Interest rates in India are higher than they have ever been in a very long time, and this elevated yield allows investors to benefit from a window of opportunity in a particular segment of the financial world that will benefit from such elevated yields.

Target Maturity Funds (TMFs) are this segment of opportunity that investors may wish to consider.

“There is a general consensus that we may be heading towards the end of a rate hike cycle. With the economic cycle advancing from slowdown to growth, it is very likely that the Reserve Bank of India would pause before moving on to a rate cut phase,” says Chintan Haria, Head Investment Strategy, ICICI Prudential AMC.

“There is a consensus that the Indian interest rate cycle seems near to its peak and that a reversal in the cycle might be due on the coming year or later. This gives the investors in TMF some marginal benefit due to interest rate cycle reversal,” says Girish Lathkar, Partner Private Wealth, Upwisery Capital Advisors.

Thus, at this point in time, one of the easiest ways to lock-in investments at the prevailing higher yields is through a target maturity fund (TMF).

So what is a Target Maturity Fund (TMF) and how do they work?

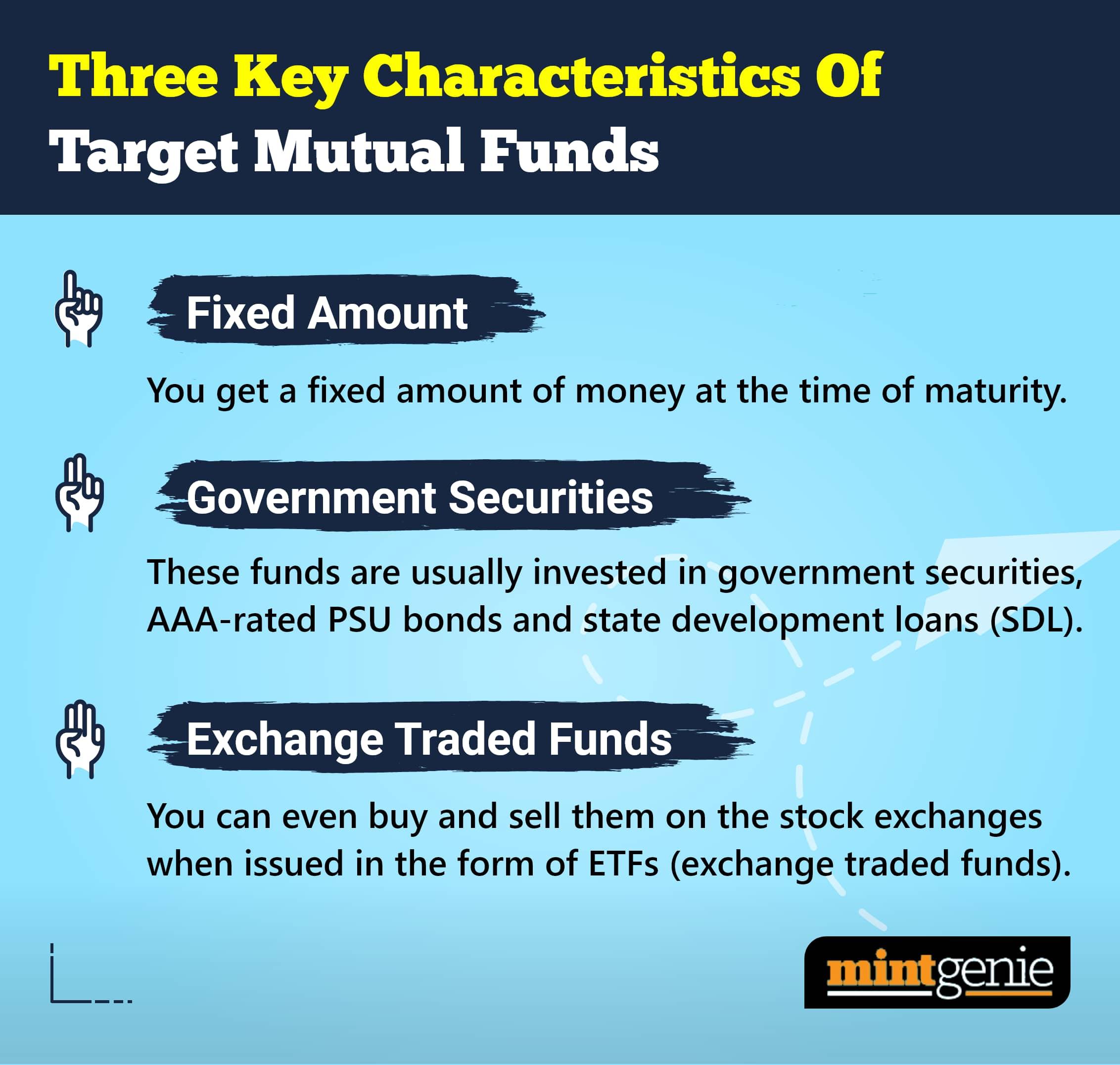

Similar to debt mutual funds, TMFs invest in a basket of fixed-income securities such as government bonds (G-secs), state development loans, and bonds issued by public sector units (PSUs) and corporate, according to note from Clear.

However, the key difference is TMFs are passively managed, that is, they track specific fixed-income indices and invest in line with the index.

Essentially, a TMF locks the money at the current yield prevailing in the bond market. Buying bonds at current prices with current (high) yields and then staying invested in them till maturity remains the core idea.

TMFs have been around in India since end 2019 and currently there are 80+ TMFs available in India, according to experts.

Chintan Haria, Head Investment Strategy, ICICI Prudential AMC, explains how TMFs work and gives us an insight why they (TMFs) make sense at this point of time.

“As the name suggests, TMFs have a fixed maturity date and, if your investment horizon aligns with this date, then you have the opportunity to lock in your returns at the present high rate of interest,” says Haria.

Why? Because the structure of TMFs is to invest in bonds with the intention of holding them till maturity. Thus, when you invest in a 10-year TMF, you place your investment in a scheme which invests in bonds with 10-year maturity, which will continue to enjoy the prevailing coupon rate, even when the rates turn lower down the years.

The structure of these funds works on decreasing residual maturity, which means that, each passing year, the maturity of the underlying bonds keeps reducing. In this way, the duration risk keeps going down, while the maturity date remains the same, making the returns from the offering predictable.

For example, an investment in a TMF of ICICI Prudential PSU Bond Plus SDL 40:60 Index Fund-September 2027, with a leftover maturity period of 4 years, will typically have a lower duration risk.

One important benefit to factor when you invest into a TMF is that you can always time your investment to an important event (say education, house purchase etc) that may occur some years into the future.

“As most of the target maturity schemes are currently available with average maturity expected within 4-5 years, investors can lock in the yields at current high levels and benefit from the residual maturity that offers low duration risk. This residual duration will have limited impact on interest rates volatility,” said Girish Lathkar, Partner Private Wealth, Upwisery Capital Advisors.

“Since TMF is designed to mature at a specific date, investors can tag the TMF investment with a specific goal,” says Haria.

Experts give their opinion on how you, the investor, need to approach your TMF from the investment perspective.

“Look to invest into target maturity funds with a goal to hold the fund till maturity,” says Kaustubh Belapurkar, Director – Manager Research, Morningstar India, who advises not to hold target maturity funds for emergency funds. Emergency funds should be parked into funds with limited interest rate risk as well as credit risk like Liquid Funds, Ultra Short Duration ,etc.

Liquidity (sale) of such TMFs is there but with an inherent risk.

While redemption is available at any point in time, mark to market impact due to interest rate movements can impact the returns of the fund in the interim. Many of these funds have long maturity investments and thus higher duration (interest rate sensitivity), which can result in significant mark to market impact on the fund NAVs in the interim. E.g. a Target Maturity Fund with a maturity date of 2033 has a duration of ~6.5 years, which means if interest rates go up by 0.5%, the fund will witness a negative mark to market NAV movement of -3.25% in the interim, according to research from Morningstar India.

Mark to market refers to the realistic estimate of the financial situation of the market depending on the assets and liabilities present.

Essentially, the structure of TMFs makes them great ‘buy’ and ‘hold’ products for investors who are looking to lock in yields and prioritize safety over earning higher yields.

But as with all financial products, do read the fine print.

In theory, in a debt fund you are paid back your principal and earn interest along the way. However, unlike most of the mutual fund schemes, the principal in TMF is not guaranteed, which is a risk that investors need to factor.

So, the entire effort is securing the principal with investments at the right time, say experts. In the current scenario, it is expected that the rates are peaking out. The expectation that the rate cycle is coming to an end points towards a surge in the Net Asset Value (NAV) of debt funds, especially those with higher duration.

Funds will have interim mark to market movement in NAV depending on interest rate movement. “These funds are passively managed and thus can lag actively managed funds that take directional interest rate calls or credit exposure in conducive market environments,” says Belapurkar.

Comparison of TMFs with other debt products

“Debt Mutual Funds depending upon the category will actively manage their portfolios within the duration and/or credit bands of the category,” says Belapurkar. Target Maturity Funds will have limited interest rate risk(if held till maturity) as compared to duration categories of funds.

TMFs with exposures to GSecs and SDLs will have lower credit risk exposure as compared to debt mutual funds with credit exposures.

Similarly, TMFs with largely holdings in central and state government bonds have lower credit risk as compared to buying bonds issued by a company.

Also, any debt mutual fund will have a diversified exposure rather than being limited to a single corporate in the case of directly buying a corporate bond.

Additionally, coupons paid by corporate bonds or interest received from fixed deposits are taxed as per the income tax slabs of the investors. TMFs and other debt funds if held for more than 3 years are taxed at an LTCG of 20% with indexation benefit, notes Belapurkar.

Research into your TMF

1) Maturity – Match maturity date with the intended investment time horizon.

2) Yield to Maturity – Current portfolio yield (Look at in conjunction with Credit Breakup)

3) Credit Breakup –Invest into funds with higher rated bond exposures (Currently most funds are a mix of government securities, state development loans (SDL) & PSU bonds).

4) Expense ratio – Lower the better.

- Morningstar India

Tax and your TMF

Target Maturity funds are taxed as debt funds (non-equity as per income tax definition).

Dividend – Taxed in the hands of investors as per their applicable tax rates.

Short Term Capital Gains (STCG)- Holding period less than 3 years taxed as per individuals income tax slab.

Long Term Capital Gains (LTCG) – Holding period greater than 3 years taxed at 20% with indexation benefit.

Manik Kumar Malakar is a personal finance writer.