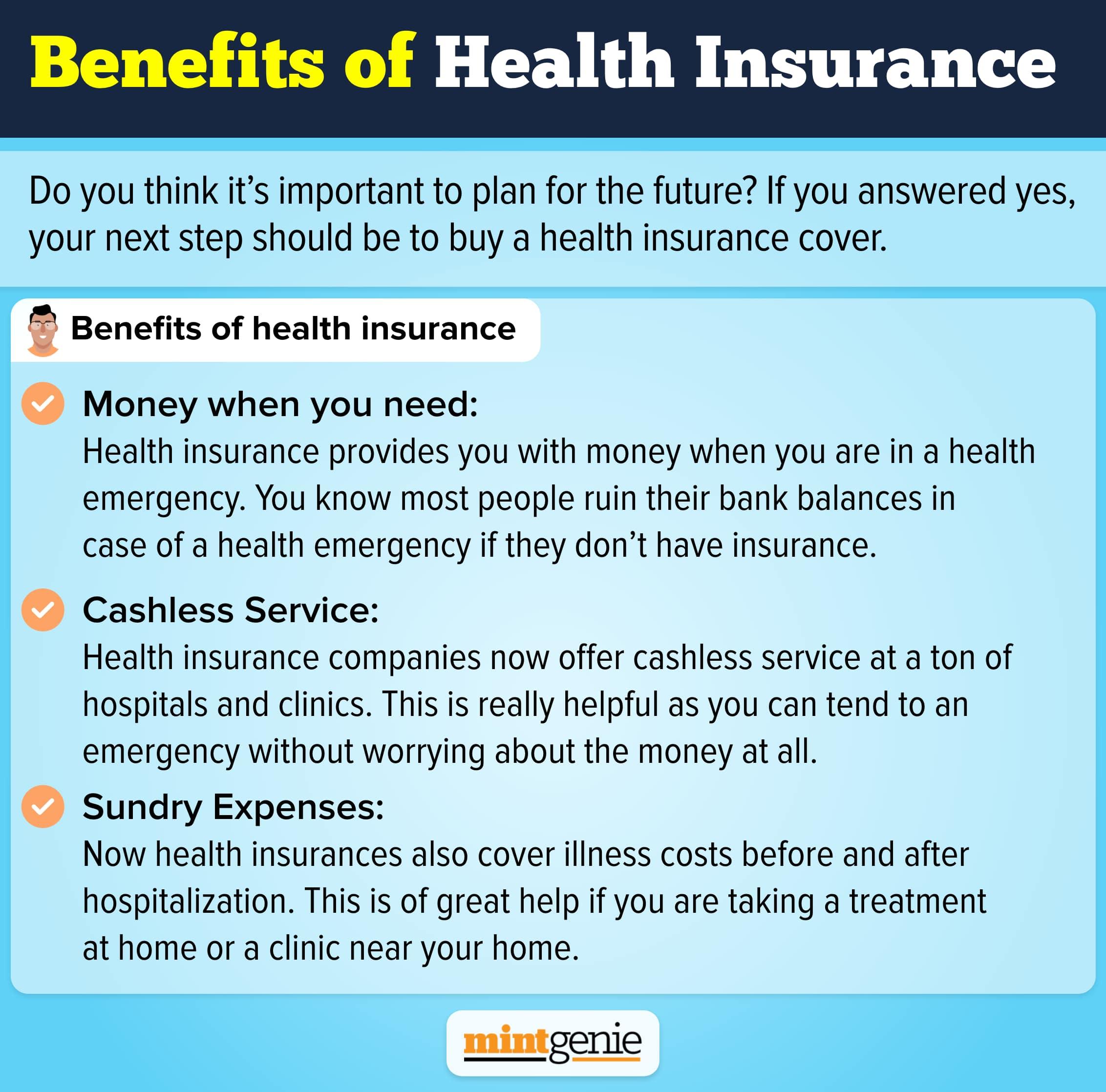

In the times of emergencies, an individual not only needs emotional support but as well as financial support. Health insurance helps in bearing the costs of the increasing medical expenses by paying the coverage, therefore the main question arises is which type of policy to be selected from the pool.

There are various policies available by different insurance companies, it is important to identify needs and wants and then make the right decision. Let’s have a look at the types of insurance policies available.

Individual Health Insurance

It is a type of insurance which covers the individual i.e., the policyholder only. The sum insured in the policy is fixed by considering major factors like age, lifestyle, medical records etc. The policy covers all the expenses which have occured in the time of any emergency related to health of the insured.

Family Floater Health Insurance

As the name suggests the plan is for all the members of the policyholder including themselves. It is an ideal policy which a person is looking for a combined policy plan. The sum insured in the plan is combined as well for all the members included, making the premium less costlier. It is beneficial to not choose the plan if one of the members is above the age of 60 years, as they are more prone to fall ill and thus making the premium costlier.

Group Health Insurance

This is the type of plan which is bought for colleagues or employees. It is a kind of incentive offered to the employees which increases their retention in the company. The plan has a low cost premium and some insurance companies also allow refills for the sum insured.

The plan covers hospitalization caused by accidents, psychiatric reasons, maternity, critical illness etc. It is important to note that the policy only holds till the time the employee is part of the organization.

Senior Citizen Health Insurance

The plan is most ideal for individuals who are above the age of 60 years. The policy covers expenses of medication, pre and post treatments, cases of critical illness and accidents.

Some companies also conduct full-body checkup before the policy is signed in order to fix the sum insured and the premium price. As the senior citizens are more prone to health problems, these policies are considered to be more expensive.

Maternity Health Insurance

It is a plan for newly married couples or families who are planning to have a baby in the coming years. All the expenses incurred during the pregnancy, pre and post delivery and expenses of the baby till 90 days are covered in the policy. The waiting period of the policy in 2 years.

Critical Illness Insurance

Lifestyle diseases have increased over the years, because of which insurance companies have come up with an insurance policy which covers certain health diseases under it. The health problems include - cancer, stroke, kidney failure, paralysis, coronary artery bypass surgery, heart attack, pulmonary arterial hypertension, multiple sclerosis, aorta graft surgery.

As the treatment of these health problems is quite expensive, the policy gives a fixed amount of payment to the insured as and when they get diagnosed. The policy has life-long renewability and the most crucial part is that the policyholder needs to survive 30 days after the diagnosis to avail the benefits.

The important part to note is that, when the diagnosis is done the sum insured fixed is given in lump-sum and then the policy terminates.