What will you do if you want to earn a regular interest of over 8 percent per year without having to risk your money in equity? Well, FD does not come anywhere close to this goal. And everything else, as they say, “is subject to market risk!”.

So, what is the next best option?

JM Financial Products recently announced the issue of its redeemable non-convertible debentures (NCDs) that will offer an interest at an aspirational rate of 8.2 percent per annum, a far cry for bank FDs. They will be redeemed after 5 years, or 60 months. Another option is to go for redemption after 100 months and earn 8.3 percent per annum.

In comparison to FDs

The interest rate offered by JM Financial Products ranges between 7.91 (monthly) to 8.2 (annual) when redeemed after 60 months, and 8.3 percent on 100-month redemption.

This is a handsome interest, especially when compared to the fixed deposit (FD) rates offered by the state lender State Bank of India (SBI) which gives 5.4 percent per annum for 60 as well as 100 months.

Let us try to understand this with the help of an illustration:

If you invest ₹3 lakh in JM Financial for 60 months, then the pre-tax income at 8.2 percent would be ₹1,23,000.

In case of SBI, the interest would accumulate to ₹90,234 (pre-tax) after five years ( ₹16,200, ₹17,075, ₹17,997, ₹18,969, ₹19,993).

So, an investor stands to earn ₹32,766 extra on account of risking his money with an NBFC instead of an FD in five years.

Risk versus returns

The concept of trying to strike a balance between the risk and return is as old as the financial markets. If you want to maximise your returns, you have no choice but to take risky bets – be it equity or debt.

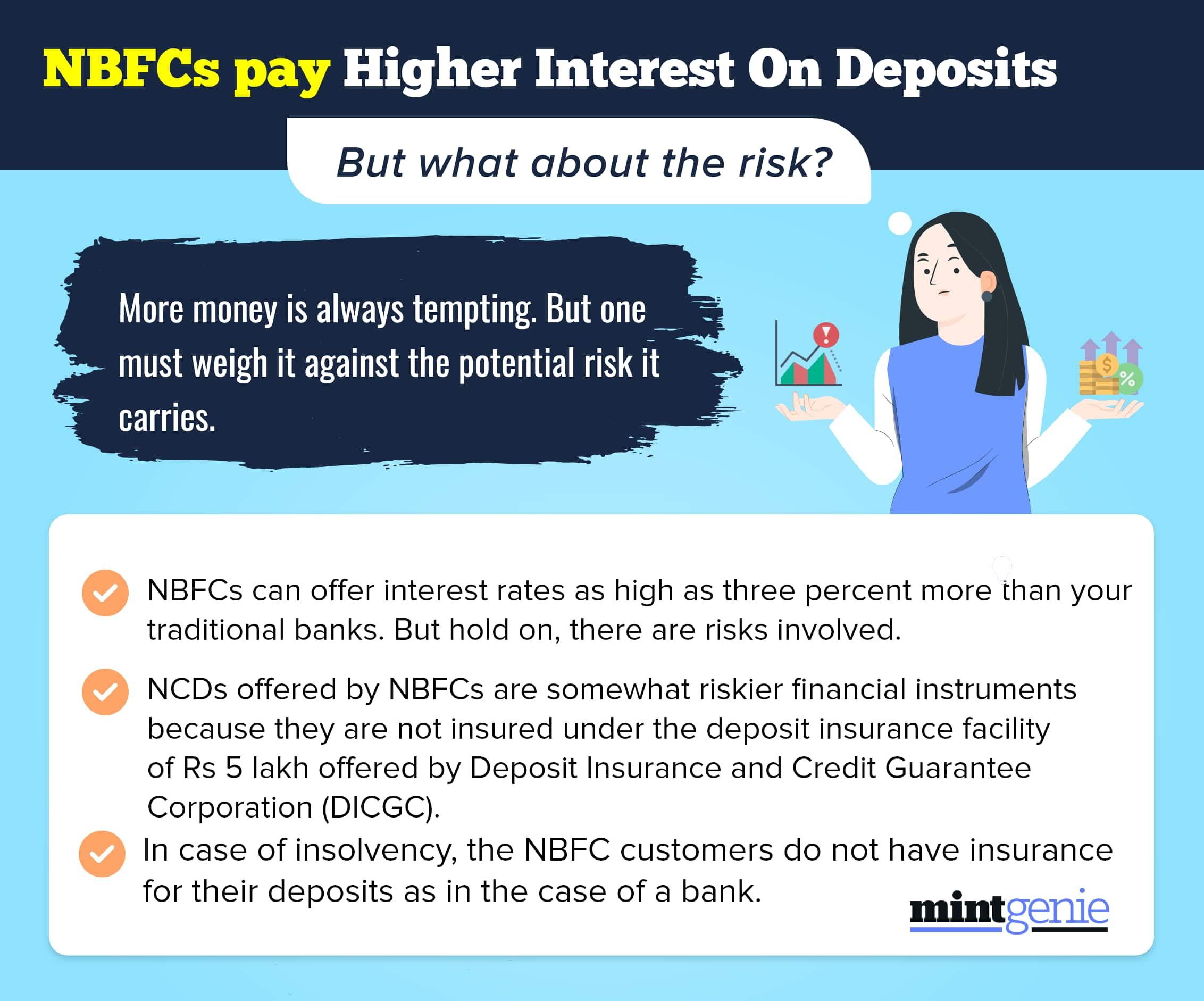

So, to be able to earn a higher interest rate on fixed income investments, you have to put your money into relatively riskier financial instruments such as NCDs by NBFCs (Non-Banking Financial Corporations).

Even the banking regulator Reserve Bank of India (RBI) highlights on its website that the deposit insurance facility of ₹5 lakh offered by DICGC (Deposit Insurance and Credit Guarantee Corporation) to all banks in the country is not given to the NBFC customers.

This means in case of insolvency of an NBFC, the customers do not have an insurance of their deposits, as in case of a bank.

Even RBI’s Deputy Governor M Rajeshwar Rao mentioned in November 2020 that the NBFCs with high systematic risk should be identified and put under stricter regulation.

However, risk is a relative term. NBFCs may be riskier than the bank FDs, but they are not as risky as equity. And there is help at hand. You can check the credibility of the issue via ratings given by the credit agencies such as ICRA and CRISIL.

A good rating implies the company will give prompt payment of interest and would likely not default on principal payment. JM Financial NCD, for instance, has been rated AA/stable, which means there is not much to worry about.

So, we can highlight that NCDs with the likes of JM Financial Products can be seen as a better option to earn some extra bucks over an FD, so long as you are willing to take some amount of risk.