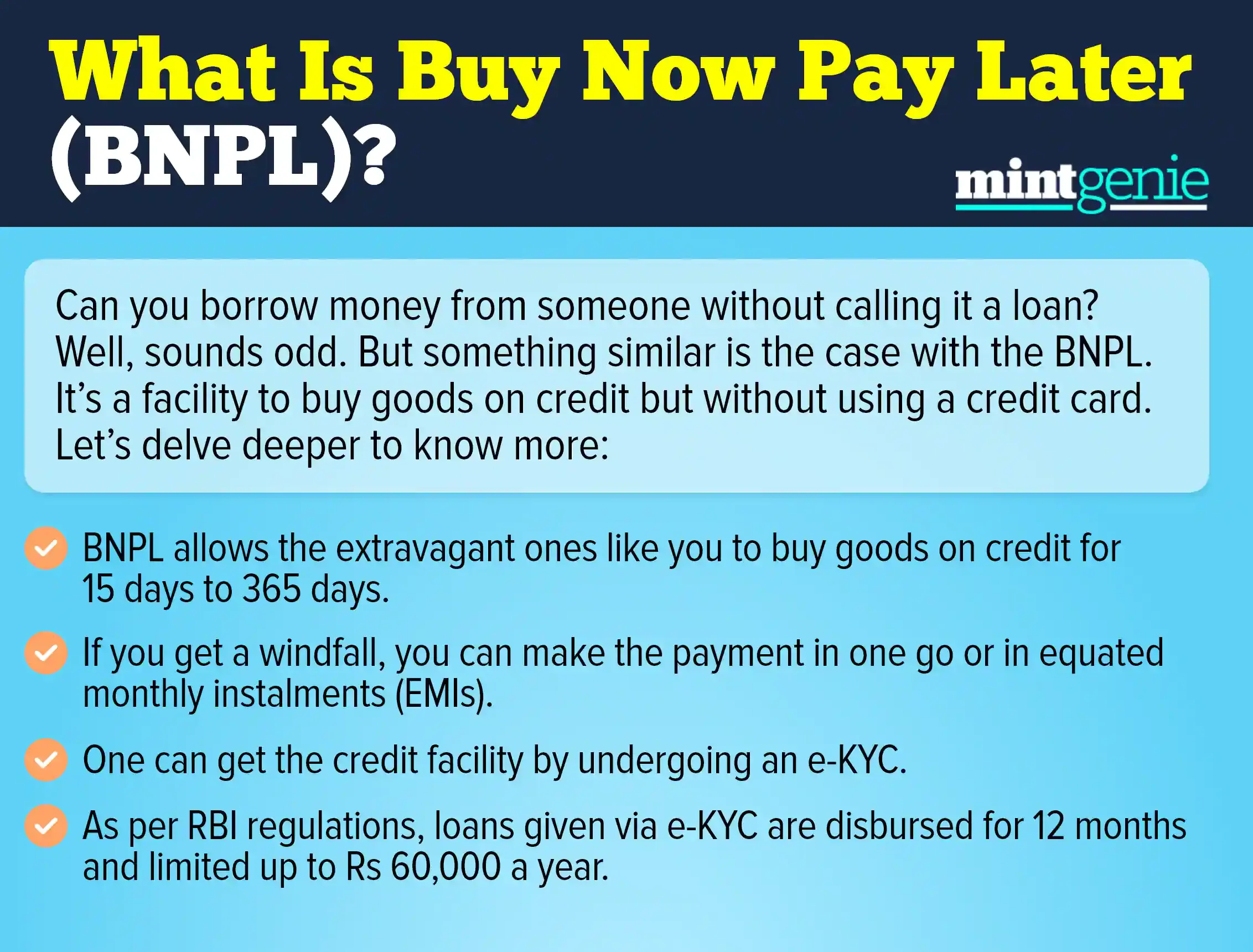

_1639560676401_1682665823037.jpg&w=3840&q=75)

In this Fintech era, every individual has access to credit irrespective of credit score and current financial situation, which opens up numerous opportunities for new and small business owners. However, along with business owners, individuals are also getting benefits of easy credit availability, which is not good news for both individuals' personal financial management and the overall economy.

Let's explore a few harmful aspects of easy credit available to individuals in terms of buy now, pay later schemes.

Unmanageable debt: By allowing individuals to purchase items without immediately paying for them, "buy now, pay later" schemes can encourage you to spend beyond your means, leading to increased debt. It can be particularly problematic for individuals who are already struggling with debt, as it can exacerbate their financial difficulties.

Higher interest rates: Many "buy now, pay later" schemes charge higher interest rates than traditional forms of credit, such as credit cards or personal loans. It means that if you are using the schemes, you may end up paying more in interest over a period of time and making your purchases more expensive in the long run.

No savings: By taking advantage of "buy now, pay later" schemes, you may be less likely to save money for future purchases or emergencies. It can leave you financially vulnerable, and it may become harder to achieve your long-term financial goals. It gives you an illusion of money, which makes you buy more than you can afford in one go.

Economic instability: The widespread use of "buy now, pay later" schemes can contribute to economic instability, as it can lead to increased levels of consumer debt and reduced savings rates. This can make it more difficult for people to weather economic downturns and can have broader implications for the health of the economy as a whole.

Potential for fraud: Some "buy now, pay later" schemes may be more susceptible to fraud or misuse than traditional forms of credit, particularly if you rely on less secure payment methods or lax verification processes. It can put both consumers and lenders at risk and may lead to broader economic instability in the event of a large-scale fraud or security breach.

How to use BNPL effectively

It seems like BNPL schemes are encouraging you to spend more than available resources, which leads to the habit of overspending for a longer period of time. If you want to take the benefits like cash back, points rewards, etc., by BNPL schemes, you can have a monthly budget for spending via BNPL, which you shouldn't cross at any cost.

You can consider BNPL not as credit money but as money in your bank account and spend according to your monthly budget. Set a reminder for the repayment and pay on the same date without any delay.

Conclusion

Monetary benefits given by credit companies seem attractive, but you need to focus on your financial health as well. By following the rules of budgetary spending, you will be able to save money on rewards and cash backs and utilise BNPL at the same time.

Anushka Trivedi is a freelance financial content writer. She can be reached at anushkatrivedi.com

Disclaimer: This story is for informational purposes only. Please speak to a SEBI-registered investment advisor before making any investment-related decision.