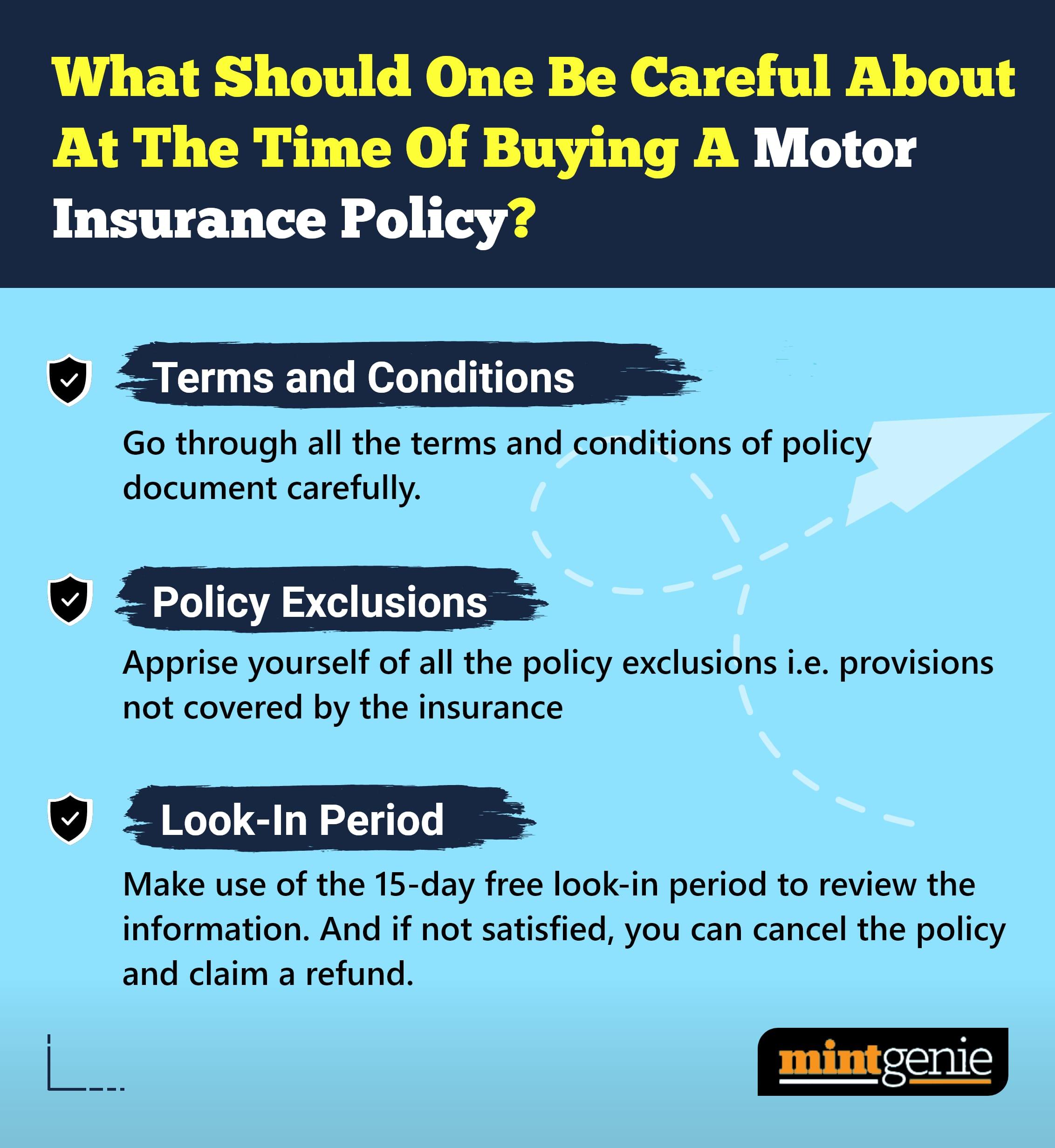

_1640329695989_1654140324657.jpg&w=3840&q=75)

Insurance is a contract between an insurance provider and an individual or entity that aims to accord security and financial support to the buyer in times of crisis. There are myriad types of insurances that one can choose from. Let’s look into two broad categories of insurances- Life insurance & General insurance and learn the difference between them.

Life Insurance

A life insurance policy is an agreement in which the insurance company covers the life of the insured. If the policyholder dies during the term of the policy, the beneficiary, as nominated by the policyholder, will be offered monetary compensation. This insurance is usually bought to support the family of the deceased in the event of his/her premature demise.

General Insurance

General insurance is an insurance contract for a particular asset wherein the insurer compensates for any expense of loss/damage pertaining to that asset. The insurance provider is liable to cover the costs of the insured asset in case of an unfortunate event. Types of general insurance include car insurance, home insurance, travel insurance, health insurance, etc.

These policies differ on the following basis:

Cover: Life insurance covers the life risk of a person whereas general insurance covers non-life assets such as vehicles, houses, health among others.

Nature: General insurances work on the principle of indemnity i.e. compensation in the event of loss or damage. Life insurance policies are however considered a type of investment to safeguard the family of the insured. The compensation for life insurance is paid either on maturity or in the event of death.

Premium: The premium for life insurance policies is fixed and is based on the cover amount that the policyholder chooses. On the other hand, the premium for general insurance policies varies depending on the condition/value/depreciation of the asset. For example: In health insurance, the premium for an individual depends on his/her age, lifestyle habits, and various other factors.

Sum insured vs sum assured: Sum insured is the amount of money that is paid as reimbursement to the policyholder in the case of damage to the asset under general insurance. While in life insurance the sum that the company is potentially liable to pay to cover the claim is called sum assured. Sum assured is a fixed sum that is paid in total whereas the sum insured depends on the extent of the damage.

Beneficiary: The benefit of the policy in general insurance is enjoyed by the insured himself. In the case of life insurance, the benefit of the claim goes towards the family member nominated by the policyholder at the time of signing the contract.

Tenure: Life insurance policies are for a long term. On the contrary, general insurance contracts are short-term and can be extended as per the policyholder’s wish.

Different types of insurance policies are offered in the market for individuals with diverse demands. It is advisable to understand the terms and inclusions of a policy and select one to suit personal needs before sealing a deal.