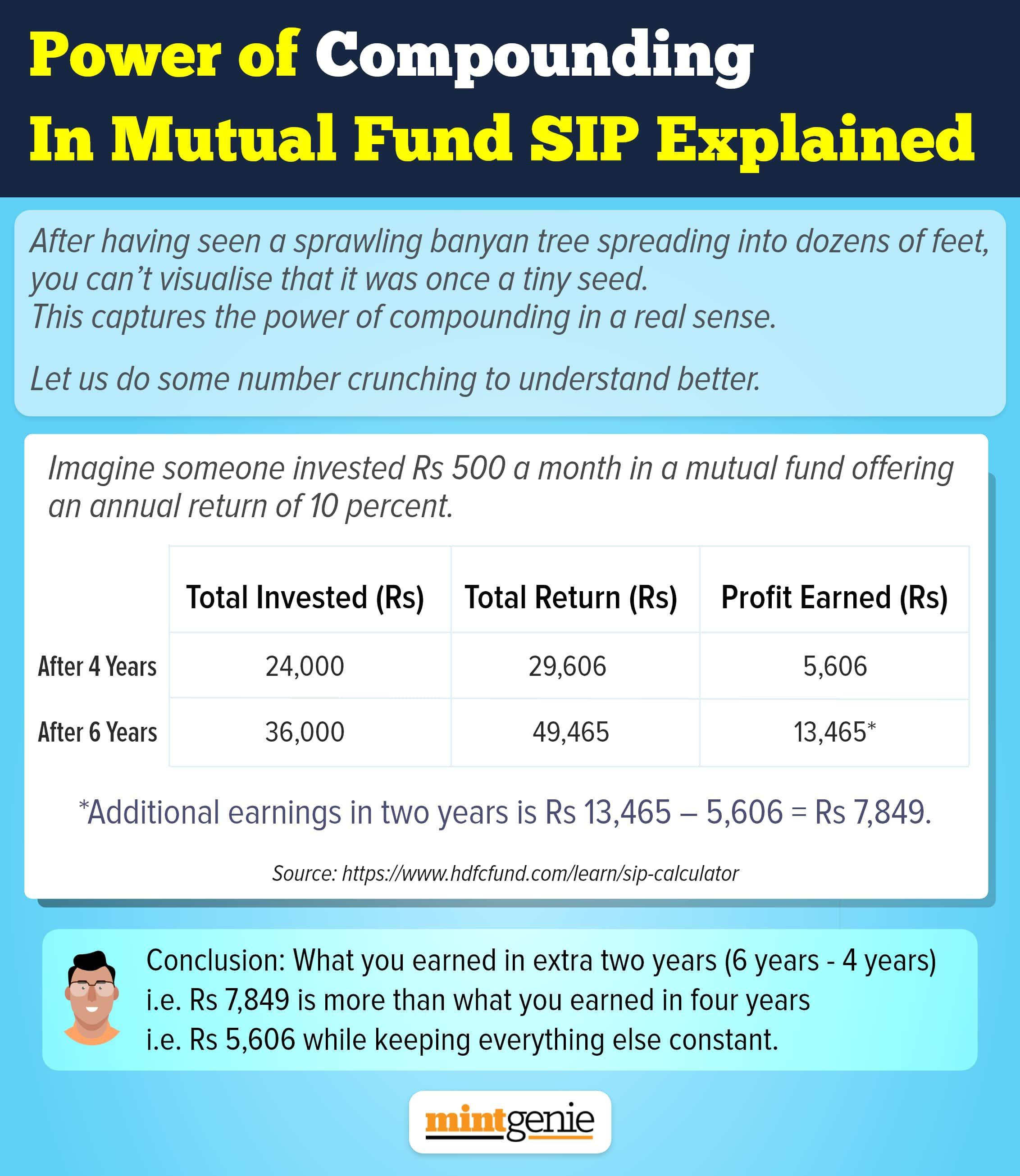

I am not here to tell you why doing SIP works. I am sure you have read tons of articles that try to convince you about that. Rather, I will highlight something else which often gets overlooked.

People start their SIP journeys with small monthly amounts like ₹5000 or ₹10,000. But will these small randomly started numbers be enough to achieve your goals? Probably not.

Doing SIP only helps you achieve your financial goals when you invest the right amount and not just any amount.

But how to find the correct SIP amount?

Find the Right SIP Amount

Further discussion demands a simple example to better understand the whole idea of the right SIP amount.

Suppose you are a 38-something professional who earns ₹2 lakh per month. Your monthly expenses, including home loan EMI, are ₹1.4 lakh.

That is, you have a surplus of ₹60,000 every month that you can invest.

A few years back, you started a SIP of ₹5000 per month. After getting good returns, you gradually increased it to ₹15,000 now. So a part of the surplus ( ₹15,000 out of ₹60,000) goes towards these SIPs. The remaining surplus isn’t well planned and gets routed to random investments and savings.

Let’s come to goals now. You have a few that have you worried:

Son’s higher education ( ₹40 lakh after 9 years)

Daughter’s higher education ( ₹60 lakh after 14 years)

Retirement at 60 ( ₹5 crore after 22 years)

If you do some calculations (or take help from investment advisor), you will find out that you need to invest the following amounts for each of the goals:

Son’s education - about ₹22,000 monthly

Daughter’s education - about ₹17,000 monthly

Retirement - about ₹53,000 monthly

Note: Assumed that investments generate about 10% returns over the investment period in a combination of equity and debt.

If you sum up the monthly numbers, then it comes to about ₹92,000 per month that you need to start investing towards your goals. Mathematically speaking, this is the right SIP amount that we were discussing earlier about.

But just investing ₹15,000 (that we assumed earlier in the example) wouldn’t help you. Right?

You will end up with a lot less money than what you need in years to come for all the goals. And then, what will you tell your son and daughter when their higher education expenses come up? Think about it.

What if You Can’t invest the Right SIP Amount today?

That’s a genuine problem. What if your income and expenses are such that you just cannot invest as much as is required?

What should be done then?

Taking the previous example - the surplus available is ₹60,000 but the required SIP amount is ₹92,000. There is a shortfall of ₹32,000 every month.

In such a case, you first invest towards the higher priority goals and cut down from the others. So out of the ₹60,000, here is how we can go about investing, priority-wise:

Son’s education – invest ₹22,000 monthly

Daughter’s education – invest ₹17,000 monthly

Retirement – invest the remaining available surplus of ₹21,000 monthly (though the required amount is ₹53,000)

This is not ideal but when the surplus isn’t enough, you have to accept and adjust.

In the above case, you are still fully funding your son and daughter’s education, though retirement savings get compromised a bit initially. But all is not lost. Once the goals of children’s education are over in the next 9-14 years, the amounts going towards those two goals (i.e. ₹22,000 and ₹17,000) will be freed up. This money can then be diverted towards retirement savings to compensate for the lower investments during the initial years.

Another good thing is that your income will also increase over the years (hopefully!). Current ₹2 lakh income and ₹60,000 surplus, both will increase every year. So extra surplus too can be pumped into the retirement bucket to bring its savings back on track. This is also what the concept of Step-Up SIP is. Every 1-2 years, you increase your SIPs in line with the increase in income.

My apologies if the conversation became a bit mathematical. But the idea was to establish the importance of knowing the right SIP amount. As you saw in the discussion above, if you wish to achieve your financial goals in time, then investing some randomly-chosen small SIP amount won’t work. You have to find the Right SIP amount and more importantly, start investing it as soon as possible.

Dev Ashish is a SEBI-Registered Investment Advisor and Founder (Stable Investor). He provides fee-only financial planning and investment advisory services to small and HNI clients across India.