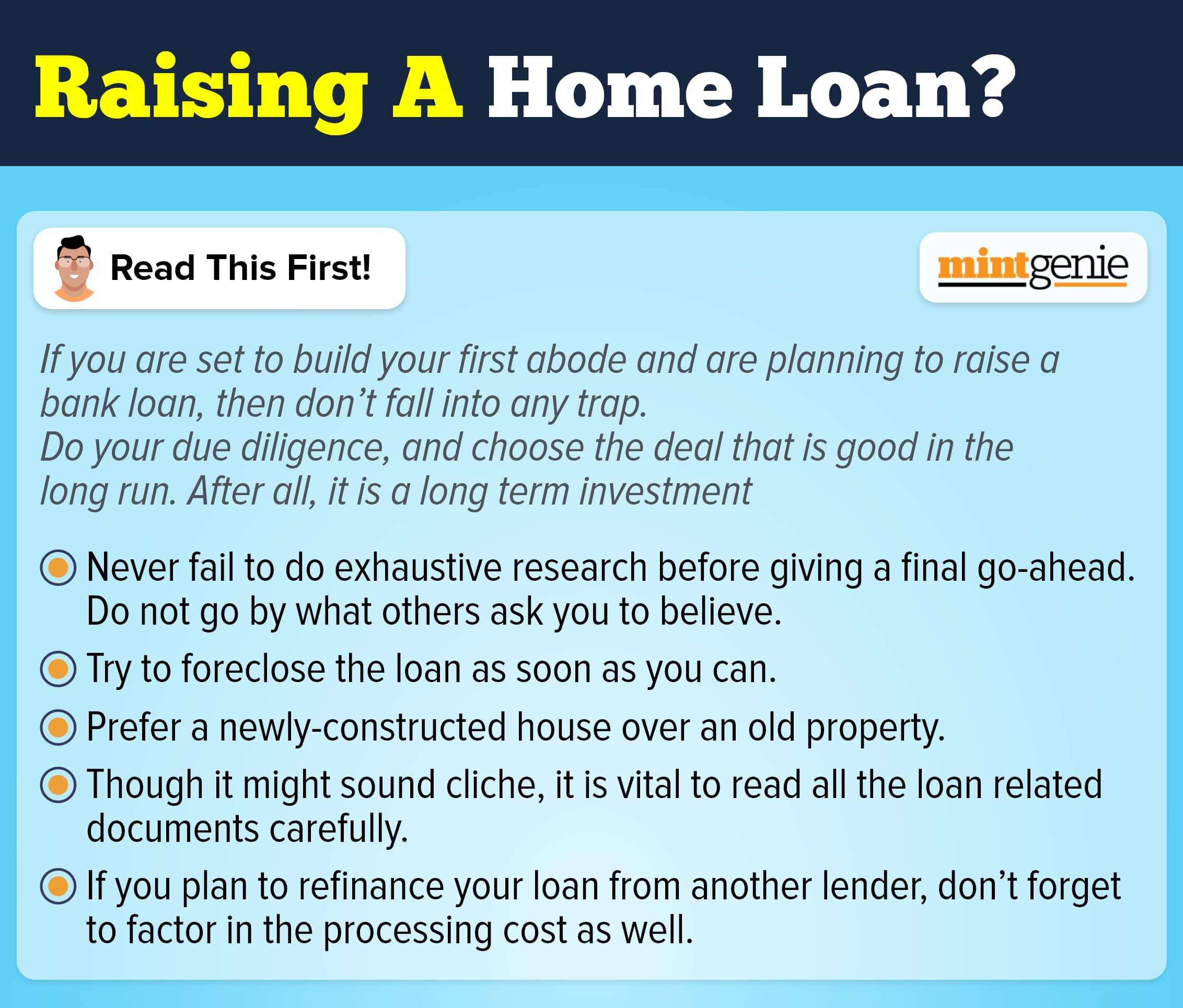

Valentine's Day is a special occasion for couples to express their love and appreciation for one another. However, this year, why not make it extra special by taking the step towards joint financial responsibility?

With a joint home loan, you and your better half can work together to purchase a home or other property of your dreams. A joint home loan is a great way to show your commitment to each other and start off your life together on the right foot.

In recent years, couples have been exploring the option of taking a joint home loan with their spouse. This is a great way for both partners to share the financial burden and benefit from the tax deductions associated with home loans.

Joint home loans are becoming increasingly popular as they make it easier for couples to purchase property together. In addition to helping couples afford larger homes, joint home loans also provide couples with the opportunity to save on taxes and build equity in their home.

What are the eligibility criteria to avail of a joint home loan?

- Applicant must be a resident Indian citizen.

- The minimum age for joint home loan applicants should be 21 years, while the maximum age should not exceed 70 years at the time of loan maturity.

- Both applicants should have a regular source of income.

- The applicants should have a good credit score and repayment record.

- Both applicants should meet the lender’s required income and employment criteria.

- Applicants must have sufficient documents to prove their identity, address, and income.

- Both applicants must submit their KYC documents, including PAN card, Aadhaar Card, voter ID, etc.

What are the benefits of a joint home loan?

Higher Loan Eligibility: One of the biggest advantages of joint home loans is that it increases the loan eligibility of the applicants. This is because the income of both the co-applicants is taken into account while calculating the eligibility. As a result, the applicants can apply for a higher loan amount than they would be able to with an individual loan.

Tax Benefits: The interest and principal repayment on a joint home loan are eligible for tax deductions under Section 24 and 80C of the Income Tax Act, 1961. Both the co-applicants can claim these deductions separately.

Lower Interest Rates: Since lenders perceive joint loans as less risky than individual loans, they tend to offer lower interest rates on joint home loans. This helps to reduce the overall cost of the loan.

Joint Liability: Another major benefit of taking a joint home loan is that the liability for the loan repayment is shared between the co-applicants. If one of the co-applicants is unable to repay the loan for any reason, the other co-applicant is liable to make the repayment.

Ease of Documentation: Applicants applying for a joint home loan need to submit fewer documents than individual applicants. This makes the process easier and faster. Applicants applying for a joint home loan need to submit fewer documents than individual applicants. This makes the process easier and faster.

What are tax benefits available when choosing a joint home loan?

A home loan is a popular option for those looking to purchase a property. Applying jointly can provide co-applicants with additional tax benefits as individual deductions are possible. Principal repayments of up to Rs.1.50 lakh are eligible for deduction under Section 80C of the Income Tax Act.

Home loan interest payments will be eligible for deduction up to ₹2 lakh if the property is self-occupied and the entire interest amount if the property is let out. This means that the collective tax benefits available in a joint home loan are much higher than those available with single-applicant loans.

Therefore, it is important for co-applicants to determine how much tax benefit they would like to avail and accordingly decide on their respective contributions. This way, they can take advantage of the greater tax benefits associated with jointly applying for a home loan.

Conclusion

Taking out a joint home loan with your spouse can be a great way to realize your dream of owning a home. There are several potential benefits, such as increased borrowing power, lower interest rates, and tax savings. However, it is important to make sure you both meet the eligibility criteria and understand the financial responsibilities involved.

Additionally, you should make sure you agree on how ownership of the property will be split, who will be responsible for making payments, and what insurance coverage is needed. If you are considering taking out a joint home loan with your spouse, make sure you do your research and properly weigh up the pros and cons before making a decision.