On the face of it both ULIPs (Unit Linked Insurance Plans) and mutual funds offer the investor some tempting investment options in the financial world. But dig a little deeper, and the two investment products are poles apart and some deep thinking is required as to which product is best suited for you.

ULIPs vs Mutual Funds: Which is a better investment option?

TL;DR.

When deciding between ULIPs and mutual funds, investors should consider their risk appetite, the fees and charges associated with each option, the investment objectives, the track record and the tax implications, to determine the best option for their financial goals.

“Investment into a mutual fund scheme is ideal for the investor who does not have the time or the knowledge to monitor the stock market and who wants a professional fund manager to manage his funds,” says Pankaj Shrestha – Head Investment Services, Prabhudas Lilladher Wealth.

Mutual funds are in a very basic form investment vehicles that pool money from many investors and invest the same in equities, bonds, government securities, money markets instruments as per scheme objectives. Each mutual fund is managed by a professional fund manager, who uses the money collected from investors to buy and sell securities on behalf of the fund.

“ULIPs are savings plans that allow an individual to earn market-linked returns along with life cover,” says Samit Upadhyay - President & Chief Financial Officer, Tata AIA Life Insurance.

While the primary objective of life insurance is to provide financial protection to the dependents, ULIPs, in addition to this, also provide an opportunity to plan for various financial goals by giving the option to switch between funds on the basis market performance, saving additional amount with the top-up features and an opportunity to partially withdraw fund value for any requirements by the investor.

Shrestha lists the salient points of the two types of investment vehicles.

The main advantage of investing in mutual funds is that investors get professional management, portfolio diversification, low cost investment, option to invest small amounts, ease of investment, liquidity, investment flexibility etc.

Negatives of investment into mutual funds include a lack of control; Investors have no control over the securities that the fund manager selects for the mutual fund. Also, it could be difficult for new investors to select the right schemes from the existing 36 categories of mutual funds and over 2500 schemes.

As far as ULIPs go they provide the dual benefit of investment and insurance, making them a comprehensive financial product. Also, ULIPs allow investors to switch between funds, enabling them to adjust their investment strategy based on market conditions or changes in their financial goals. Do remember that such switches are not taken as redemption, so it does not attract capital gains tax.

To be sure your ULIPs also have some negatives.

First off the charges are on the higher side. Charges include premium allocation charge, administration charge, fund management charge & mortality charges which negatively impacts investors return.

Next a lock-in period; ULIPs have a lock-in period of 5 years during which the investor cannot surrender the policy.

Finally, there are high surrender charges. If an investor surrenders his policy before maturity, it attracts high surrender charges/penalty.

“A ULIP is a complex investment vehicle and it is not suitable for a short term investment horizon,” advises Gautam Kalia, SVP and Head - Super Investor, at Sharekhan by BNP Paribas.

Also, they may be more expensive than other investment options for the first few years of their investment cycle.

“Any individual who is looking forward to a hassle free one stop solution for their insurance and investment needs should definitely prefer ULIPs,” says Upadhyay, when asked who should invest into ULIPs.

Past fund performance might not be a key indicator for future returns but provides ample insight into how the investments team of any of the companies is performing and great performances in the past can reflect a good performance in the future as well. “Investing in a mutual fund or a ULIP is similar but the additional life cover in case of ULIPs is what creates the difference,” says Upadhyay.

But finally as with most options in the investment world, the investor must know what are his/her priorities.

“Having the right asset allocation between equity and debt schemes as per the risk appetite of the investor should be on priority while investing in mutual funds and investors should invest for the long term while investing in ULIP policies. Investors should have adequate life insurance cover and should not only depend on life insurance over ULIP policy,” says Gautam Kalia, SVP and Head - Super Investor, at Sharekhan by BNP Paribas.

“An investor should not mix Insurance with investment goals. Insurance should be taken only to cover risk,” says Shrestha who advises that the ideal combination for investors should be taking a term life insurance policy which offers life cover at nominal premium along with investment in equity mutual funds for long term capital appreciation.

The fine print

All investment options have the fine print, that obtuse writing that serves to indemnify the issuing company while taking investors money.Experts list the fine print that we need to check in the MF versus ULIPs tug of war.

While selecting mutual funds

Investment objective: The equity fund may have the objective of investing in growth stocks or the sector fund will have the objective to invest in companies in the chosen sector. While considering the investment objective of the fund, the investor needs to consider whether it matches his financial goal requirement.

Type of fund: There are equity, hybrid and debt mutual funds. The equity funds are aggressive and the hybrid funds which invest in equity and debt are balanced whereas the debt funds are conservative. Investor should select as per his risk appetite and investment tenure.

Investment tenure: If the investment tenure is long term and the investor is ready to take risk then he should go with equity schemes and if the tenure is short term and investor risk appetite is conservative, then he should go with debt schemes.

Track record of the fund: While analysing the fund, investors should consider the consistency of the fund, the fund volatility, the track record of the fund manager and size of the fund.

While selecting ULIPs

Risk appetite of the investor: ULIPs invest in equities and fixed income securities. This investment risk is borne by the investor

Premium payment options: Multiple premium payment options are available and investors should select the policy which is convenient to the investor.

Charges in the ULIP policy: Investors should select the policy with minimal administration, fund management, switching and surrender charges.

Flexibility of switching between investment options: The cost of switches and the number of free switches during a policy year are factors while evaluating ULIP policy.

(Sources- Sharekhan by BNP Paribas)

Differences in operations

Mutual funds have a lower expense ratio than ULIPs, which means that the costs of managing a mutual fund are significantly lower than the costs of managing a ULIP.

Also, mutual funds also do not have any upfront charges, unlike ULIPs. ULIPs have a number of charges such as premium allocation charges, policy administration charges, and mortality charges. These charges reduce the overall returns earned by investors in ULIPs.

Another differential between mutual funds and ULIPs is because of the high agent commission charged by ULIPs. ULIPs are sold by insurance agents who earn a commission on every policy they sell. This commission can be as high as 20% of the premium paid by the investor. This high commission reduces the overall returns earned by the investor, which the investor must factor in while making the investment choice.

Mutual funds are sold through distributors who earn a commission on the mutual fund units sold. Typically mutual fund distributors earn around 1% commission on the value of their clients’ equity schemes and 0.5% on debt schemes.

Taxes and mutual funds versus ULIPs

Investment in ULIPs is eligible for Income Tax deduction under Section 80C where investors can claim tax deductions in an assessment year on ULIPs investment.Whereas mutual funds offer a tax deduction only against investment in ELSS.

Manik Kumar Malakar is a personal finance writer.

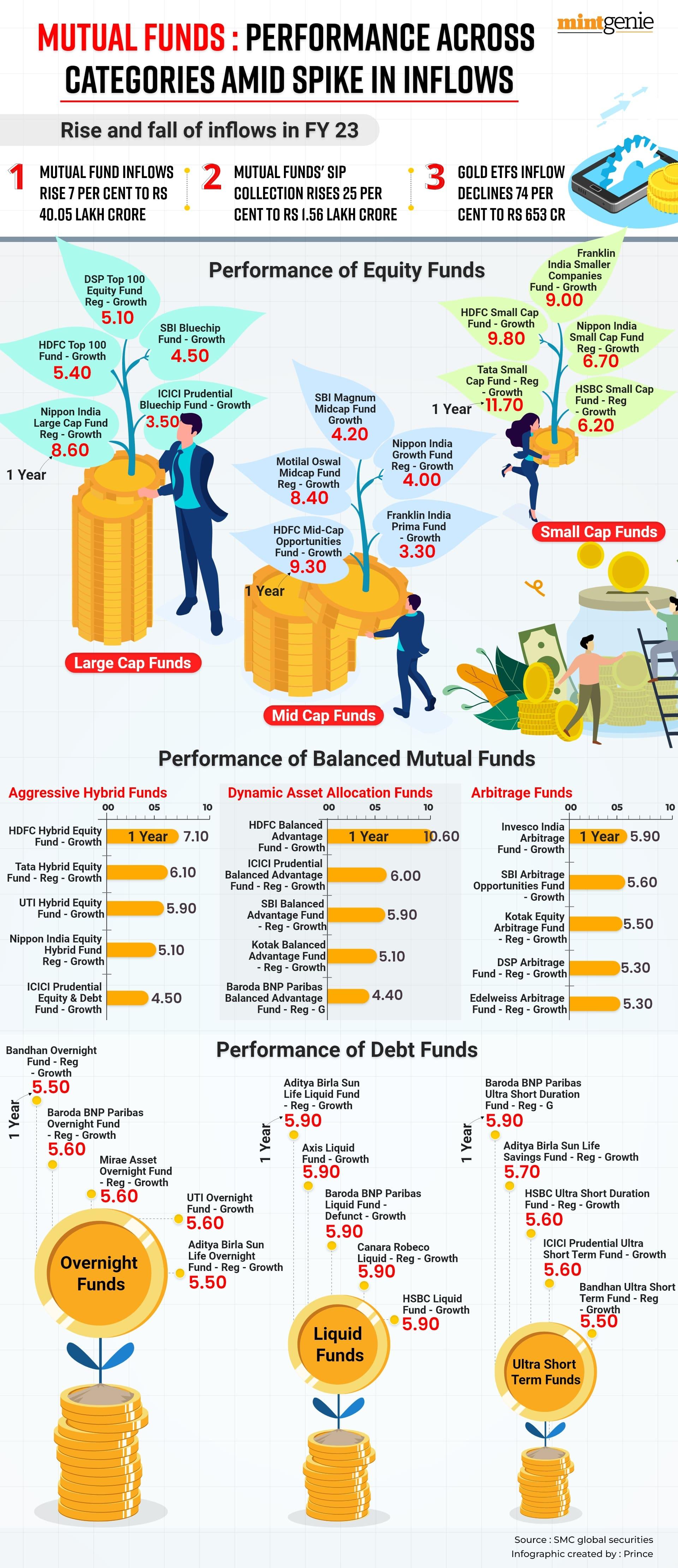

Mutual Funds' SIP collection rises 25 per cent to ₹1.56 lakh crore in FY23

First Published: 30 Apr 2023, 11:06 AM IST

Related Stories

personal finance

Open ended vs close ended mutual funds: What should investors opt for?

Padmaja Choudhurypersonal finance

Planning to invest in ULIPs? These are the factors to consider before choosing a plan

Manik Kumar Malakar