have to pay the premiums accumulated and left unpaid over the period along with interest and taxes. Naval Goel, CEO & Founder, PolicyX.com shares, “Revival of lapsed life insurance usually requires you to pay premiums along with interest and penalty amounts that vary from insurer to insurer. However, in most cases, if the lapsed duration is not very high, insurers typically come up with revival schemes wherein they waive off the penalty amount to encourage policyholders to revive the policy.”

How much interest and penalty must be paid depends on the policy terms and conditions.

Checking policy exclusions

No life insurance policy comes without its set of exclusions. These exclusions are common in all life insurance policies, though insurance companies may vary in their list and details of exclusions. You must be aware of these exclusions, lest your ignorance causes your beneficiaries to lose out on your death benefits.

Pankaj Bansal, Chief Business Officer, BankBazaar.com says, “A reinstated policy is as good as a new one, and the insurer may impose new terms and conditions, especially on exclusions and pre-existing conditions. So it is important to check these clauses. While the revival of the lapsed policy may happen at the earlier premium, some of the benefits accrued, such as the waiting period for pre-existing illnesses, may lapse and you may have to wait out the waiting period again. Insurers often run campaigns for the revival of lapsed policies where they waive penalties on lapsed policies. However, before reviving an existing policy, do a cost analysis which not only considers the premium but also the waiting period and other factors and only then take a call on whether to renew or not.”

Though a lot depends on the terms and conditions of the insurance company, in most cases policyholders may be asked to undergo medical tests to check for pre-existing disorders prior to policy revival.

Renew or buy?

There is a constant raging debate regarding whether policyholders must seek revival of lapsed policies or opt for a new one altogether. Many policyholders face this dilemma considering that there is no one-line answer to this question and that it all depends on myriad factors.

Reviving an old life insurance policy involves some added charges apart from the premiums left unpaid. You must consider these charges before applying to get your old policy revived. Similarly, if a considerable time has elapsed since you had last paid your premium, chances are that the policy now costs more. This is especially true for policyholders who had bought life insurance when young and many years have passed since you had first paid for this policy. New premiums are most likely to be higher as life insurance plans get costly with age.

There is another facet to life insurance that we dare not ignore. Technology has made it possible for you to buy insurance online, thus, cutting down on the cost of the policies. This also means that life insurance bought from the insurer’s site or from the portal of an online insurance aggregator will not cost as much as those bought through an agent. With technology helping insurance companies to cut down their policy prices, chances are that you can buy a new life insurance policy with better and more enhanced coverage. However, for this, you must compare the plans on offer by various insurance companies and choose the one that offers the most at the least possible prices.

High prices may prompt many people to choose between old policy revival and the purchase of new policies. Similarly, a comparison of life insurance coverage amounts may cause some of them to tilt in favour of the latter.

For example, it is best to revive policies bought a long time back, say 10-15 years back since premiums of new age policies would be much more than what insurers charged a decade back. However, lapsed policies that were bought recently around a or two years back should be best revived. This is because the number of unpaid premiums would be far too less compared to what a new policy would charge. Also, in many instances, insurance companies wave off the interest and penalty charges on the policies to encourage their customers to continue with their policies. But then, do not forego the benefits that new policies would offer. This means that you must weigh policies depending on what they charge and what they offer to their customers.

Check for policy riders and cover too

New life insurance policies on the block offer benefits that were non-existent in earlier policies. The coverage amount is also more at cheaper premiums. Added riders allow you to choose from the myriad options while keeping in mind the kinds of benefits you want your nominees to have. All these and more encourage many policyholders to discard their lapsed policies in favour of a new with nominal premium charges, greater coverage and added rider benefits.

You must consider these and other factors before deciding whether to revive a lapsed policy or buy a new one.

Buying life insurance is a must considering how none of us can be sure of what the future has in store for us. The present is not so pleasant, the past is filled with grief and the future is uncertain. It is to tackle this uncertainty you must opt for a life insurance plan that will take care of the finances of your loved ones in your absence.