The dreaded days are here. The Reserve Bank of India (RBI) has hiked the policy rate three times since May. The repo rate at 5.40 per cent is now higher than the pre-pandemic level of 5.15 per cent. The repo rate is the interest rate at which banks borrow short-term funds from the RBI.

When the borrowing cost for banks goes up, it passes it on to those who borrow from the banks. That said, the historic low home loan rates that the borrowers enjoyed over the last couple of years are seeing a revision upwards. Several banks from ICICI Bank, Bank of India to Canara Bank have hiked the home loan rates.

If your bank has also hiked the rates, you must be wondering if you should keep paying higher interest rates or try to refinance from the other bank. It is to be noted that repo-linked loans are mostly the cheapest and most transparent, while MCLR, Base Rate, Prime Lending Rate-linked loans may charge a premium compared to the repo loans. So, one can refinance from the same bank itself if one is to only change the underlying benchmark rate.

Should you make the switch?

“Today, the lowest home loan rates are at a premium of around 240-250 basis points over the repo rate. You should ideally not pay more than this if you have a good credit score, stable income, and good repayment record,” says Adhil Shetty, CEO, BankBazaar.com.

Top 5 public and private banks with lowest Interest on home loans

We have compiled a table on top five public and private sector banks with the lowest interest rates:

| BANKS (Floating Rates) | Interest Rate (% pa) (on Loan >= ₹35 Lac to <= ₹75 Lac) |

| Public Banks | |

| Central Bank | 7.2 |

| Bank of India | 7.8 |

| Bank of Maharashtra | 7.8 |

| Indian Bank | 7.9 |

| Punjab National Bank | 7.9 |

| Private Banks | |

| Karnataka Bank | 7.96 |

| Kotak Mahindra Bank | 7.99 |

| IDBI Bank | 8 |

| Karur Vysya Bank | 8.05 |

| Axis Bank | 8.1 |

Note: Top 5 public and 5 private banks with lowest interest on specified home loan range are separately shown in the table in descending order. Data taken from respective bank’s website as on Aug 24, 2022. (Source: BankBazaar.com)

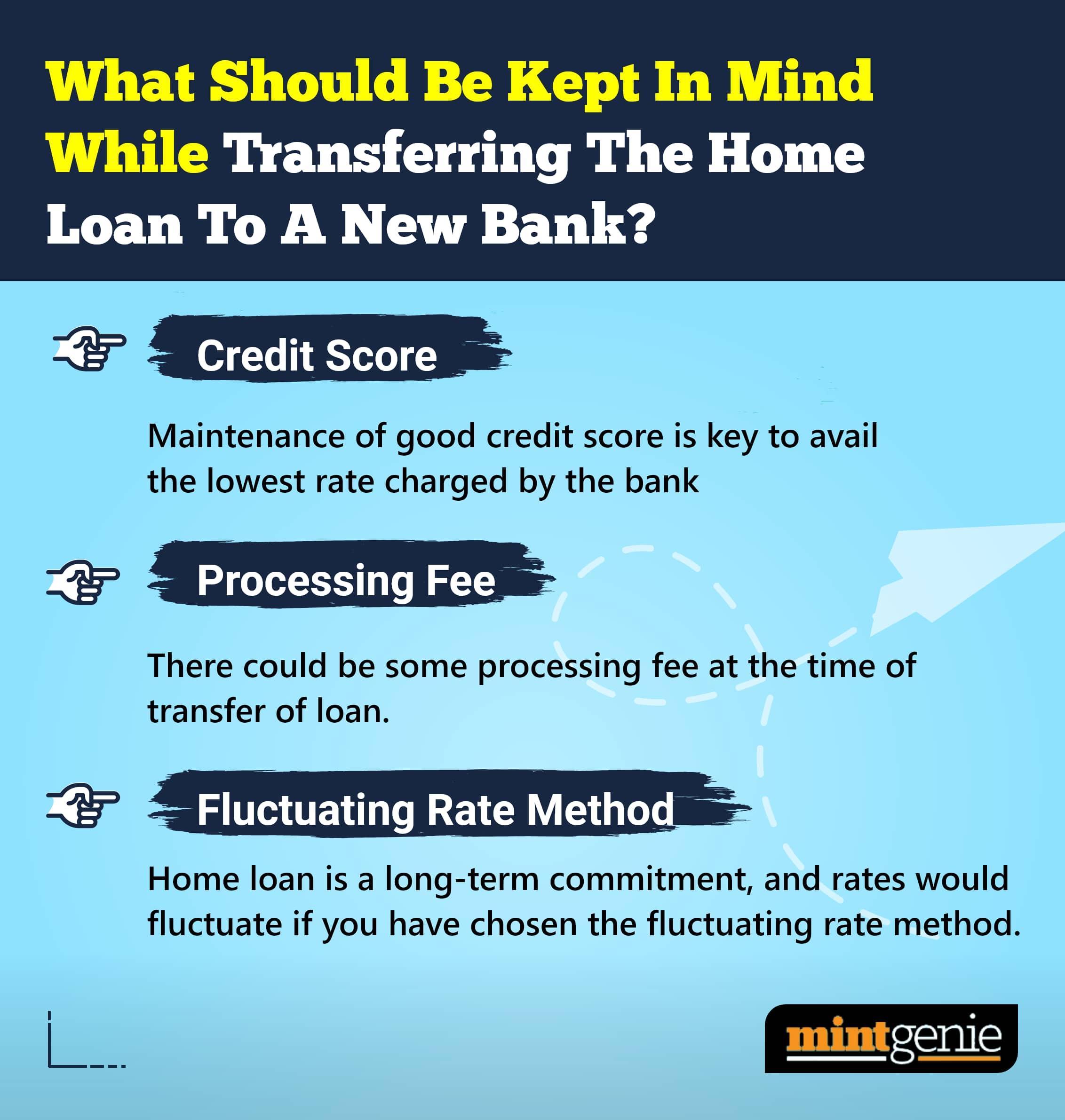

Take a thorough look

Remember lending rate alone doesn’t matter. You need to be aware of processing and other legal charges. The decision whether to switch to another bank also depends on how far ahead you are in the repayment cycle. The earlier you refinance in your tenor, the better. “Assuming no prepayment, in a 20-year loan, refinancing in the first 13 years has the highest impact. In a 25-year loan, it’s in the first 18 years. In a 30-year loan, it’s 22 years. At these points, you have around 50 per cent of your loan left. Thereafter, the impact decreases gradually,” says Shetty.

So, consider refinancing only if the outstanding loan is more than 50 per cent.

Further, cost justification is needed. A typical refinance to a new lender involves processing fees, legal and paperwork fees, and MOD charges. “The costs may be in the range of 0.2 to 0.4 per cent of the loan in most cases. You should be able to recover the costs as interest savings preferably in the first two years of the new loan,” advises Shetty.

Finally, better customer services and proximity to the lender's branch should also be considered.

Case study

Ms Sneha Pratap had taken a bank home loan of ₹50 lakh in 2016 at an interest rate of 7.65 per cent. The loan was linked to the MCLR. The market rate had come down to 6.50. With regular prepayment, Ms. Y had brought her loan down to ₹20 lakh. She had less than six years left on the loan. But the interest rate at her loan was still high. Her own bank was offering a lowest rate of 6.65 on a repo loan. Her options were to refinance with her own bank or do a balance transfer. She chose to refinance with her own lender. Here is how she decided:

| Factor | Analysis | Reason to Refinance | Justification |

| Rate | The difference of 100 bps is huge. | Strong | No reason to pay a high rate when she is eligible for a big discount. |

| Benchmark | Switching from MCLR to repo. | Strong | A good reason to refinance since repo rates are the lowest and more transparent |

| Payment Terms | No change. | Low | Since she remains with the same bank, no changes in how she pays the loan. |

| Time Left | 6 years. | Low | A weak reason to refinance since pre-payment has reduced the loan tenor considerably. |

| Loan Left | Rs. 20 lakh or 40% of the loan. | Moderate | Nearly half of the loan still needs to be repaid and a refinance can help save interest |

| Costs | Processing fee of Rs. 3000. | Strong | The costs are very low and make the refinance attractive. |

| Customer Service, Proximity | No change | Low | No changes since she is sticking to the same bank |

Source: BankBazaar

Decision: Shetty of BankBazaar says, “Sneha has little to benefit from a balance transfer since 60 percent of her loan is paid off. It is a smarter choice to refinance with her own lender. Her bank can convert her MCLR loan to a repo loan. The loan balance of 40 per cent can now be paid at a lower cost. She can recover the refinance cost almost immediately.”

A check-list based on the above factors can help in deciding if you should stick to your existing loan conditions or make an effort to switch within the bank or to another bank.

Aprajita Sharma is a freelance journalist and a certified financial planner. She can be reached at @apri_sharma on Twitter and LinkedIn.