Choosing the right investment option for you can be confusing and scary. With a number of options to choose from varying from equities to bonds to government schemes etc, it can be a difficult decision to make.

While equities are riskier investments, bonds and government schemes make a safer choice. One such safe investment option is savings bonds. These are convenient for people who are looking for a fixed income source. They have a fixed rate of return and hence are unaffected by the markets or the economic conditions.

Generally, bonds have a higher minimum investment limit so a number of investors do not prefer it, however, savings bonds have lower investment limits making it easier and more affordable for investors.

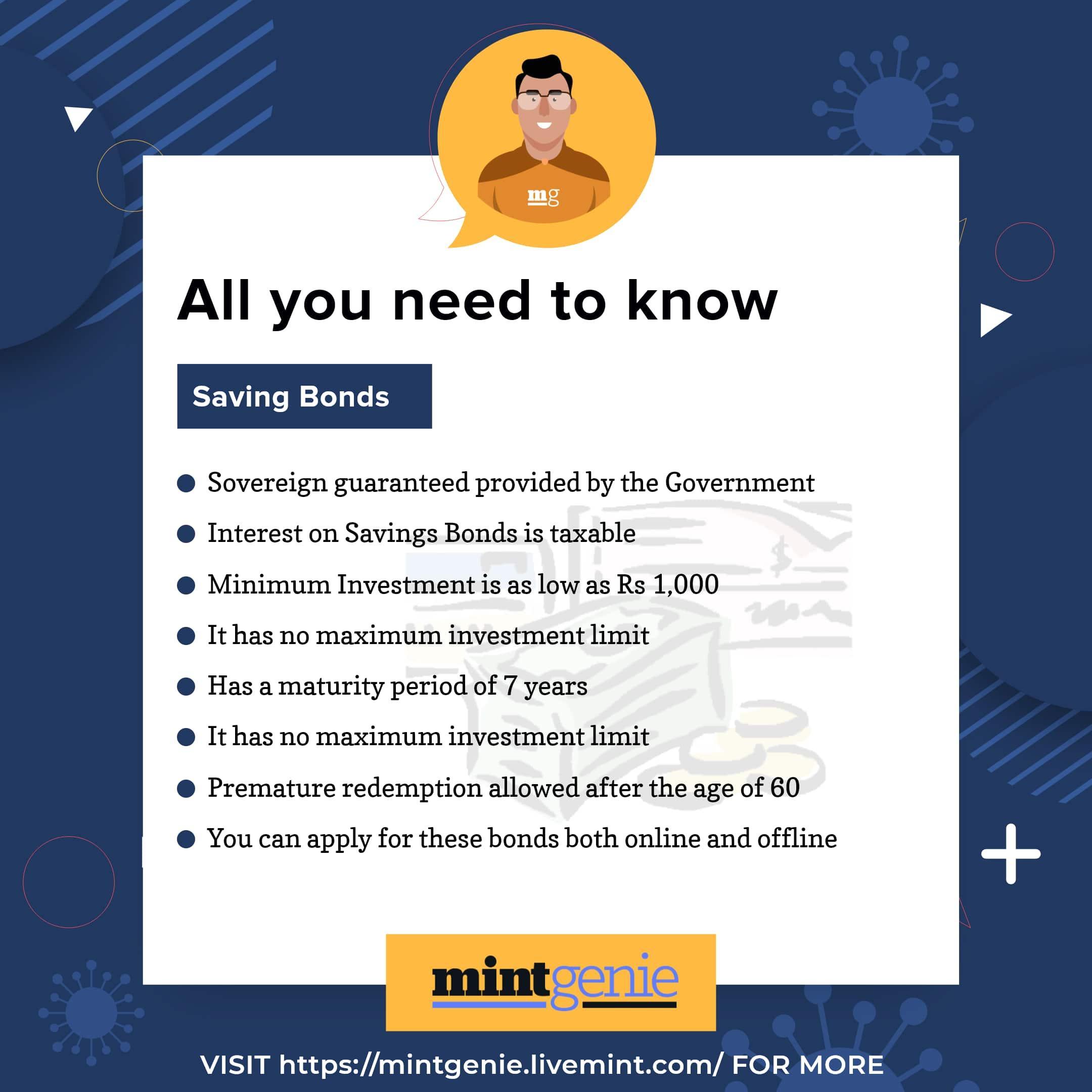

In 2003, the government introduced an 8 percent Savings Bond but later replaced it in 2018 with a 7.75 percent bond. It has a minimum investment of ₹1,000 or in multiples of ₹1,000 making it very affordable.

Types

There are two options available to you while investing in a savings bond - cumulative and non-cumulative.

In the cumulative option, the interest is paid out directly at maturity. So suppose you invested ₹1000, you will get ₹1,703 at maturity. The interest amount is reinvested in bonds till maturity in this case.

While in the non-cumulative option, the interest is paid out every six months to the investor.

Let's look at the key features of this bond to decide whether it is a good choice for investment:

1) Any individual or Hindu Undivided Families can invest in these bonds. However, they are not open for investment to non-resident Indians (NRIs).

2) These bonds have a sovereign guarantee which means the agreed-upon rate of interest, currently 7.75 percent, will be paid by the government irrespective of any downtrends. At maturity, the total amount (principal + interest) will be returned to you by the government and there is no risk involved.

3) One can apply for these bonds in online as well as offline mode. A number of banks also provide this investment option. You can download a form online, or take one from their branches, fill it up and submit it.

4) The bank then starts the process and issues you a certificate of holding for proof of investment.

5) It is important to note that these bonds are NOT tax-free. The interest you get on these bonds will be added to your taxable income and taxed at your income tax rate. A TDS will also be deducted on the interest earned.

6) While the minimum investment limit of a savings bond is ₹1,000, there is no maximum limit. You can invest as much as you like.

7) While the redemption period is 7 years, premature withdrawal is allowed for senior citizens. The lock-in period decreases as the investor's age increases.

8) These bonds are non-transferrable.

9) These bonds cannot be used as collateral for loans like PPF.

Now that we know what are the basic features of a savings bond, it will be easier for you to make a decision as to whether it fits your portfolio or not.