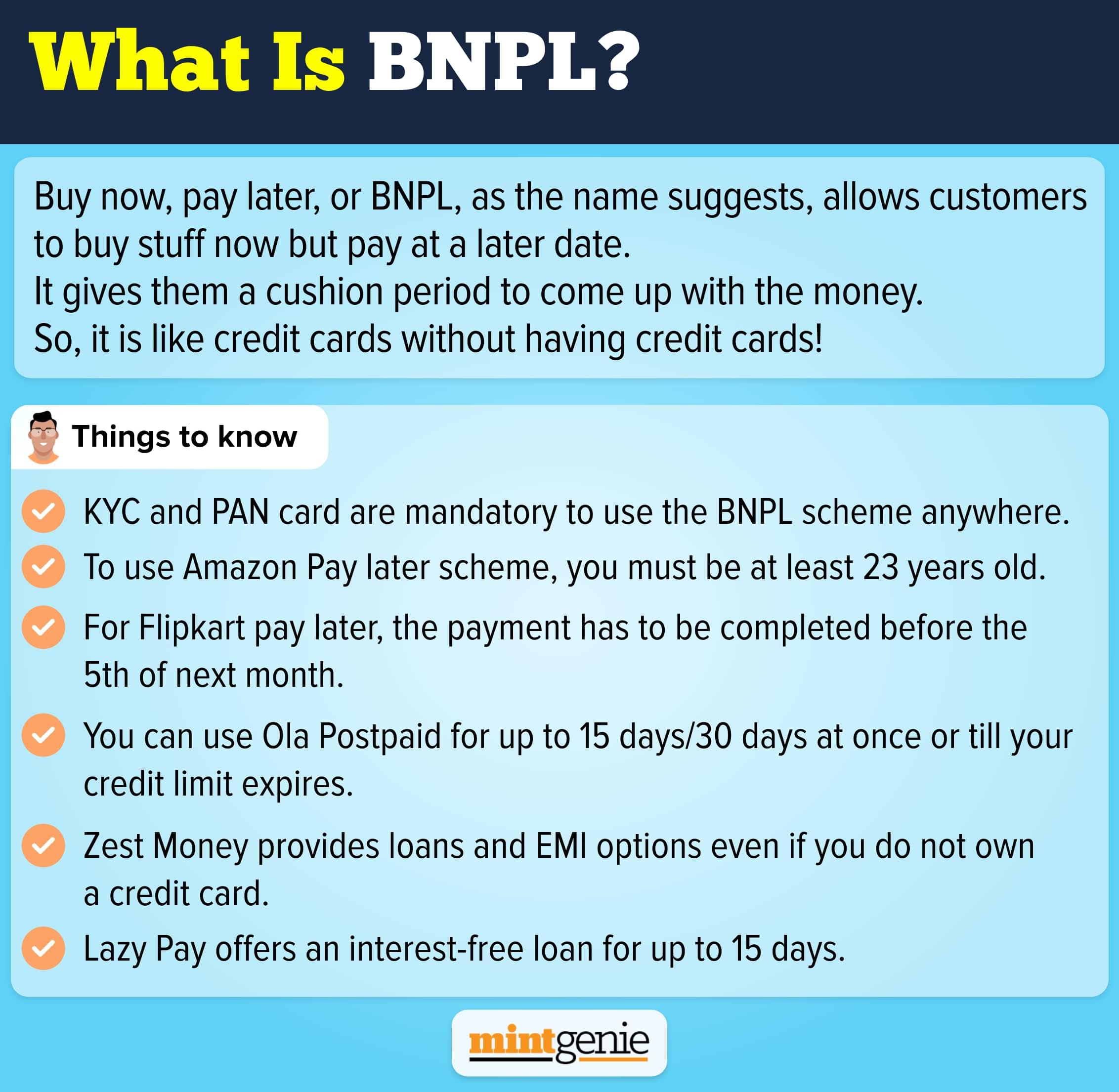

There is a whole new craze about “Buy Now, Pay Later” schemes that have prompted many fintech companies to promote this product. The BNPL scheme serves a simple purpose as it allows people to buy something without going through the hassle of having to pay for it immediately. Similar in many aspects to the credit card facility that we already avail of, the BNPL scheme caught people’s attention during the pandemic as they relied more on online shopping. The increase in the number of online shoppers catapulted the popularity of this scheme. In between, whether you must opt for it depends on your need and financial situation.

Understanding how BNPL works

Assuming that you wish to buy something, but do not have the much-needed money to pay for it. The BNPL scheme is more or less like a loan facility that allows you to purchase something in lieu of paying for it in small instalments. The first payment must be made at the time of checkout with the remaining payments getting billed to the debit or credit card until the entire purchase amount is paid for.

Though you will find many of these plans in stores today, people make the most use of them when shopping online. The most common ones that you will find today on most e-commerce platforms are KreditBee, EarlySalary, Stashfin, ZestMoney, Paytm Postpaid, Ola Money Postpaid, Amazon Pay Later, and Flipkart PayLater. These plans have now been extended for healthcare and travel services too.

Apart from the e-commerce giants and fintech players that offer this facility to their shoppers, traditional banks are also offering this product owing to its pervasive use, especially, among the millennials who love to buy things on credit. This means that you can use this facility to pay for products like gadgets and apparel apart from services including food delivery, travel booking, groceries, and other expenses.

Why is BNPL preferred?

These payments come without the pain of interest. This is the biggest benefit that BNPL users have compared to credit card users who are often burdened with huge interest debt. The loan eligibility norms are not too stringent, which means that anyone can avail of this scheme and then repay the amount within the given time frame. Only those with a certain income threshold can apply for credit cards. If you cannot meet the eligibility criteria for a credit card, the BNPL option can serve you with its similar services, albeit at much lower costs. Though in most cases, BNPL players do not charge any interest, some of them may charge interest or penalty fees for late payment.

How different is BNPL from a credit card facility?

You get the benefit of making a delayed payment for a stipulated period in both. However, you can use the BNPL facility via a partner merchant alone while credit cards can be used at any place or business where they are accepted. However, credit cards entail onboarding costs like joining fees apart from the yearly recurring fees. Though there is no concept of onboarding fees with BNPL, few non-banking lenders require their customers to pay so.

The interest charges on credit cards are considerably higher than the penalties charged by BNPL service providers. The credit limit in BNPL is, however, lower than that available on credit cards. Also, most credit cards offer an interest-free period of up to 45 days, some BNPL options allow only a small repayment period between 15 and 30 days.

Living on credit

The “Buy Now, Pay Later” scheme sounds enticing, especially, for those who love to live life on the fast track. Millennials looking to buy the best gadgets or upgrade their existing systems love this scheme. What many do not realize is that the money must be repaid within the given time. Non-repayment within the stipulated period results in an added liability (called penalty) other than the principal payment. While availing BNPL facility will enable you to create your credit history, non-repayment or late payment can lessen your credit score to a considerable extent.